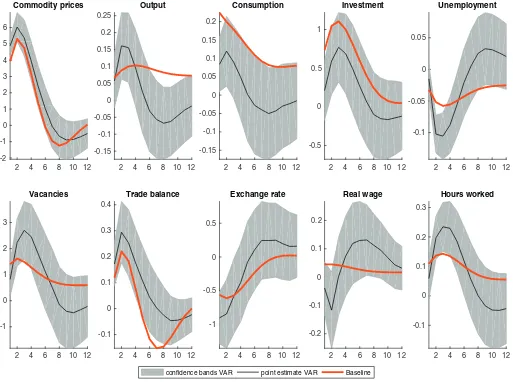

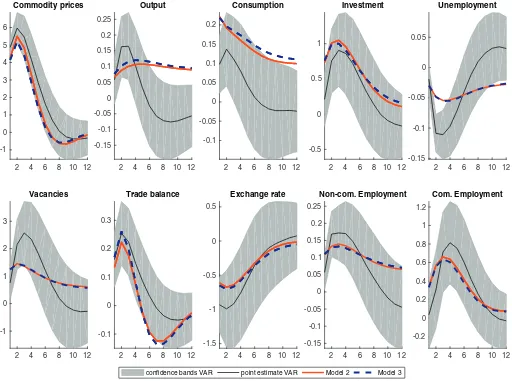

Commodity prices and labour market dynamics in small open economies

Full text

Figure

Related documents

This findings were almost similar with previous study that was conducted among 480 incident cases of ovarian cancer in Norway with five-year survival probability of 39% and

Sustainability Champion had direct influence upon the curriculum within her department, which is evident in the answers provided, however at College A, the Sustainability Champion

To comply in the most appropriate manner with the demands of the stadium security standards (which require automatic control systems at entrances and a total ban on supporters

(5 Week Class - Starts 1/4/2016, Ends 2/7/2016) 037 CHICANO LITERATURE (UC:CSU) 3.00 UNITS Prerequisite: None.. An analysis of the literary, social, and historical aspects of

Th is course prepares candidates for certifi cation as an Emergency Medical Technician according to the regulations set forth by the State of New Jersey in accordance with the

Foam board photograph of Robert H. Goddard with rocket in background and people on either side. Foam board photograph of Robert H. Goddard as a boy with his parents.

The aim of the study was to examine the relationship between child rearing practices and adolescents’ attitudes towards sexual debut and to see which among

Meaning that Tourism sector (number of tourism arrival (NTA), Expend on tourism sector (ETS), agriculture (AGR), Transport on tourism sector (TPT), Exchange rate (EXR),