KATHRYN R. MULLEN. Beverage Container Deposit Laws and Their

Effect on Curbside Recycling. (Under The Direction of Dr. RICHARD

N.L. ANDREWS)This paper examines the effect beverage container deposit laws

(BCDLs) have on curbside recycling, focusing on the Orange County

program. A literature study was conducted to help develop a model

which was used to determine the cost increase to a municipal

recycling program when a BCDL is in effect. The results were that

it costed $169.53 per ton to run a municipal recycling program in

1991. If a BCDL had been in effect and the cost to run themunicipal recycling program would have increased to $229.25 (If all

the materials that could be collected in the BCDL were divertedfrom the recycling stream to the BCDL stream). Collections cost

remain constant in a dual system, however revenues decrease

dramatically. Processing cost also decrease but not as

dramatically as revenue resulting in the increased costs to a

municipal recycler under a BCDL system.

I. INTRODUCTION ... 1

1.1 Definition of a Beverage Container Deposit Law... 1

1.2 The History of the Beverage Container Industry ... 2

1.3 States that have Beverage Container Deposit Laws ... 5

1.4 North Carolina's Interest in Beverage Container Deposit Laws ... 9

II. THE EFFECTS OF BEVERAGE CONTAINER DEPOSIT LAWS ON CURBSIDE RECYCLING ... 12

2.1 The Franklin Associates, LTD. Model... 13

2.1.1 Structure and Assumptions... 14

2.1.2 The Franklin Associates, LTD.'s Findings . 15 2.1.3 Analysis of the Franklin Associates, LTD. Study... 20

2.2 The Gershman, Brickner & Bratton, Inc. Study . . 22

2.2.1 Structure and Assumptions ... 22

2.2.2 GBB's Findings... 25

2.2.3 Analysis of GBB's Findings ... 26

2.3 The Rhode Island Model... 27

2.3.1 Structure and Assumptions... 27

2.3.2 Findings of the Rhode Island Study .... 28

2.3.3 Analysis of the Rhode Island Study .... 30

2.4 The Florida Public Interest Research Group Study 32

2.4.1 Structure and Assumptions... 322.4.2 Finding of the Florida PIRG Ed Fund Study . 3 3

2.4.3 Analysis of the Fl. PIRG Ed. Fund Study . . 33

2.5 Review of "Bottle Bills and Municipal Recycling: A

Preliminary Cost Analysis" by the Tellus Institute... 402.5.1 Structure and Assumptions... 40

2.5.2 Findings of the Tellus Institute... 42

2.5.3 Analysis of the Tellus Institute... 44

2.6 Conclusions... 46

III. PROJECTED EFFECTS OF A BCDL ON ORANGE COUNTY'S RECYCLING PROGRAM ... 50

3.1 Scenario for Orange County ... 50

3.2 Landfill Avoidance Costs ... 54

3.3 Conclusions... 59

IV. CONCLUSIONS... 60

4.1 Generalizations about the Effects of BCDLs on

Curbside Recycling Programs... 60

4.2 Can Curbside Recycling and BCDLs Coexist? .... 61

4.3 Escheat Clauses... 62

XV

Appendix A... Al Appendix B... Bl

Appendix C... CI

Appendix D... Dl

Figure 1.1 How a Deposit System Works ... 3

Table 1.1 Generation of Beverage Containers, 1960 to 2000 (InMillions of Tons) ... 4

Table 1.2 Beverage Container Deposit Laws ... 6 Table 1.3 Bottle Deposit Legislation in North Carolina . . 11 Table 2.1 Summary of New York Comprehensive Municipal Recovery

Program's Capital Costs, Annual Operating Costs,

Revenues, Net Operating Costs, And Recyclables RecoveredWith A BCDL in Place (in dollars and tons) ... 16

Table 2.2 Summary of Vermont Comprehensive Municipal Recovery

Program's Capital Costs, And Recyclables Recovered With

and Without A BCDL In Place (In dollars and tons) . . 17 Table 2.3 Comparison of Net Costs To Operate Two Separate

Recyclable Material Recovery Systems or One System - New

York... 18

Table 2.4 Comparison of Net Costs To Operate Two Separate Recyclable Material Recovery Systems or One System

-Vermont... 19

Table 2.5 Islip Residential Recycling System Revenues and

Costs With and Without BCDL in 18,991 Households ... 23

Table 2.6 Anne Arundel Residential Recycling System Revenues

and Costs With and Without BCDL... 24 Table 2.7 Recycling Cost Per Ton... 25

Table 2.8 Comparison of Rhode Island's Curbside Recycling

Program and a Curbside/BCDL Program ... 29

Table 2.9 Comparison of Rhode Island's Curbside Recycling

Program and a Curbside/BCDL Program When Residues areLandfilled... 30 Table 2.10 Cost to the Municipal Recycling Program in

Rhode Island ... 31

Table 2.11 City of Tallahassee Recycling: Government Costs and

Revenues in Calendar Year 1991... 34 Table 2.12 City of Gainesville Recycling: Government Costs

Table 2.13 City of Hialeah Recycling: Government Costs and

Revenues in Calendar Year 1991... 36

Table 2.14 City of Miami Recycling: Government Costs and Revenues in Calendar Year 1991... 37

Table 2.15 Cost of Curbside Program vs. Curbside/Bottle Bill When Only the Materials Collected in the Curbside Program are Considered... 39

Table 2.16 Cost of Curbside Program vs. Curbside/Bottle Bill When Only the Materials Collected in the Curbside Program are Considered and the Landfill Avoidance Cost is not Considered... 39

Figure 2.1 Social Cost Comparisons With and Without a Bottle Bill... 43

Figure 2.2 Municipal Cost Comparisons With and Without a Bottle Bill... 45

TABLE 2:17 Effects Of BCDL On Curbside Recycling Programs 47

Table 3.1 Predicted Effect of a BCDL on the Curbside Recycling Program in Chapel Hill... 51

Table 3.2: Processing and Collection Costs ... 55

Table 3.3 Collection Costs Variance ... 56

Table 3.4 Processing Costs Variance ... 56

Table 3.5 Newspaper Revenue Variances ... ... 56

Table 3.6 Aluminum Revenue Variances ... 57

Table 3.7 Glass Revenue Variances ... 57

ACKNOWLEDGEMENTS

I would like to thank my husband who supported me throughout the writing of this document and had faith in me even when I did not.

Also I want to thank him for his love and support. I would also like to thank my parents and my brother whose encouragement and love were a constant source of emotional strength.

I would like to thank Dr. Richard N.L. Andrews for his guidance during my study at UNC. I am also grateful to Dr. Deborah Amaral

and Dr. Luger for their positive criticism and support during the

preparation of this report.

I am grateful to Amanda Williams who proof-read my final draft. Also I would like to thanK Blair Pollack and Wendy McGee who

This paper presents a study of the effect of beverage container deposit laws (BCDLs) on curbside recycling, focusing on the effects that a beverage container deposit law would have on curbside recycling in Orange County, North Carolina. Beverage Containers are a growing segment of the

waste stream. Also they are very visible component of litter. As landfill space continues to dwindle, new solid waste management policies will need to be evaluated. One of the possible solutions to this problem has been beverage container

deposit laws.

One of the major criticisms of these policies has been the effect a BCDL has on curbside recycling because it pulls

aluminum and glass out of the recycling stream. If these programs can be run simultaneously the amount of recyclables

diverted from the waste stream can increase significantly. It

is speculated that they become more expensive to run because

aluminum, which is the most valuable material in the recycling

waste stream, is diverted to the BCDL stream.

I have evaluated five studies which estimate the effects

of a BCDL in Chapter 2. These studies have different assumptions which affect their outcomes. I evaluate each on

the validity of its assumptions. I use critiques of these

studies construct the framework within which the outcome of a

BCDL on curbside recycling in Orange County is predicted.

1.1 Definition of a Beverage Container Deposit Law

A Beverage Container Deposit Law (BCDL) or a bottle bill,

as it is often called, is a deposit-refund system which is

the brewer/bottler. For the soft drink industry, this is

usually initiated by the distributor. Retailers pay a deposit

to the distributor when they buy the beverages and receive adeposit from the consumer when they sell the beverage. When

the consumer returns the beverage container, the retailer

reimburses the consumer, and then is reimbursed by the distributor. Figure 1.1, taken from the US GAO report. Trade¬ offs Involved in Beverage Container Deposit Legislation illustrates the deposit return cycle.

1.2 The History of the Beverage Container Industry

After World War II, the steel and can industry

realized that there was an opening to expand the beverage

industry market. The beverage industry suggests that

consumers were interested in more convenient packaging. In

1935, beer was first packaged in nonrefillable cans. This was

followed by the emergence of the "one way" bottle. By 1970

the container mix was 40% nonreturnable soft drink packaging

and 76% non-returnable beer packaging. By 1986 the mix was 86% nonreturnable soft drink containers and 91% non-returnable

for beer containers^.

Figure 1.1 How a Deposit System Works^

Beverages Are Sold and Depostts Are Paid

Distributor

Retailer

Beverage

Consumer

Empty Containers Are

Redeemed for Deposits

Consumer

Empty Bottle

I

Retailer

Empty Bottle

i

Distributor

^General Accounting Office, Report to Congressional

Requesters, Trade-offs Involved in Beverage Container Deposit

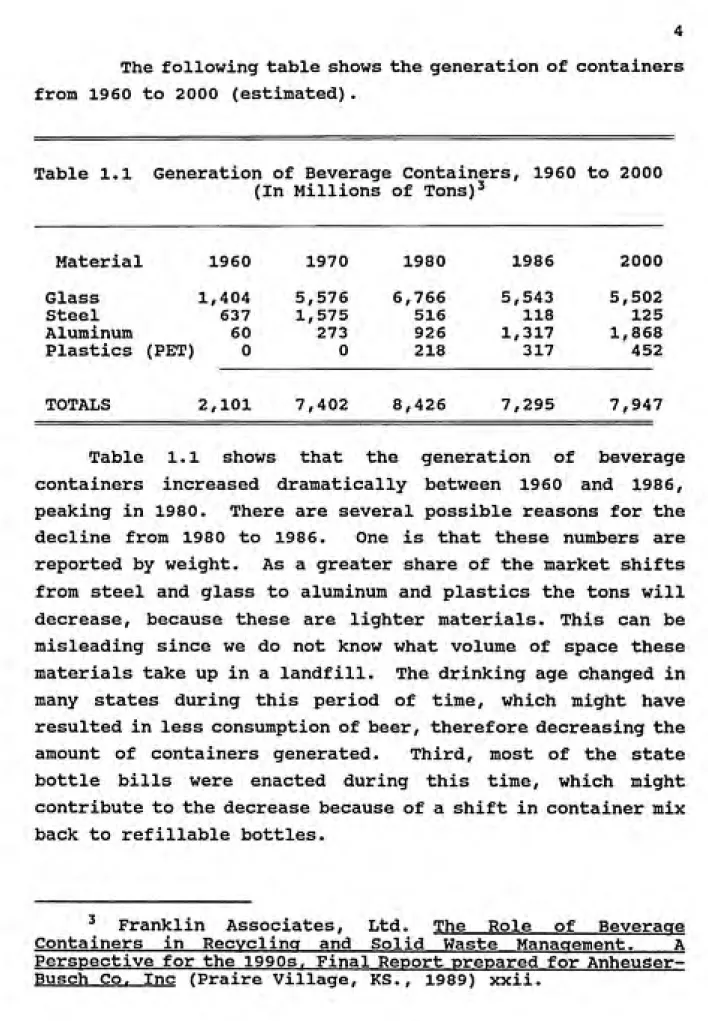

from 1960 to 2000 (estimated).

Table 1.1 Generation of Beverage Containers, 1960 to 2000

(In Millions of Tons)^

Material 1960 1970 1980 1986 2000

Glass * ' 1,404

Steel 637 Aluminum 60

Plastics (PET) 0

5,576 6,766 5,543 5,502

1,575 516 118 125

273 926 1,317 1,868

0 218 317 452

TOTALS 2,101 7,402 8,426 7,295 7,947 Table 1.1 shows that the generation of beverage containers increased dramatically between 1960 and 1986, peaking in 1980. There are several possible reasons for the

decline from 1980 to 1986. One is that these numbers are

reported by weight. As a greater share of the market shifts

from steel and glass to aluminum and plastics the tons will

decrease, because these are lighter materials. This can be misleading since we do not know what volume of space these

materials take up in a landfill. The drinking age changed in

many states during this period of time, which might have

resulted in less consumption of beer, therefore decreasing the

amount of containers generated. Third, most of the state

bottle bills were enacted during this time, which might

contribute to the decrease because of a shift in container mixback to refillable bottles.

' Franklin Associates, Ltd. The Role of Beverage

Containers in Recycling and Solid Waste Manacrement. A

Perspective for the 1990s. Final Report prepared for

Beverage container production will continue to increase

over the next few years. As Table 1.1 shows, the estimated increase from 1986 to 1990 was 8.9%. The number of bottlers also has decreased dramatically. In the soft drink industry the number of manufacturers dropped from 6118 in 1940 to 1011

in 1989.^ The remaining bottlers have increased in size and

serve larger areas, making nonreturnable bottles more convenient.

1.3 States that have Beverage Container Deposit Laws

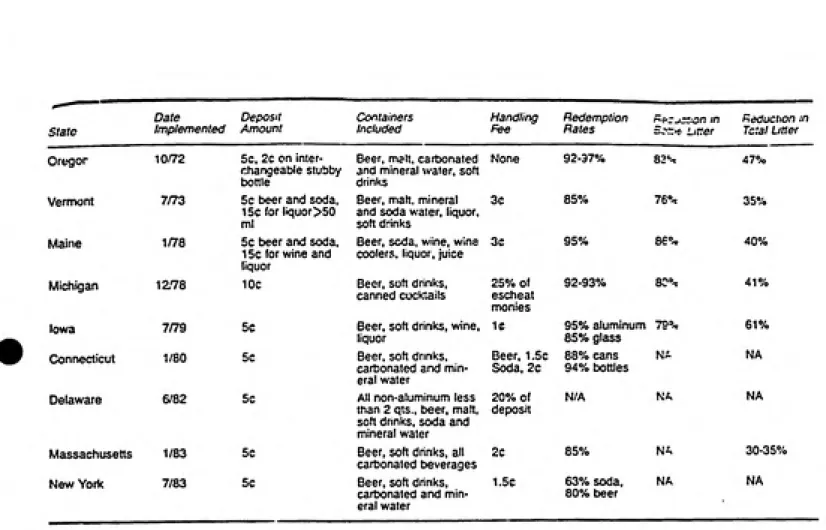

Nine states have adopted Beverage Container Deposit Laws. Table 1.2 shows the provisions of each law. This table

illustrates the wide variety of materials that can be collected and that a deposit system can be one or two - tier.

Two - tier systems have a lower deposit on bottles that can be interchanged between manufacturers.

One could argue that the California Beverage Container

Recycling and Litter Reduction Act should be included in this

chart. The major reason California has been excluded from

this chart is that there is no deposit per se. The containers can be redeemed by consumers for 2. 5<: for containers which are less than 24 ounces and 5<: for containers greater than 24 ounces. Distributors pay the state a 2C and 4<: processing fee

respectively for every beverage they distribute. The beverage

industry likes this initiative better than traditional bottle bills because the redemption is handled in state - certified

redemption centers and administrative costs are covered by the

money paid by the distributors that the consumers do not collect. This money also helps subsidize grants to nonprofit

''" Soft Drink Trends," Beverage Industry Annual Manual

Table 1.2 Beverage Container Deposit Laws^

state Date Implemented Deposit Amount Containers Included Handling Fee Redemption Rates '^rr^-r.-or in S.-'r^ Lirter Reduction :n Tctal LitterOregor 10/72 5c. 2c on inter¬

changeable stubby

tx)tlle

Beer, malt, cartKDnated

and mineral water, soft

drinks

None 92-37% 83=--. 47%

Vermont 7/73 5c beer and soda,

15c for liquor >50 ml

Beer, malt, mineral

and soda water, liquor,

soft drinl<s

3e 85% 76% 35%

Maine 1/78 5c beer and soda, 15c for wine and

liquor

Beer, soda, wine, wine

coolers, liquor, juice

3c 95% 86% 40%

Michigan 1278 10c canned cocktailsBeer, soft drinks.

25% of escheat monies

92-93% 80% 41%

Iowa 7/79 5c Beer, soft drinks, wine, liquor

1C 95% aluminum

85% glass

79% 61%

Connecticut 1/80 5c Beer, soft drinks,

carbonated and min¬

eral water Beer, 1.5c Soda, 2c 88% cans 94% bottles NA NA

Delaware 6/82 5c All non-aluminum less

than 2 qts., t>eer, malt, soft drinks, soda and

mineral water

20% of

deposit

N/A NA NA

Massachusetts 1/83 5c Beer, soft dnnks, all carbonated tieverages

2C 85% NA 30-35%

New York 7/83 5C Beer, soft drinks,

carbonated and min¬ eral water

1.5e 63% soda,

80% beer

NA NA

^Patricia Franklin, " Bottle Bill: Litter Control Measure

related programs. The retailer is totally left out of the

cycle and the distributors do not have to worry about

transporting bottles or having to take more bottles back than

they sold. The return rate is approximately 85% overall.^

For the purposes of this paper this system is not considered

a BCDL, because of the lack of the deposit side of the program.

Arguments often used against deposit systems are that

they are inconvenient and that people will refuse to

participate.^ However, redemption rates in the states that

have beverage container laws are between 63 percent and 97

percent.® The systems seem to be convenient or at least have

enough incentive built in for people to use them. Some people

will argue that just because bottles are getting back, a few people could be doing the returning. If they are being

returned by a third party, however, there might still be social value associated with the system. For example, if homeless people collected bottles which have been discarded and return them it might be a source of income for them. Gershman, Brickner & Bratton conducted a survey in which they asked residents of Islip, NY if they redeemed their bottles. Depending on the material of the bottle, the percentage of people who claimed that they redeemed their beverage

^Container Recycling Institute. Beverage Container

Deposit Systems in the United States (Washington D.C., 1992)

np.

^W.K. Moore and D.L. Scott, "Beverage Container Deposit

Laws: A Survey Of the Issues and Results," Journal of Consumer Affairs 17.1 (1983) 64.^These numbers came from state agencies in the respective

containers ranged from 74 - 80%.' Redemption rates do not

seem to be affected by deposit levels over 2<:. This statement

is based on studies in Michigan, Oregon, and Europe. A

possible explanation for this phenomenon is that "the

consumer's opportunity cost for returning containers is in

excess of the cost of forfeiting a deposit of two to ten

cents". ^°Beverage Container Deposit Laws were originally passed to

help control litter. The idea was that beverage containers

would be too valuable to throw out the window. Money would

also be saved on litter pick-up, and injuries due to broken

glass would decline. Table 1.2 illustrates that bottle bills

are effective as a deterrent of litter. Bottle litter has decreased between 76 and 88% while total litter has been

reduced between 30 and 47%." This helps explain why total

litter is reduced. Several BCDL states confirmed that the cost for litter pick-ups decreased after the law was enacted. (A

detailed explanation of various litter surveys can be found in

Appendix A).

The decline in available landfill space, and the

difficulties in siting new landfills and incinerators have

focused the nation's attention on waste reduction andrecycling. Senate Bill 111 passed in North Carolina requiring

'"Impact of Container Deposits on Curbside Recycling: Two

Case Studies", (Falls Church, VA: Gershman, Brickner, & Bratton, July 1991): V-5.

^°William Lesser and Ananth Madhaven, "Economic Impacts

of a National Deposit Law: Cost Estimates and Policy

Questions." Journal of Consumer Affairs 21.1 (1987) 132.

"These numbers came from a wide variety of state agencies

which are documented in Beverage Container Deposit Systems in

the United States which is written by the Container Recycling

1993.^^ Proponents of the BCDL suggest that bottle bill

legislation will help municipalities reach the 25% recycling

goal. If materials collected in the BCDL system are not

counted toward materials recycled then a BCDL would be a

detriment to counties trying to meet this goal.

BCDL supporters suggest that since BCDLs cause a

container mix shift toward returnable bottles, and because of

the high return rate which efficiently collects bottles for

recycling, solid waste is decreased. (See Appendix B for a

discussion of the effects of BCDLs on solid waste in Michigan

and Maine).

1.4 North Carolina's Interest in Beverage Container

Deposit LawsTable 1.2 shows that no new Beverage Container Deposit

Laws have been passed since 1983. However, due to the

reduction of landfill space and the difficulty of siting new

solid waste disposal facilities, a new interest in methods

that increase recycling has emerged. This interest includes

beverage container deposit laws. Proponents see this as a way

to promote recycling and source reduction. Source reduction

occurs because there is often a shift back to returnable

containers. Legislators in both the federal government and in

North Carolina have tried to pass Beverage Container Deposit

Laws during the last ten years.

At the national level, bottle bills have been introduced

almost every year since 1977. The major supporter of the

bills at the national level has been Rep. Paul Henry (R-MI).

^^Lee M. Mandell and Matthew R. Banks,What are We Doing

In 1991 a bottle bill was introduced to be considered as an

amendment to the reauthorization of RCRA." The provisions

of this proposed bill are presented in 40CFR part 244. The

intent is to reduce waste by making all beverage containers

returnable and encouraging the recycling of beverage

containers. The beverages included in this bill are

"carbonated natural or mineral waters, soda water and similar

carbonated soft drinks; and beer or other carbonated malt

drinks in liquid form^^". The deposit level is set at 5<:

except in areas with a lower deposit already. There is no

handling fee proposed. The Comprehensive Recycling Act of

1991 (H.R. 945) Which would set recycling goals in programs of

the state's choice is an alternative to the BCDL.^^ It

requires that states offer recycling to 20% of their state

within two years of the bill's passage. The beverage industry

supports this bill. A bottle bill was voted on July 2,1992 by

the full Energy and Commerce Committee and was defeated by a

27 to 17 vote.

In North Carolina beverage container deposit laws have

been introduced 24 time, first in 1969. Table 1.3 lists all

the bills that have been introduced on the subject since 1969.

The last bill. House Bill 1007 introduced by Karen Gottovi

(D-Wilmington) in 1991, was defeated. It would have enabled the

Legislative Research Commission to study the issue of a

beverage container deposit law.

^^Stephen Barlas, "Beverage Industries Support Bottle Bill

Challenger," Beverage World June 1991: 65.

^^40CFR Ch 1 (7-1-91 Edition) Part 244 - Solid Waste

Management Guidelines for Beverage Containers, 279.

15

Table 1.3 Bottle Deposit Legislation in North Carolina

Year______Bill No. Short Title____________________Disposition

1969 H 1017 Soft Drink / Bottle Deposit left in committee

S 791 Soft Drink Containers, cleaning Rat. Ch. 1068

1971 S 177 Deposit on Soft Drink or Beer Cans/Bottles unfav.

1973 H 1329 Redemption Beverage Containers reptd. unfavorably

S 828 Senate version of H 1329 left in committee

S 959 Control Beverage Container Litter left in committee

1975 H 457 Beverage Container Return postponed indef. S 365 Senate version of H 457 reptd. unfavorably 1977 H 697 Refund Required on Drink Bottles reptd. unfavorably H 1181 Drink Bottle Deposit Referendum reptd. unfavorably H 1203 Drink Bottle Tax Fund, Uses reptd. unfavorably H 425 Litter Control Resource Recovery left in Sen. Comm. 1979 H 857 Deposit for Beverage Container reptd. unfavorably

H 1419 Bottle Bill Referendum Funds reptd. unfavorably 1981 H 513 Beverage Container Referendum reptd. unfavorably

H 1292 LRC Studies Res. 61 Sec 1 (14)

1985 H 1141 Soft Drink Bottles / Alcohol in Parks reptd. unfav.

1987 H 1212 Recyclable Containers Required left in committee

1989 H 1225 Containers; Deposit(p.70) left in committee S 958 Solid Waste Advance Fee left in committee H 2365 Raise Soft Drink Tax left in committee

1991 H1007 Plastic/Glass Container Deposit postponed indef. H 97 Uniform Color Disposable Glass left in committee

S 229 Simplify ^oft Drink Tax(study) Incorp. in Ch.754

Source: Computer Search Completed by the North Carolina

II. THE EFFECTS OF BEVERAGE CONTAINER DEPOSIT LAWS ON

CURBSIDE RECYCLING

One of the arguments most frequently used against

beverage container deposit laws is that they have a negative

impact on curbside recycling. One of the strongest arguments

invoked is that a BCDL pulls aluminum, which has the most

stable and profitable market of recyclable materials, out of

the recycling waste stream. The revenues gained from the sale

of recyclables help offset some of the costs of running a

recycling program. Proponents of BCDLs, however, argue that

the amount of materials pulled into the waste stream are

increased by having a dual system. They suggest that

collection costs are avoided since redemption centers are at

retailers where the consumer already shops. They also suggest

that there is no cost to the municipal government, so they

argue that BCDLs are cost-effective ways to increase the

amount of recyclables.

Since the nine states with BCDLs had enacted there laws

before curbside recycling was popular, there are no actual

case studies available. In this paper, I use five studies

which estimated the effects of BCDLs on curbside recycling, in

order to develop a model to determine the structure of a model

that will be used to estimate the effect that a beverage

container deposit law would have on curbside recycling,

specifically in Orange County, North Carolina. These studies

include one conducted by Franklin Associates, LTD. for

Anheuser-Busch Companies,Inc; one conducted by the National

Container Recycling Coalition; one conducted by Gershman,

Brickner & Bratton, Inc. for the National Soft Drink

Association; one by the Tellus Institute; and one by the

Florida Public Interest Research Group. I chose to examine the

results of these studies when fighting BCDLs, for example, in

the pamphlet "Why Comprehensive Recycling Is a Solid Winner.

Why Forced Deposit Laws are a Solid Waste" which distributed

by the National Soft Drink Association all three studies are

guoted to show that comprehensive recycling costs more when a

BCDL is in place. I chose the study by the National Container

Recycling Coalition (Pat Franklin) because it shows that a

dual system can be cheaper than a single comprehensive

recycling system and because Rep. Paul Henry has quoted it at

a congressional hearing on a national beverage container

deposit law. I chose the FIPIRG because it supported the

NCRC's findings. In the next five sections, each study is

examined in depth.

2.1 The Franklin Associates, LTD. Model

The report, The Role of Beverage Containers in Recyclincf

and Solid Waste Management A Perspective for the 1990s, was

prepared by Franklin Associates, LTD. for Anheuser-Busch in

April of 1989. It examines the economic costs associated with

running a dual system which includes a BCDL and comprehensive

curbside recycling compared to a single comprehensive curbside

recycling program. They applied their model to New York State

and Vermont. The model estimated amounts recycled, operating

and processing costs, and capital costs. These values were

estimated for three different size communities and then a

weighted average was calculated to determine these figures on

14

2.1.1 Structure and Assumptions

This is the most complicated model discussed in this

chapter. The seven major assumptions made by Franklin

Associates, LTD are listed below:1) The recycling program would be operated statewide and

would be mandatory. A participation rate of 80-90% is

needed to sustain this model. Also the capture rate of

recyclables must be high (85-100%).

2. Adequate capital investment will be made to collect and

process recyclable materials. ,

3. Newspapers, glass containers, plastic containers,

and aluminum cans will be collected in the program.

4. When mandatory recycling is the only system in place,

buy-back centers, drop-off centers and scrap dealers

will operate.5. "Revenues realized from the mandatory recycling paxpam

are for fully-prepared materials brokered to or delivered

directly to end users of recovered materials. Programs

structured to operate via intermediate processing facilities

(IPCs) where materials flow to a scrap dealer for further

preparation and marketing will realize a lower revenue."^*

6. All materials will be accepted by the market, "however

prices will fluctuate cyclically for all materials.''^" The

most dramatic fluctuations will be for paper which will

^^Franklin Associates, LTD. 50,

fluctuate from negative values to $50 a ton.

7. "Where beverage containers deposit laws are in effect,

there will be two distinct recyclable materials

recovery systems in place, one operating via retail

stores and wholesalers and one via

municipally-sponsored recovery programs. (In fact, deposit-type

beverage containers could be placed in a mandatory

recycling program because the citizen values

convenience more highly than deposits) . "^°.

2.1.2 Franklin Associates, LTD's Findings

Tables 2.1 and 2.2 show the final calculations of cost

per ton for the New York and Vermont municipal recycling

markets at 80 and 90% participation rate. The Franklin

Associates, LTD. conclude that a dual system costs more per

ton than a single municipally based program. The amount

collected in the municipal recycling program is reduced for

the curbside program, therefore, the operating costs decrease.

The material revenue costs decrease more though because

aluminum is the highest revenue generator and almost all of

it goes to the BCDL. In Tables 2.1 and Table 2.2 the quantity

of recyclables collected in the municipal recycling program

decrease because the beverage containers are diverted to the

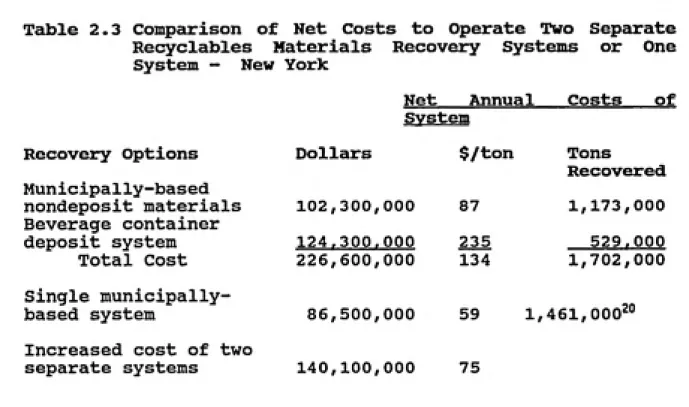

BCDL system. Tables 2.3 and 2.4 show that more materials are

collected in a dual system overall. They also show that

curbside recycling programs' cost-effectiveness depend on the

amount of materials collected and on the revenue they

generate.^' The Franklin

^^Franklin Associates, LTD 49-50,

SUMMARY OF NEW YORK COMPREHENSIVE MUNICIPAL RECOVERY PROGRAM*8 CAPITAL COSTS«

ANNUAL OPERATING COSTS, REVENUES, NET OPERATING COSTS, AND

RECYCLABLES RECOVERED WITH AND WITHOUT A BCDL IN PLACE

(In dollars and tons)

Category

Capital Investment

Operating Costs

Revenue @ 90% Participation

Net Operating Costs

Quantity of Recyclables

Recovered @ 90% Participation

tonsNet Operating Costs - $/ton

No BCDL

287,018,000

180,258,000"

93,800,000

86,458,000

1,461,000

59.18

With BCDL

287,018,000

148,245,000

45,930,000

102,315,000

1,173,000

87.22

Dlff«renoa

(32,013,000)

(49;870,000) *

15,857,000

(288,000)

28.04

Revenue § 80% Participation

67,885,000

28,975 ,,000

(38,910,000)

Quantity of Recyclables Recovered

@ 80% Participation - tons

972,000761,000

211,000Source: Franklin Associates, Ltd.

SUMMARY OF VERMONT COMPREHENSIVE MUNICIPAL RECOVERY PROGRAM* 8 CAPITAL

€

SOBT»t

ANNUAL OPERATING COSTS, REVENUES, NET OPERATING COSTS, AND

RECYCLABLES RECOVERED WITH AND WITHOUT A BCDL IN PLACE

(In dollars and tons)

Categoiry

Capital Investment

Operating Costs

Revenue @ 90% Participation

Net Operating Costs

No BCDL

11,213,800

5,217,000

2,443,000

2,774,600

With BCDL

11,213,800

4,234,000

881,0003,353,000

Differenoa

(983,000)

(1,562,000)

579,000Quantity of Recyclables

Recovered ©90%

Participation - tons

Net Operating Costs - $/ton

27,600

100.52

20,900 160.43

(6,700)

59.91

Revenue 6 80% Participation

Quantity of Recyclables

Recovered § 80%

Participation - tons

1,827,000

17,300

503,000

12,300

(1,324,000)

(5,000)

Table 2.3 Comparison of Net Costs to Operate Two Separate

Recyclables Materials Recovery Systems or One

System - New YorkNet Annual Costs of

Recovery Options Municipally-based nondeposit materials

Beverage container

deposit system

Total Cost

Single municipally-based system

Increased cost of two

separate systems

system

Dollars $/ton Tons

Recovered

102,300,000 87 1,173,000

124,300,000 235 529.000

226,600,000 134 1,702,000

86,500,000 59

1,461,000^°

140,100,000 75Source: Franklin Associates, Ltd. 95,

20,

Table 2.4 Comparison of Net Costs to Operate Two Separate Recyclables Materials Recovery Systems or One

System - Vermont^^

Net Annual Costs of

Recovery Options

Municipally-based

nondeposit materials Beverage container deposit system

Total Cost

Single

municipally-based system

Increased cost of two

separate systems

System

Dollars $/ton

3,335,000 160

2.575,000 121

2,928,000 140

2,775,000 101

3,153,000 39

Tons

Recovered

20,900

21.300

42,200

27,60022

Source: Franklin Associates, Ltd. 93.

^^Tonnage Recovered in private program is excluded;

refillable bottles are also excluded.

Associates, LTD. concluded:

"Comprehensive materials recovery programs are more cost-effective when they include beverage containers... There would be additional overall

savings in a single system because the beverage

container deposit system operating independently

has a net cost also. In either case the

unrecovered costs are borne by the citizens ||23

The Franklin Associates, LTD. also conclude that a single

comprehensive system is more cost efficient than a dual system.

2.1.3 Analysis of the Franklin Associates, LTD.

Study

The beverage industry frequently quotes this study to support their opposition to BCDLs. Supporters of BCDLs feel that the bias of this study can be seen in the executive summary which states that "An opportunity of uncommon circumstances now exists for the beverage industries and packagers to participate in comprehensive recyclable materials

recovery programs and, at the same time, work toward solutions

that could phase out beverage container deposit laws." One major criticism of this study is that the participation rate of 90% is not realistic. It is more likely that New York and Vermont could reach levels comparable to those in model

recycling programs like the one in Seattle, Washington where

they are recycling around 40%. Critics of this study suggest that if participation rates are low in curbside programs then the BCDL becomes more important due to the fact that more

materials are collected in a dual system. As we saw in Chapter

1 return rates are extremely high for BCDL.

The Franklin Associates factor a cost for a BCDL into

their cost analysis. This figure is based on costs that are

incurred by the beverage industries (See Appendix D).^^ The

Franklin Associates suggest that the costs looked at in this paper are those that the average citizen pays. They suggest that taxpayers will have to pay for increased comprehensive

recycling as well as costs incurred by the beverage industries

(these costs would be seen in higher prices and possibly less

consumption resulting in lost sales and excise, and in the case of alcoholic beverages, taxes). Pat Franklin of the National Container Recycling Coalition, suggests that if only the costs to the municipality are considered, and if one

assumes that there is no cost associated with a BCDL for the

municipality (this point will be more fully scrutinized in the

Rhode Island Model section) the costs to Vermont to run a dual program would be $22/ton and the cost to New York would be

around $60/ton.^^

One other point Ms. Franklin makes is that the capital

investment needed to sustain a program with these costs is probably not feasible. The Franklin Associates projected $267

million capital investment for the New York comprehensive

recycling program and an $11 million capital investment in Vermont. New York allotted $26 million and Vermont allotted $3.5 million for recycling efforts statewide in 1989. If the

Franklin Associates estimates are right the governments of those state would have to pay $241 and $5.2 million

respectively to run a comprehensive recycling program.^^

^^Mandell and Banks 10.

^^ Pat Franklin, Critique of the Franklin Associates.

LTD.Study. National Container Recycling Coalition, September18, 1989. 26

2.2 The Gershman, Brickner & Bratton, Inc. Study

In July 1991 Gershman, Brickner & Bratton, Inc. completed

a study. Impact of Container Deposits on Curbside Recycling;

Two Case Studies for the National Soft Drink Association.

2.2.1 structure and Assumptions

This study compared the town of Islip, New York with

Anne Arundel County, Maryland. GBB analyzed the economic

effects of the BCDL in Islip and estimated the effects in Anne

Arundel based on actual cost figures from 1990. A detailed

description of their model is shown in Appendix D. The

results of the analysis are shown in Table 2-5 and Table 2-6.

One assumption they make but do not state is that all the

waste that is collected in the BCDL would be transferred to the recycling program.GBB then developed a model for a generic community of

100,000 people with 40,000 households. The major assumptions

in this study are that the recycling quantity per household is

6.4%, that processing costs are 50 dollars per ton, and that

collection costs are 2 dollars per household per month. The

detailed analysis of the generic community is shown in

Appendix F. The findings of the study for a community which

Table 2.5 Islip Residential Recycling System Revenues

and Costs With and Without BCDL in 18,991

Households (1990)Revenues or (Costs)

Paper

Non-Deposit Containers

Deposit Containers Total Revenues

With BCDL

$(55,599) $ 24,578

$ 26.338

$ (4,683)

Without BCDL

$(55,599)* $ 24,578

$107.804

$ 76,783

Costs

Collection

Processing

Operating Costs

Revenue or (Costs)

Net Program Costs

With BCDL

929,311

365.500

$1,299,494

$(4.683)

$1,299,494

Paper had a negative value during 1990.

Without BCDL

929,311

415.700

$1,268,228

- $76.783

$1,268,288

Table 2.6 Anne Arundel Residential Recycling System Revenues

and Costs With and Without BCDL

(1990) Revenues or (Costs)

Paper

Non-Deposit Containers Deposit Containers

Total Revenues

With BCDL

$ 6,219 $ 27,556

S 22.715

$ 56,490

Without BCDL

$ 6,219 $ 27,556

$ 90.982

$124,757

Costs With BCDL Without BCDL

Collection

Processing

Operating Costs

Revenue

Net Program Costs

316,777

231.158

', 547,935

- $56.490

$419,455

316,777

274.995 591,772

S467.015

$467,015

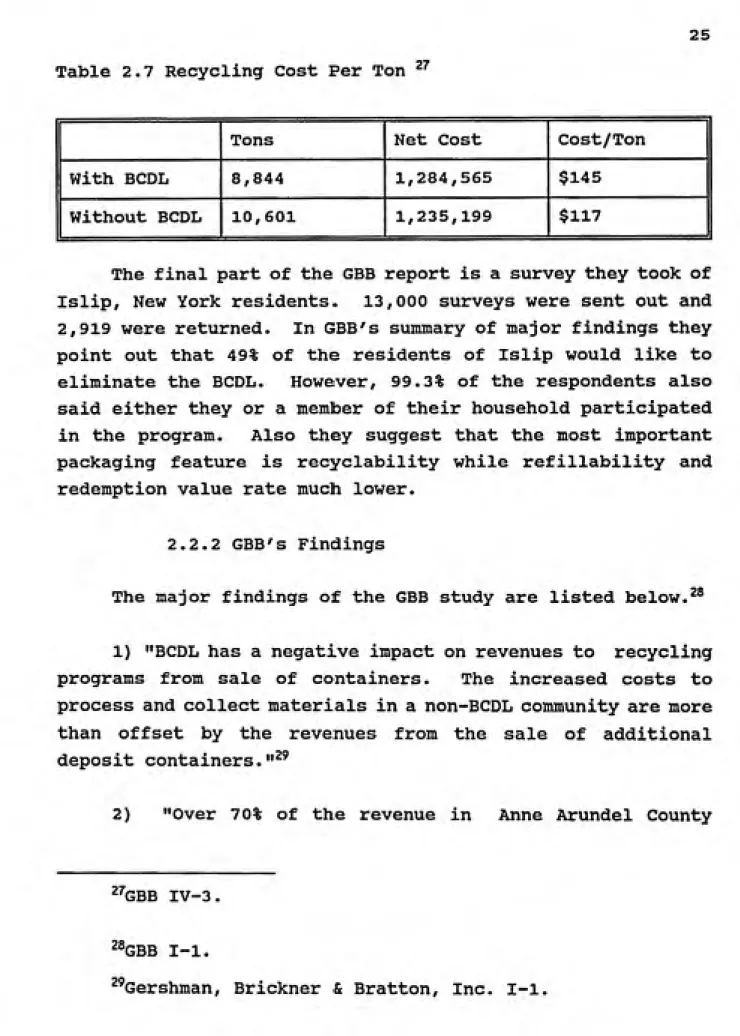

Table 2.7 Recycling Cost Per Ton ^^

Tons Net Cost Cost/Ton

With BCDL 8,844 1,284,565 $145

Without BCDL 10,601 1,235,199 $117

The final part of the GBB report is a survey they took of

Islip, New York residents. 13,000 surveys were sent out and

2,919 were returned. In GBB's summary of major findings they

point out that 49% of the residents of Islip would like to

eliminate the BCDL. However, 99.3% of the respondents also

said either they or a member of their household participated

in the program. Also they suggest that the most important

packaging feature is recyclability while refillability and

redemption value rate much lower.

2.2.2 GBB's Findings

The major findings of the GBB study are listed below.

281) "BCDL has a negative impact on revenues to recycling

programs from sale of containers. The increased costs to

process and collect materials in a non-BCDL community are more

than offset by the revenues from the sale of additional

deposit containers."^'

2) "Over 70% of the revenue in Anne Arundel County

2^GBB IV-3.

28,

GBB I-l.

29,

comes from the sale of beverage containers."'° This is

calculated by taking the $90,982 worth of revenue created by

deposit material and dividing by the total revenue figure of

$124,757. The revenue from deposit containers offsets 15% of

the total costs of the curbside program.

3) The recycling rate is 18% and the redemption rate is

1.6% in Islip. The recycling rate in Ann Arundel, MD. is

17.7%.4) With a dual system, 23% of beverage containers still

end up being disposed.

5) The generic analysis shows that a community can

offset up to 12% of its operating costs from the sale of

beverage containers.

2.2.3 Analysis of GBB's Findings

The analysis of the effect of a BCDL on Islip, New York

is different then the rest of the studies examined in thischapter due to the fact that it looks at a BCDL already in

place and what would happen if it were removed. The structure

of this study is to assume that all of the materials collected

in the beverage container deposit system would be transferred

to the curbside recycling program. However this assumption

probably overestimates the number of beverage containers that

would return to the curbside program. Some people might not

be served by the curbside program and would be unwilling to

use drop-off services, and some people might not be willing to

recycle without the economic incentive. Even so, the

processing costs should have increased proportionately to the

amount of materials added to the system so the numbers

generated should be valid. Also Islip might not be a typical

situation since it is known for its garbage problems.

2.3 The Rhode Island Model

Patricia F. Franklin of the National Container Recycling

Coalition, presented a paper at the Windstar in Washington

Conference on September 15, 1990, called "Curbside Recycling

and Deposits— Removing More from the Waste Stream for Less**.

A model which is similar to the GBB model is used to determine

the effect of a BCDL on curbside recycling in Rhode Island for

four scenarios. The scenarios are a Curbside program

(residues being landfilled), a Curbside program (residues not

being landfilled), a Curbside/BCDL program (residue being

landfilled), and a Curbside/BCDL program (residues not being

landfilled). Residues are primarily made up of contaminated

glass which some reports say is being landfilled.

2.3.1 Structure and Assumptions

The major assumptions are:

1) The recycling program would serve 660,000 residents of

Rhode Island (approximately half the state) in one

comprehensive program.

2) The data for only a curbside program are projections

for 1990 made by the Johnson Material Recycling Facility

Financial Analysis.

3) In a dual system no beverage containers end up in the

curbside recycling program.

4) There is no cost to the municipal government for

5) 85% of beverage containers are returned through the

BCDL.

6) Operating and per-ton collection costs remain the same

under a dual system ($82/ton).

7) Total beverage containers generated annually are

estimated to be 306,240,000 which is based on a figure of 464

per capita. The markets shares of each container are shown in

table 2.8. They are based on statistics used in "The Role of

Beverage Containers in Recycling and Solid Waste Management"

which was written by the Franklin Associates, LTD.

8) The revenues for the materials are as follows:

Aluminum = $958 per ton Glass = $48 per ton

Plastic (PET) = $157 per ton

2.3.2 Findings of the Rhode Island Study

The major finding of this study is that a dual system can

be cheaper on a cost-per-ton basis than a single curbside

recycling program as shown in Table 2-8.^' This table shows

the results when the residues are recycled. The more

realistic scenario is that the residues will be landfilled.

Some bottles may be unrecyclable due to dirt or breakage. The

National Container Recycling Coalition's estimation of cost

per ton and tons collected when the residues are landfill is

shown in Table 2.9.^^

^^Patricia Franklin 48.

32t

ͣ

^Pat Franklin, Curbside Recycling and Deposits —

Table 2.8 Comparison of Rhode Island's Curbside Recycling

Program and a Curbside/BCDL Program

Material

Rhoae Island Curbside Program

(Protected 1990 Figures) Combined Curbside Recycling/Bottle BHi________{Estimated Figures)_______ Tons Cost of Tons Cost of

Removed Revenue Collection (1) Removed Revenue Collection

Newspaper 27,800

Aluminum HOPE PET Tin Glass Residue Totals 625 725 800 2,600 6,700 7.500 43,600 599,000 106,500 125,300 39,000 322,700 0 2,291,300 51.500 59,200 65,900 214,300 552.200 618.200 27.800 2.666 725 1.562 2.600 22.605 (2) 3,450 43.600 0 106.500 0 39,000 147.936 0 2.291,300 0 59.450 0 213.200 252.724 282.900

46,750 51,236,100 $3,853,400 61,408 $337,036 $3,087,874

Operating costs

Collection costs

Subtotal operating cos:

Revenue

Net operating cost Cost per ton of

material removed

Curbside Program

Without Bottle Bill

$1,779,600

•*ͣ $3,853,400 $5,633,000 -$1,236,100

$4,396,900

$94.05

Combined Curbside

Bottle Bill Program $1,779,600

$3,087,874 $4,867,474 -$ 337.036

$4,530,438 $73.77

(1) $82.42 was used as Vte average cost of collection per toa l>ased on total collection costs of $383,500

in the Johnston MRF Financial Analysis. Column may not sum to total due to rounding.

(2) 19,523 tons oollectec through BCDL 3.082 tons collected through curbside program. Assumes that

46% of trie glass in the curbside program is non-t>everage container glass (per "U.S. kxJustrial Outlook

Table 2.9 comparison of Rhode Island's Curbside Recycling

Program and a Curbside/BCDL Program When Residues are

Landfilled

Rhode Island's

Curbside Program

Estimated Figures |

for a Combined Curbside/BCDLProgram

Total Tonnage 39,250 57,958

Cost per Ton $112.02

$78.17 1

2.3.3 Analysis of the Rhode Island Study

The reason the dual system is cheaper is the assumption

that there are no costs associated with a BCDL. However,

there are costs at all levels in the beverage industry, and

there are administrative costs associated with implementing a

BCDL. Temple, Barker and Sloan estimate that the

administrative costs of the BCDL range from $l,700-$57,000

annually for the nine bottle bill states. Some of these

administrative costs include regulatory development, and

information and enforcement. These costs include salaries for

either full or part-time employees who provide regulatory

support, answer consumers' questions and provide information,

or for employees who enforce the regulations.^^ Most of

these tasks may be executed at the state level. If that is

true then the assumption that there is no cost for a BCDL to

the municipal government may be valid. If the costs to the

municipality running the curbside program are evaluated, only

the materials collected from the curbside program should be

considered in the cost per ton analysis. Below are the

33n

^Temple, Barker and Sloan, Economic Impacts of a National

Beverage Container Deposit Lav, Prepared for the National Soft

results of looking at the problem in this context. A detailed

explanation of calculation of these nvunbers are shown in

Appendix G.

Table 2.10 Cost to the Municipal Recycling Program in

Rhode Island""""

Tons Removed in

Curbside Program

Only

Cost per Ton

Curbside Program (residues

landfilled)

39,250 $112.02

Curbside/BCDl

(residues landfilled)

34,250 $135.12

Curbside Program (residues not landfilled)

46,750

$94.05 1

Curbside/BCDL

(residues not landfilled)

37,657 $122.74

The costs of running a dual program becomes more

expensive when the situation is framed in this manner. The

costs to run a dual program increase by 20% when residues are

landfilled and by 31% when they are recycled. The material

collected in a dual system also increases. When the residues

are landfilled the total amount of recyclables in the system

increases by 48% and when residues are recycled they increase

by 31% (See Table 2.9 for total amount collected in a dual

system) . The most likely scenario is the one where residue is

landfilled. In the BCDL system less residues are generated due

to the fact that the collection process under a BCDL is more

efficient. In other words, if a person tries to return a

bottle that is not properly cleaned for recycling under a

BCDL, the retailer will most likely reject the bottle and not

Rhode Island has an unusually high percentage of glass

bottles. Approximately 30% of their beverage containers are

glass bottles which is above the national average of 20%. In

other states where the glass percentage is lower, more

beverages would be packaged in aluminum or plastic. Both of

these materials have higher revenues and would probably hurt

the recycling program more under the bottle bill. Finally Ms.

Franklin suggests that the increased tonnage in a dual program

would result in an avoided disposal cost of between $448,000

and $570,000 (with a tipping fee of $30 a ton). The issue of

avoided disposal costs is discussed more thoroughly in the

next study.

2.4 The Florida Public Interest Research Group Study

Bill Wood of the Florida Public Interest Research Group

Educational Fund (FIPIRG) conducted a study which is very

similar to the study conducted by Pat Franklin of the National

Container Recycling Institute (in fact the CRI and the

National Environmental Law Center contributed research

assistance). It projects the effects that a BCDL would have

on curbside/drop-off recycling in four communities in Florida.

2.4.1 Structure and Assumptions

The impacts of a beverage container deposit law on

curbside recycling in four cities in Florida were assessed.

The four cities studied were Tallahassee, Gainesville,

Hialeah, and Miami. The first assumption is that all

beverage containers are pulled from the curbside programs.

Since the author had difficulty collecting data for the actual

scrap revenues and other values, he used the values given in

the GBB study analyzed above. The author suggests that the

case scenario. One of the major criticisms he has of the GBB

study is that it fails to take into account the avoided

disposal costs. In this study avoided disposal costs are

estimated as the avoided landfill tipping fee. Mr. Wood feels

these are conservative estimates of avoided disposal costs

because they do not take into account lowered processing,

transportation, and other solid waste management costs. The

information for material tonnage was taken from actual data

for the county and then a percentage based on population was

calculated and used to determine the amounts of materials generated for each city.

2.4.2 Finding of the Florida PIRG Ed Fund Study

Tables 2.11 - 2.14 show the results of this study. The

details of how these numbers were calculated are shown inAppendix H. The data show that a dual program is less

expensive to operate on a cost per ton basis when avoided

disposal costs are subtracted. These are higher in a dual

system because more waste is diverted in the dual system. The

Florida PIRG Education Fund conclude that more waste is

diverted in a dual system, and the government management costs

are decreased. They estimate beverage container recycling

will quadruple in Florida if a BCDL is passed.

2.4.3 Analysis of the Fl. PIRG Ed. Fund Study

The two assumptions that influence the results of this

Table 2.11 City of Tallahassee Recycling: Government

Costs & Revenues in Calendar Year 1991I. Curbside without Bottle Bill (as exists now)

II. As Projected via Curbside and Bottle Bill Combined

I. Curbside II. Curbside and

W/O BB BE Combined

COSTS/REVENUES

Collection Costs $644,823

Processing Costs 129.954

Total Operating Costs $774,777 $728,290

Revenue from Sale of - 198,397 - 91,263Scrap Materials

---$576,380 $637,027

Avoided Disposal Costs - 82.152 -114.948

Net Operating Costs $494,228 $522,079

TOTAL TONS DIVERTED: 4,564 6,386Table 2.12 City of Gainesville Recycling: Government

Costs & Revenues in Calendar Year 1991I. Curbside without Bottle Bill (as exists now)

II. As Projected via Curbside and Bottle Bill Combined I. Curbside II. Curbside and

w/o BE BE Combi ned COSTS/REVENUES

Collection Costs $260,000

Processing Costs 71.000

Total Operating Costs $331,000 $311,000

Revenue from Sale ofScrap Materials:

Newspaper (ONP) 7,047

---Plastic

PET ---HDPE

Glass 14,230

Aluminum 6,752 Metal 1,801 - 39,970

$291,030 Avoided Disposal Costs - 120.960

Net Operating Costs $170,070

TOTAL TONS DIVERTED: 2,688GOV'T COST/TON DIVERTED: $63

Source: Florida Public Interest Research Group 61.

3, 7,

403 392

1,331 - 22,366

$288, 634 -228. 634

$103, 774

4. 108

Table 2.13 City of Hialeah Recycling: Government

Costs & Revenues in Calendar Year 1991

I. Curbside without Bottle Bill (as exists now)

II. As Projected via Curbside and Bottle Bill Combined

Diversion savings shown as two figures:

now; Dade Landfill disposal rate of $45/ton and after 10/92 when rate is estimated to rise to $54/ton.

I. Curbside

w/o BE

COSTS/REVENUES

Government Operating Costs (Collection & Processing)

Revenue from Sale of

Scrap Materials

Avoided Disposal Costs Net Operating Costs

TOTAL TONS DIVERTED:

$400,000

- 108,000

$292,000

now

II. Curbside and

BE rnmbi ned

$376,000

- 50,000 . $326,000

after noH after

-178.000 -213.000 -285.000 -342.000

$114,000 $79,000 $41,000 $0

3,948 6,332

GOV'T COST/TON DIVERTED: $29

after

$20 m

after

Table 2.14 City of Miami Recycling: Government Costs & Revenues in Calendar Year 1991

I. Curbside without Bottle Bill (as exists now)

II. As Projected via Curbside and Bottle Bill Combined

Diversion savings shown as two figures:

now: Dade Landfill disposal rate of $45/ton and

after 10/92 when rate Is estimated to rise to $54/ton.

I. Curbside

w/o BB COSTS/REVENUES

Government Operating Costs (Collection &

Processing)

Revenue from Sale of

Scrap Materials

Avoided Disposal Costs

Net Operating Costs

TOTAL TONS DIVERTED:

$526,000

- 72,000

$454,000

II. Curbside and BB Combined

$494,000

- 33,000

after

$461,000

noM after

-113.000 -136.000 -408.000 -489.000

$341,000 $318,000 $53,000 $0

2,516 9,064

GOV'T COST/TON DIVERTED: $136

after

$126 $€

after

n/at$0]

government to run a BCDL and that the landfill diversion costs

for a dual system are more due to the fact that more materials

are collected in a dual system. The first issue, no cost to

the municipality, was discussed in the analysis of the Rhode

Island Model and is the same for this study. The consumer

ends up paying for the system, but from a municipal government

viewpoint, if all enforcement and administrative costs are

handled by the federal government, then this can be a valid

assumption. The results of

looking at only the materials collected in the recycling

program before and after the passage of a BCDL are shown in

Table 2.15. As one can see there is no consistency. In the

case of Tallahassee, it costs more to run a curbside program

under the dual system, whereas the three other municipalities

would save money under a dual system when a landfill avoidance

cost is considered. If the municipal point of view is used

and the landfill avoidance costs are not considered the dual

system is always more expensive than the curbside only

solution. This is shown in Table 2.16. The assumption

that the landfill avoidance cost will be greater for a dual

system depends on the amount of materials collected in each

system. This assumption is valid today. Most recycling

programs capture below 4 0% of recyclables. If that 40% is

constant across all materials, in other words 40% of newspaper

and 40% of beverage containers, etc. are captured, then the

BCDL which has a return rate of approximately 85% (See Chapter

1) captures more materials than curbside/ drop-off.

Unfortunately very few studies actually break down the actual

amounts of each material that are generated and recycled, so

it is difficult to determine the actual percentage of each

material that is being recycled. If curbside recycling ever

reaches the point where it captures 85-90% of the beverage

container waste stream then this assumption will not hold

true. However as we saw in the Franklin Associates, LTD.

39

Table 2.15 Cost of Curbside Recycling vs. Curbside/Bottle

Bill When Only the Material Collected in the Curbside Program

are Consider

Town Tonnage in

Curbside after

BCDL enacted^*

Cost per Ton of only

Curbside

Cost per Ton

Curbside after

BCDL

Enacted'^

Tallahassee 3,703 $108 $149.09

Gainesville 2,138 $63 $48.54

Hialeah 2,820 $29 $14.54

Miami 2,039 $136 $25.99

Table 2.16 Cost of Curbside Program vs.Curbside/Bottle Bill

When Only the Materials Collected in the Curbside Program are

Considered and the Landfill Avoidance Cost is not Considered

Town Cost of Curbside

Only when Landfill Avoidance isn't

Considered

Cost of Curbside when a BCDL is

enacted and

Landfill Avoidance

isn't Considered

Tallahassee $125.74 $172.03

Gainesville $108.27 $135.00

Hialeah $73.96 $115.60

Miami $180.45

$226.09

^^These number were reported by the various cities and

have been adjusted to not include the estimated residue

material.

35r

'These numbers were calculated by taking the total cost

very expensive.

One criticism of this study is the way they calculated

the numbers for the curbside with BCDL program. They

took the number presented in the GBB generic analysis and

determined the percentage difference between the curbside-only

program and the dual program (for example, in the Tallahassee

scenario, the total costs were calculated by taking $774,777

the value for a single program in the generic analysis vs.

$728,290 for a dual program and saying that this is 94% of the

first value). The value for the second column of the generic

GBB analysis were actually based on the number of households

times the average collection costs, and the operating costs

times an estimated quantity of recyclables (which was

determined by estimating what would happen to each material

if a BCDL were enacted) , not a percent difference. The

numbers for the dual program in the Florida PIRG Education

Fund study may not be very accurate.

2.5 Review of "Bottle Bills and Municipal Recycling: A

Preliminary Cost Analysis" by the Tellus Institute

A study called "Bottle Bills and Municipal Recycling: A

Preliminary Cost Analysis" was preformed by Frank Ackerman and

Todd Schatzki of the Tellus Institute for the U.S.

Environmental Protection Agency. This study was revised on

May 2, 1990. It compares the social costs and the municipal

costs of four systems of solid waste management which are

presented below.

2.5.1 Structure and Assumptions

This study looked at a generic community of 500,000

They used four scenarios based on the Tellus Institute Waste

Plan model. The four scenarios are listed below:^*

1) No recycling of any kind is conducted. All waste goes

to the landfill.

2) A BCDL, which diverts 85% of beer and soft drink

containers from the landfill, is in place. All other

waste goes to the landfill.

3) A curbside recycling program is in place which recycles

newspaper, glass, aluminum, and plastic containers.

These materials are then sent to a Municipal Recovery

Facility (MRF). The diversion rate of the curbside

program is 42-56%.

4) When both the BCDL and the curbside program are in

place. The BCDL diverts 85% of beer and soft drink

containers. The curbside recycling program divert 85%

of the remaining waste. The rest of the waste is

diverted to the landfill.

The Tellus model then compared the total social costs of

the four scenarios and the total municipal costs of the four

scenarios. They did this by graphing the total solid waste

system costs against landfill tipping fees. They felt that

"the higher the tipping fee, the more attractive any given

recycling option becomes^^". The social costs included the

BCDL cost per ton based on the value of $278 per ton for New

York in the Franklin Associates, LTD. model. The municipal

^^Frank Ackerman and Todd Schatzki. Bottle Bills and

Municipal Recycling; A Preliminary Cost Analysis (Boston:

costs do not use this figure and represent the cost to the

solid waste authority. These costs were graphed against

tipping fees which represented landfill avoidance costs.

2.5.2 Findings of the Tellus Institute

The Tellus Institute found that as tipping fees increase

recycling options became more cost-effective. The slopes of

these graphs represent the change in solid waste system cost per dollar of tipping fee, in other words the tonnage landfilled (Tellus, 1990). Figure 2.1 shows the results of the social cost versus the landfill tipping fees. The two

scenarios containing BCDL are higher in costs. At $0 tipping

fee, recycling options are more expensive than no recycling. This changes at $24 for a curbside program and at $48 for a

dual program. On the social graph, if the graph were

continued, the BCDL would become most attractive at $260. Theformula they used to calculate this is

Net BCDL system cost = avoided garbage collection costs +

avoided tipping fees.^

This formula was rearranged to determine:

Tipping fee required = bottle bill system cost

-for bottle bill break-even avoided garbage costs.

This cost of $260 was calculated using the value of $278

from the Franklin study. The value $18 was used for avoided

collection costs. This value may seem small but collection

costs are based mostly on the number of stops and they do not

decrease significantly due to a reduction in volume.

Figure 2.1 Social Cost Comparisons With and Without a Bottle

Bill

Total Cost (Millions)

0 10 20 30 40 50 60 70 80 90 100

Tip Fee ($/Ton)

--- W/ BCDL. No Curbslde-4- W/ BCDL, W/ Curbside

-*- No BCDL, W/ Curbslde-s- Nothing

ͣ

44

The municipal cost graph is shown in figure 2.2. If we

look at the Municipal Graph, a BCDL with no curbside is most

cost effective at tipping fees of less than approximately $42.

From approximately $42-$52 the three scenarios (a dual system,

a BCDL only, and curbside only) are indistinguishable, but

clearly better than no BCDL and no curbside. At greater than

a $52 tipping fee, a dual system is most cost-effective. The

final conclusion of this report is that "under our

assumptions, a bottle bill is not cost-effective if viewed as

purely a solid waste management option for a large community

(Tellus 1990)." However they go on to state that other

issues associated with cost-effectiveness such as the cost of

litter prevention have to be considered. For New York the

increased cost of the BCDL could be broken down into a litter

prevention cost of $6.00 a person.^' They also suggest that

further study is needed to determine if more or less material

is diverted from landfilling and incineration due to the

effects of a BCDL on curbside recycling.

2.5.3 Analysis of the Tellus Institute

The most disputed part of this report is the use of the

value $278 per ton as the net cost of the beverage container

deposit system. This was the value used by the Franklin

Associates, LTD. for the system in New York. When the Tellus

Institute uses the value shown in the Franklin Associates,

LTD.Report for Vermont ($168 per ton) the tipping fee is

reduced to $150. Although this is high it represents a

reduction in cost of about 40% overall.

These values as determined by the Franklin Associates,

LTD. were based on the costs to the wholesalers and

Figure 2.2 Municipal Cost Comparisons With and Without a

Bottle Bill