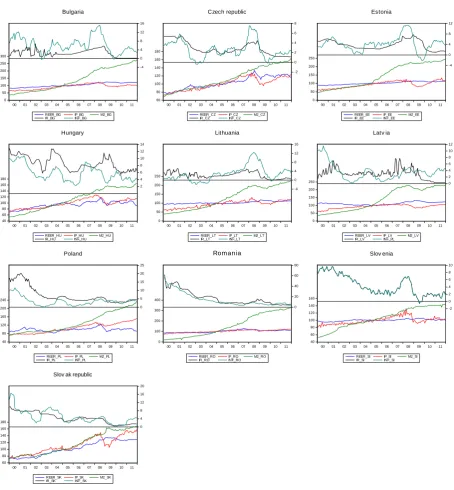

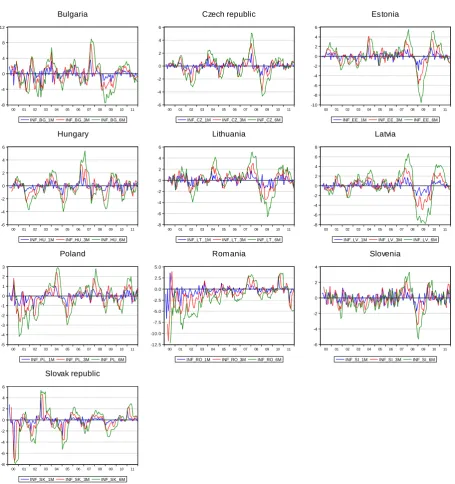

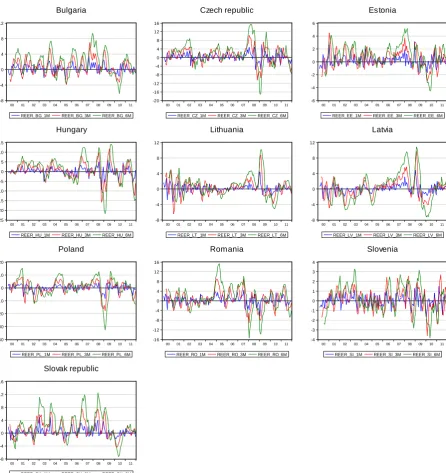

Real Output and Prices Adjustments Under Different Exchange Rate Regimes

Full text

Figure

Related documents

The OIC aims to improve the practices of Thailand’s insurance industry so as to conform with the Insurance Core Principles (ICP), as written by the International Association

By estimating wage regressions with data from the German Socio-Economic Panel (GSOEP) and using individually perceived hazards of work accidents as a risk variable, evidence that

A way of han- dling such a feedback situation is to use a model of the feedback path from the control loudspeakers to the feedforward microphones to sub- tract the contribution from

Each response to a GZ2 morphology question is allocated a p value ranging from 0 to 1, where 0 indicates no volunteers responded positively to that question and 1 indicates

Therefore, the comparative study of time series and artificial neural network methods for short term load forecasting is carried out in this paper using real time load

This paper proposes a method to find a deep neural network centred on architecture evolution (DNN-CAE) for short-term load forecasting. The method focusses on NAS using EA

The present study discusses the use of fuzzy inference mechanism to recognize the most notable rules in the development of fault prediction model using GUAJE framework ( Alonso

This study predicts future runoff conditions under changing climate using multi model outputs from Coupled Model Intercomparison Project Phase 5 (CMIP5) over Lake