ABSTRACT

BECKER, TIMOTHY CARL. Improving the Predictability of Construction Project Outcomes through Project Level Indirect Construction Cost Practices. (Under the direction of Dr. Edward J. Jaselskis).

manager-representing five hard project performance metrics. In summary, this research operationally defines IDCC, tests the association between IDCC practices and construction project outcomes, and offers process improvement opportunity by recommending leading IDCC practices. The predictability of construction project outcomes can be improved through application of the full collection of IDCC practices outlined and detailed in this research. Financial and time resources are constrained on construction projects, so practitioners may elect to focus their efforts on those specific IDCC practices most closely related to the construction project outcome(s) considered of highest value to the owner.

Improving the Predictability of Construction Project Outcomes through Project Level Indirect Construction Cost Practices

by

Timothy Carl Becker

A dissertation submitted to the Graduate Faculty of North Carolina State University

in partial fulfillment of the requirements for the Degree of

Doctor of Philosophy

Civil Engineering

Raleigh, North Carolina

2012

APPROVED BY:

________________________________ ________________________________ Edward J. Jaselskis, Ph.D., P.E. Min Liu, Ph.D.

Committee Chair

DEDICATION

BIOGRAPHY

ACKNOWLEDGEMENTS

Many individuals contributed to this work and I wish to properly acknowledge them. First, Dr. Edward J. Jaselskis provided training, inspiration, and support as my major professor—I am for grateful that many years after being in his undergraduate class I was reunited for this pursuit of a Ph.D.

This dissertation research was conducted with the financial support of the Construction Industry Institute (CII). CII is a highly reputable organization comprised of leading owner and construction companies with the purpose of improving the delivery of capital improvement projects. I wish to acknowledge Co-Principal Investigator Dr. Mohamed El-Gafy and the members of CII Research Team 282. These friends, along with more than 100 other industry professionals, offered their personal insights and company data which underlie the findings of this research.

I wish to acknowledge special academic and professional mentors who have supported me and contributed to this educational journey, namely: Bob Stephenson, Mark Federle, Charles Jahren, Jennifer Shane, Kelly Strong, Kent Moe, Doug Powell, and Mike Espeset.

TABLE OF CONTENTS

LIST OF TABLES ... ix

LIST OF FIGURES ... xii

CHAPTER 1: INTRODUCTION ...1

1.1 Problem Statement ...3

1.2 Essential Research Question ...3

1.3 Research Objective ...4

1.4 Definition of Professional Service Areas ...5

1.5 Dissertation Overview ...6

CHAPTER 2: LITERATURE REVIEW ...7

2.1 Indirect Costs ...7

2.1.1 Causal Relationship ...9

2.1.2 Physical Incorporation ...11

2.1.3 Definition of the Cost Object ...11

2.2 Indirect Construction Costs...13

CHAPTER 3: METHODOLOGY ...18

3.1 CII Approach to Research ...18

3.2 Overview of Research Methodology ...19

3.2.1 Outline of Research Methodology ...19

3.2.2 Data Collection Instruments ...22

3.3 Phase 1: Research Planning and Scope Refinement ...24

3.3.1 Master Research Question #1 ...24

3.3.2 Aggregation and Analysis of IDCC Items ...25

3.3.3 Structured Research Charrettes ...26

3.3.4 IDCC Importance Ranking Survey ...27

3.4 Phase 2: Data Collection & Documentation ...28

3.4.1 Master Research Question #2 ...29

3.4.3 Data Collection Survey for Key IDCC ...30

3.4.4 Data Collection Interviews ...31

3.4.5 Data Aggregation and Documentation ...36

3.5 Phase 3: Verification and Validation Process ...41

3.5.1 Master Research Question #3 ...41

3.5.2 Subject Matter Expert Verification ...44

3.5.3 Validation Case Studies ...45

3.5.4 Statistical Analysis of IDCC-Practices Project-Level Survey ...46

3.6 Statistical Software Applications ...74

CHAPTER 4: IDCC OPERATIONAL FRAMEWORK ...76

4.1 Operational Definition ...76

4.1.1 Lexical Definition ...77

4.1.2 Aggregate Chart of Accounts...84

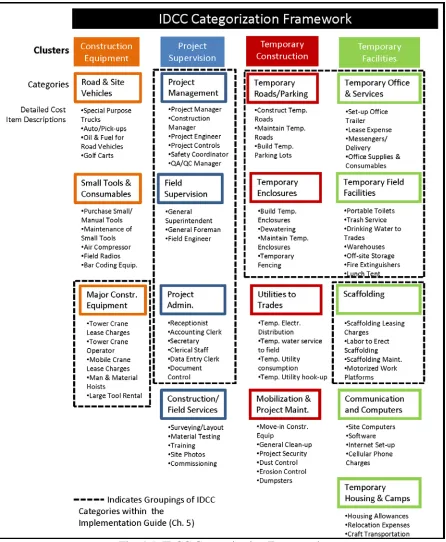

4.1.3 Categorization Framework ...85

4.2 Preliminary Rankings of IDCC Categories...87

4.3 IDCC Prioritization ...89

4.3.1 Most Important IDCC Categories ...90

4.3.2 Most Challenging IDCC Categories ...94

4.3.3 Most Wasteful IDCC Categories ...95

4.4 Company Approaches to IDCC ...96

CHAPTER 5: IMPLEMENTATION GUIDELINES ...99

5.1 Overview of Leading IDCC Practices ...100

5.2 Major Construction Equipment...101

5.2.1 Overview ...101

5.2.2 MCEQ Considerations Checklists ...102

5.2.3 MCEQ Process Flowcharts ...112

5.2.4 MCEQ Representative Tools ...116

5.3 Construction Management and Supervisory Personnel ...125

5.3.2 CM&SP Considerations Checklists ...127

5.3.3 CM&SP Process Flowcharts ...133

5.3.4 CM&SP Representative Tools ...136

5.4 Scaffolding ...141

5.4.1 Overview ...141

5.4.2 Scaffolding Considerations Checklists ...141

5.4.3 Scaffolding Process Flowcharts ...148

5.4.4 Scaffolding Representative Tools ...151

5.5 Temporary Provisions ...158

5.5.1 Overview ...158

5.5.2 TP Considerations Checklist ...158

5.5.3 TP Process Flowcharts ...166

5.3.4 TP Representative Tools ...169

5.6 Innovative Practices for Estimating, Controlling & Managing IDCC ...171

5.6.1 Overview ...171

5.6.2 Real-time, Online Equipment Tracking ...171

5.6.3 Advanced Small Tools Inventory Systems ...173

5.6.4 Delivery of Trade Worker Amenity Services to Work Locations ...174

5.6.5 Advanced Laydown Yard Management Systems ...174

CHAPTER 6: VERIFICATION & VALIDATION ...177

6.1 Validation Case Studies ...177

6.2 Statistical Analysis of IDCC-Practices Project-Level Surveys ...179

6.2.1 Descriptive Statistics of Dataset ...180

6.2.2 Data Reliability Testing ...184

6.2.3 Hypothesis Testing and Correlation Analysis ...185

6.2.4 Investigation of IDCC Histogram Practice Data ...192

CHAPTER 7: SUMMARY AND CONCLUSIONS ...201

7.1 Research Summary ...201

7.3 Intellectual Merit ...202

7.4 Limitations ...204

7.5 Recommendations for Future Research ...206

7.6 Conclusions ...210

REFERENCES ...211

APPENDICES ...218

APPENDIX A―CII RT-282 GLOSSARY ...219

APPENDIX B―AGGREGATED CHART OF IDCC ACCOUNTS ...221

APPENDIX C―RESEARCH CHARRETTE TEMPLATE (FEB. 2011) ...228

APPENDIX D―SUMMARY OF REPORTED IDCC PROBLEMS ...230

APPENDIX E―IDCC IMPORTANCE RANKING SURVEY ...235

APPENDIX F―RESEARCH CHARRETTE EXAMPLE (APRIL 2011) ...236

APPENDIX G―DATA COLLECTION INSTRUMENT (JULY 2011) ...239

APPENDIX H―DATA COLLECTION INTERVIEW GUIDE (SEPT. 2011) ...258

APPENDIX I―TOOL EVALUATION SURVEY INSTRUMENT ...273

APPENDIX J1―CII BM&M IDCC PROJECT LEVEL ON-LINE SURVEY ...285

APPENDIX J2―IDCC PRACTICE PROJECT LEVEL SURVEY ...290

APPENDIX K―LIST OF TEMPORARY PROVISION ITEMS ...295

LIST OF TABLES

Table 2.1: Summary of Definitions of Indirect Costs from Literature ...8

Table 2.2: Definitions of Commonly Used Terminology Similar to or Substituted for IDCC ...14

Table 2.3: Categorization of Project Costs by Indirect Construction vs. Indirect Non-Construction Costs. ... 16

Table 3.1: Companies Represented by Subject Matter Experts on RT-282 ... 18

Table 3.2: Summary of Data Collection Instruments... 23

Table 3.3: Summary Relevant Research with Example Statistical Approaches ... 51

Table 3.4: Listing of Representative IDCC Practices (independent variables) ... 54

Table 3.5: Listing of Project Outcomes (dependent variables) ... 55

Table 3.6: Summary of Statistical Tests and Data Types ... 56

Table 3.7: Decision Rules and Group Counts for Lower and Higher IDCC Practices .... 58

Table 3.8: Decision Rules and Counts for High and Low Project Outcome Groups... 60

Table 3.9: Critical Levels of Z Statistic for Selected Levels of Significance ... 67

Table 3.10: Summary of Software Utilized in this Research ... 75

Table 4.1: Categorization of Project Costs by Indirect vs. Direct Construction Costs .... 84

Table 4.2: Count Data for Most Important IDCC Categories ... 90

Table 4.3: Ranked Order of Importance by Expert Area of Expertise... 91

Table 4.4: Wilcoxon Signed-Rank Test p Values ... 94

Table 4.5: Count Data for Most Challenging IDCC Categories ... 94

Table 5.1: Count Summary of IDCC Practices Included in Chapter 5 ... 100

Table 5.2: Considerations Checklist for Estimating Major Construction Equipment (MCEQ) Costs ... 102

Table 5.3: Considerations Checklist for Controlling Major Construction Equipment (MCEQ) Costs ... 107

Table 5.5: List of Common Titles of Field Supervision Staff... 126

Table 5.6: List of Common Titles of Project Management Staff ... 126

Table 5.7: Considerations Checklist for Estimating CM&SP Costs ... 127

Table 5.8: Considerations Checklist for Controlling CM&SP Costs ... 130

Table 5.9: Considerations Checklist for Managing CM&SP Costs ... 131

Table 5.10: Considerations Checklist for Estimating Scaffolding Costs ... 141

Table 5.11: Considerations Checklist for Controlling Scaffolding Costs ... 144

Table 5.12: Considerations Checklist for Managing Scaffolding Costs ... 145

Table 5.13: List of Common Items Included as Temporary Provisions. ... 158

Table 5.14: Considerations Checklist for Estimating Temporary Provisions Costs ... 159

Table 5.15: Considerations Checklist for Controlling Temporary Provisions Costs ... 162

Table 5.16: Considerations Checklist for Managing Temporary Provisions Costs ... 164

Table 6.1: Summary of Results from the Validation Case Studies ... 178

Table 6.2: Descriptive Statistics for IDCC Practices ... 180

Table 6.3: Descriptive Statistics for Construction Project Outcomes ... 181

Table 6.4: Most Often Used of the IDCC Practices ... 182

Table 6.5: Least Often Used of the IDCC Practices ... 182

Table 6.6: Most Not-Applicable of the Representative IDCC Practices ... 183

Table 6.7: Greatest Variation in Use of the Representative IDCC Practices ... 183

Table 6.8: Data Reliability Statistics ... 184

Table 6.9: Mann-Whitney U Test Results for the 15 Representative IDCC Practices vs. 5 Project Outcome Metrics ... 188

Table 6.10: Spearman Correlation Results for the 15 Representative IDCC Practices vs.5 Project Outcome Metrics ... 188

Table 6.11: Chi-square Test Results for the 15 Representative IDCC Practices vs. Five Project Outcome Metrics ... 189

Table 6.13: Statistical Test Results for 15 Representative IDCC Practices vs.

Averaged Project Outcome ...190

Table 6.14: Summary of Statistical Findings (alpha levels of 0.05, 0.01 and 0.005) ...191

Table 6.15: Data Table of IDCC Histograms by Project Size by Cost Category ...193

Table 6.16: Data Table of IDCC Histograms by Project Size by Duration Category ...194

Table 6.17: Data Table of IDCC Histograms by Project Type ...195

Table 6.18: Data Table of IDCC Histograms by Project Nature ...196

Table 6.19: Chi-square Test Results for Project Characteristics vs. Schedule Outcomes ...198

Table 6.20: Chi-square Test Results for IDCC Histogram excluding Non-Use Respondents ...199

Table 6.21: Phi Correlation Test Results for IDCC Histogram excluding Non-Use Respondents ...199

Table 6.22: Mann-Whitney Test Results for IDCC Histogram excluding Non-Use Respondents ...199

Table 6.23: Spearman Rank Test for IDCC Histogram excluding Non-Use Respondents ...200

LIST OF FIGURES

Fig. 3.1: Flowchart of Research Methodology by Phase & Task ... 22

Fig. 3.2: Categorization of Project Type Experience of Subject Area Experts ... 33

Fig. 3.3: Distribution of Data Collection Interview Participants by Company ... 33

Fig. 3.4: Symbolism Used in Flowchart Mapping of Processes ... 39

Fig. 3.5: Generic Flowchart for Estimating, Controlling & Managing IDCC ... 40

Fig. 3.6: Distribution of Construction Costs of Sample Projects ...49

Fig. 3.7: Distribution of Construction Durations of Subject Projects ... 49

Fig. 3.8: Distribution of Project Type of Subject Projects ... 49

Fig. 3.9: Distribution of Project Nature of Subject Projects ... 50

Fig. 3.10: Data Analysis Work Plan Flowchart... 56

Fig. 3.11: Contingency Table for 2-Group Median Test ... 63

Fig. 4.1: 2-Dimensional Matrix Model for Categorization of Project Construction Costs ... 79

Fig. 4.2: Definition Model of Construction Costs as Subset of Total Project Costs ... 80

Fig. 4.3: Model of Chronological Factor of Defining Indirect Construction Costs ... 81

Fig. 4.4: Model of Location Factor of Defining Indirect Construction Costs ... 83

Fig. 4.5: IDCC Categorization Framework ... 86

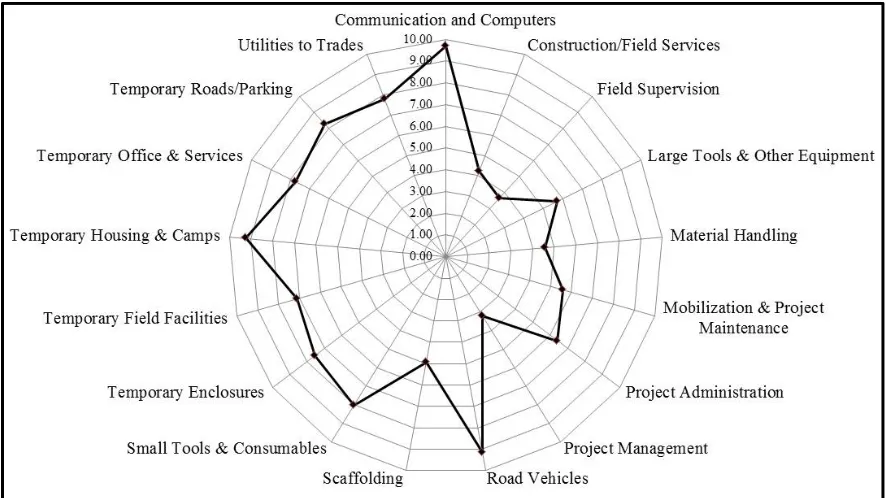

Fig. 4.6: Radar Plot of Importance of Preliminary IDCC Groupings ... 87

Fig. 4.7: Radar Plot of Importance of Preliminary IDCC Groupings Separately Ranked by Owners and Contractors ... 88

Fig. 4.8: Histogram Relating Better IDCC Practices with Project Performance ... 89

Fig. 4.9: Histogram of IDCC Categories by Relative Importance ... 91

Fig. 4.10: Most Important IDCC Category Histogram by Estimating ... 92

Fig. 4.11: Most Important IDCC Category Histogram by Controlling ... 93

Fig. 4.12: Most Important IDCC Category Histogram by Managing ... 93

Fig. 4.13: Histogram of IDCC Categories by Most Challenging ... 95

Fig. 4.15: Histogram of Perception of Company’s Approach to IDCC ... 97

Fig. 4.16: Histogram of Perception of Wasteful Spending due to Current IDCC Practices ... 97

Fig. 5.1: Process Flowchart of MCEQ Cost Estimating Process ... 113

Fig. 5.2: Process Flowchart of MCEQ Cost Controlling Process ... 114

Fig. 5.3: Process Flowchart of MCEQ Cost Managing Process ... 115

Fig. 5.4: List of Heavy Lifts ... 116

Fig. 5.5: MCEQ Planning Worksheet ... 117

Fig. 5.6: MCEQ Maintenance Tracking Log ... 119

Fig. 5.7: Operator Logs for Shared MCEQ ... 120

Fig. 5.8: MCEQ Utilization Tracking Log ... 121

Fig. 5.9: Equipment Rental Rate Tracking Chart ... 122

Fig. 5.10: MCEQ Control & Forecasting Cumulative Cost Histogram ... 123

Fig. 5.11: Shared MCEQ Use Request Form ... 124

Fig. 5.12: Process Flowchart for Estimating CM&SP Costs ... 133

Fig. 5.13: Process Flowchart for Controlling CM&SP Costs ... 134

Fig. 5.14: Process Flowchart for Managing CM&SP Costs ... 135

Fig. 5.15: CM&SP Staff Plan ... 137

Fig. 5.16: Force Report/Project Staff Head-count Tracking Log ... 138

Fig. 5.17: CM&SP Control & Forecasting Cumulative Cost Histogram ... 139

Fig. 5.18: Representative Report Card by Client ... 140

Fig. 5.19: Process Flowchart for Estimating Scaffolding Costs ... 148

Fig. 5.20: Process Flowchart for Controlling Scaffolding Costs ... 149

Fig. 5.21: Process Flowchart for Managing Scaffolding Costs ... 150

Fig. 5.22: Scaffolding Estimating Worksheet ... 152

Fig. 5.23: Scaffolding Utilization Report ... 153

Fig. 5.24: Scaffolding Control & Forecasting Cost Histogram ... 154

Fig. 5.25: Scaffolding Identification Tags ... 155

Fig. 5.27: Scaffolding Dismantlement/Return Form ... 157

Fig. 5.28: Process Flowchart for Estimating Temporary Provisions Costs ... 166

Fig. 5.29: Process Flowchart for Controlling Temporary Provisions Costs ... 167

Fig. 5.30: Process Flowchart for Managing Temporary Provisions Costs ... 168

Fig. 5.31: Sample of Temporary Provisions List of Items ... 169

Fig. 5.32: TP Control & Forecasting Cost Histogram ... 170

Fig. 5.33: Model of Online Equipment Tracking Process ... 172

Fig. 5.34: Photograph of a Small Tools Vending Machine ... 173

Fig. 5.35: Traditional one-dimensional bar code and two-dimensional bar code ... 175

Fig. 5.36: Photograph of an RFID-tagged Pipe Spool ... 176

Fig. 5.37: Example of GPS Location of Material... 176

Fig. 6.1: Cronbach’s Alpha Scores for the Independent and Dependent Variables .... 184

Fig. 6.2: Cronbach’s Alpha Scores for Project Outcome Variables ... 185

Fig. 6.3: Histogram of Responses Regarding Use of Histograms to Control IDCC ... 193

Fig. 6.4: Stem and Leaf Plot of Project Cost Category by Level of Use of IDCC Histograms ... 194

Fig. 6.5: Stem and Leaf Plot of Project Duration Category by Use of IDCC Histograms ... 195

Fig. 6.6: Stem and Leaf Plot of Project Type Category by Use of IDCC Histograms 196 Fig. 6.7: Stem and Leaf Plot of Project Nature Category by Use of IDCC Histograms ... 197

CHAPTER 1: INTRODUCTION

In today’s highly competitive business environment, construction companies can no longer sustain, and with an even lesser probability grow, current businesses by continuing the status quo approach to the management of construction project operations. Many market indicators point to a likely future of increased global competition, greater penetration of foreign construction firms in U.S. markets and intensifying client demands for reduced project cost and an enhanced service proposition (Friedman, 2007; FMI, 2009). Leading construction firms will evolve their people, processes and organizations to modern views of productivity and collaboration. To this end, construction companies must remove non-value adding effort (“waste”) from their processes. Elimination of waste results in lower costs, quicker schedules, smarter construction methods and more satisfied clients.

Since all projects incur IDCC, all owners and contractors face responsibilities, obligations, and opportunities with respect to IDCC. Contractual provisions, corporate cultures, standard operating procedures and many other business- and project-specific factors determine the categorization of discrete project costs as either direct or indirect costs. Differences of understanding, perspective, and opinion can lead to misunderstanding, lack of communication, and, at times, mistrust. For these reasons and other, owner and construction companies have reported through the Construction Industry Institute (CII) that estimation, control and management of indirect construction costs (IDCC) is an opportunity for process improvement and waste elimination. Some construction industry experts have described their handling of IDCC as more reactive than proactive. Other experts consider IDCC non-consequential thereby little effort is afforded to proper planning, control and execution of indirect construction scope.

on construction projects resulting from the lack of attention given to IDCC. This research suggests that the identification and sharing of effective IDCC-related practices to be performed at the project level, including consideration checklists, process mapping and practical tools, may improve the predictability of certain key project outcome measures and the ultimately has the potential to improve the construction industry as a whole.

One view of reducing the total cost of construction projects is to minimize spending on IDCC (these costs are also referred to general conditions, general requirements, project overhead expenses and other terms). For example, clients may insist on reduction of craft supervisory staff or elimination of certain temporary office services each in an approach to drive down the total cost of the project. This dissertation suggests that across the board reduction in IDCC practices is unwise. Rather proper levels of effort afforded to key IDCC practices are positively correlated to improved project performance metrics. For example, this research has shown a strong statistically significant relationship between the frequency of meetings of project managers and field supervisors to specifically discuss IDCC and the quality performance outcomes of construction projects.

Multiple project-level case studies support that the application of IDCC practices leads to better project performance. If the perception of these experts and the findings of the case studies are correct, the construction industry should leverage leading practices for estimating, controlling and managing IDCC to improve project performance. Doing so will contribute to the overall productivity of the construction industry and aid in its long-term durability and future financial resiliency.

It is proposed that by doing so, the predictability of construction project outcomes can be improved at the project level.

1.1 Problem Statement

Literature reports the percentage of indirect cost of total cost ranges from less than 10% to as much as 40% or more. Therefore, the construction industry should and can do a better job of estimating, controlling and managing IDCC. By doing so, individual project performance will be improved as measured though key project specific metrics. Further, in a larger context, increased productivity through IDCC practices can contribute to some extent to the overall durability of the construction industry.

Two hurdles stand in lane to achieving improved estimation, control and management of IDCC. The first hurdle is building the prerequisite motivation within construction project teams to increase focus and resources to IDCC—in short, answering why should project teams care about IDCC. To this point, this research provides empirical data validating the positive relationship between the use of certain leading IDCC practices and improved project performance outcome metrics.

The second hurdle is providing project teams with knowledge necessary to execute improved estimating, control and management of IDCC. This research has identified and documented industry expert-recommended, leading practices (e.g., checklists, process flowcharts, and tools) for four groups of IDCC deemed the most important to project outcomes by subject matter experts. By doing so, this research offers a framework for industry to allocate and resource levels of effort in estimating, controlling and managing with project outcome measure.

1.2 Essential Research Question

“What best or innovative practices are now available or utilized for managing construction indirect costs (and the associated component elements) such that risks, schedules, and costs are properly optimized for both contractor and owner”?

In developing the research plan to address the above essential question, the writer proposed three master research questions (MRQ) to add definition for the research.

1. What are IDCC, how can they be categorized, and what is the prioritization of IDCC?

2. What are the leading industry practices for estimating, controlling and managing IDCC?

3. Is there a relationship (and if so in what direction) between the level of effort given to estimating, controlling and managing IDCC (i.e., IDCC practices) and key metrics of project outcome?

Within the structure of these three master research questions are numerous related questions and proposed hypothesis addressed in this research. These questions are detailed in Chapter 3 with results presented in Chapters 4 and 5.

1.3 Research Objective

The research objective of this project is to answer the essential research question by investigating, documenting, and validating leading industry practices for estimating, controlling and managing indirect construction costs. Answering this question offers mutual and shared benefit to owners and contractors engaged in capital improvement projects. Further investigation into new or innovative practices may encourage strategic application of these approaches to IDCC. By accomplishing this primary research objective, the research will contribute to the improvement of the construction industry as a whole.

2. Investigate and outline leading IDCC practices for improving construction project outcomes

3. Validate use of IDCC practices at the project level and assess relationships between IDCC practices and construction project outcomes.

A full methodology with detailed, step-by-step explanation is provided in Chapter 3.

1.4 Definition of Professional Service Areas

Reporting by the industry members of the research team identified three specific areas of professional expertise and/or departmental services typical to the construction industry regarding IDCC practices. These three professional service areas are estimating, controlling and managing. The research team conceived a research work break-down structure categorizing specific IDCC practices and tools used by industry into each of these three professional areas.

Some confusion became evident within the research team as to the definition of these areas. Follows are guidelines for readers of this dissertation to understand what is meant by estimating, controlling and managing within the context of this research. It is acknowledged that differing definitions can be found in literature and throughout industry practice.

Estimating—establishing a plan for the project (the “plan” is often comprised

of many sub-plans and addresses cost/budget, schedule, safety and other project outcome metrics)

Controlling—measuring, tracking and reporting the progress of the project,

comparing progress to plan, and forecasting/predicting project outcomes on a periodic basis

Managing—taking actions to influence the performance outcome metrics of the

project

1.5 Dissertation Overview

This dissertation provides a tool for the construction industry to focus on IDCC and related estimating, control and management practices. This introduction to the topic is followed by review of published literature in Chapter 2. Explanation is given of work by prior researchers both in the more general topic of indirect cost and on literature addressing indirect costs specifically for construction projects. Chapter 3 outlines a 3-phase research methodology conducted in execution of this research, including statement of numerous research questions and proposed hypotheses. Specific steps are described and data collection instruments are listed that have been taken to collect and analyze data supporting the findings and conclusions of this research.

CHAPTER 2: LITERATURE REVIEW

This research project commenced with a review of published literature regarding indirect costs and thorough targeting of the more narrowly defined subject of indirect construction costs (IDCC). It became evident after much literature searching that little specific research has been conducted regarding IDCC. Literature review was also performed to identify published industry practices specifically regarding estimating, controlling and managing of the key IDCC categories of interest, namely major construction equipment, project staff, scaffolding and temporary provisions. Again, scarce literature has been published by academia in this narrowly defined area.

Literature review revealed that a significant body of academic work has been conducted in the field of accounting to define direct and indirect costs, including elaboration in many university textbooks. Chapter 2 provides some background information on defining indirect costs, including three concepts used to organize accounting costs into direct or indirect categories. This explanation is followed by the presentation of an operational definition for indirect construction costs, including foundational information and a categorization framework. The IDCC categorization framework served as an important scope definition tool throughout the course of this research. It quickly provides parameters for what costs are termed IDCC for this research. The author proposes that this framework similarly can serve as a helpful communication aid for construction industry professionals.

2.1 Indirect Costs

Table 2.1: Summary of Definitions of Indirect Costs from Literature

Definitions of Indirect Costs Source of

Definition

Indirect costs are “costs that are not normally recognized as a direct cost of ‘work in place’.” (p. 49)

Holland and Hobson (1999)

1. Indirect costs are “cost that cannot be attributed to any specific work item…” (p. 92).

2. “Indirect costs are such items as contractors’ overheads, profit, contingencies, escalation, and interest during construction.” (p. 10)

Ahuja and Campbell (1988)

“Costs that can be specifically identified to the completion of a specific construction project, but cannot be identified with the completion of a specific construction component on that project.”

Peterson (2005)

“Indirect costs are costs that cannot be attributed readily to a part of the final product (e.g., temporary facilities).”

Construction Owners Association of Alberta (COAA) “1) Costs not directly attributable to the completion of an activity. Indirect

costs are typically allocated or spread across all activities on a predetermined basis. 2) In construction, all costs which do not become a final part of the final installation, but are required for the orderly completion of the installation and may include, but are not limited to, field administration, direct supervision, capital tools, startup costs, contractor’s fees, insurance, taxes, etc.”

Association for the Advancement of Cost Engineering International (AACE)

Costs that are not directly assignable/traceable to a product or process. Brimson (1991)

Costs that “cannot be associated with any particular work package or activity (typically vary with time).”

Gray and Larson (2008)

Any cost that cannot be directly identified with a single final cost object but can be identified with two or more final cost objective or an intermediate cost objective.

Cost Accounting Standards, CAS 418.30(3) Indirect costs are any costs “not directly identified with a single, final cost

objective, but rather identified with two or more final cost objectives or an intermediate cost objective.

U.S. Federal Acquisitions Regulations For the construction industry, indirect costs are “basically everything except

craft labor, material, equipment, and subcontracts.” (p. 2)

Northfleet (2007)

“Indirect costs, also known as construction overhead, relate to expenses that cannot be easily identified with a specific contract. Indirect costs may include rent for the shop/yard, shop labor, repairs and maintenance, and equipment insurance.”

Blattner (2008)

“Indirect costs are costs that cannot be easily and accurately traced to a cost object.” (p. 32)

Mowen and Hansen (2006)

“An indirect cost is a cost which can be identified with jobs but not with a specific job or unit of production.” (p. 243)

Palmer et al. (1999)

“Indirect costs consist of site overheads, general overheads, profits and allowance for risks.” (p. 31)

Tah et al. (1994)

“Indirect costs are those not directly assignable/traceable to a product or process.”

Table 2.1 continued

“Indirect costs….include the costs of indirect labor, contract supervision, tools and equipment, supplies, quality control and inspection, insurance, repairs and maintenance, depreciation and amortization, and, in some circumstances, support costs, such as central preparation and processing of payrolls.” (p. 18892)

AICPA (1981)

“Indirect costs. The costs that cannot be attributed to a single task of construction work are classified as indirect costs. These costs include overhead, profit, and bond.”

Knutson et al. (2004)

“There are also indirect costs that occur in the field. These costs, called general conditions or field office overhead, are necessary to supervise and support the job site.”

Gould (2002)

“Indirect cost. Cost that is not easily traced to a cost object; no clear cause-and-effect relationship exists between the cost object and the cost, or the cost of tracing the cost to the object exceeds the benefit.” (p. 680)

Eldenburg and Wolcott (2005)

The difference in definition of direct and indirect costs provided in the above sources can be explained by three conditions applicable to any particular discrete cost, as follows: 1) identification of causal relationship of a particular cost item to a cost object, 2) evaluation of whether a particular cost item becomes physically incorporated as part of final product delivered to the customer, and 3) the perspective of the accountant or other individual making the categorical determination. These three cost conditions are explained further in the following sections.

2.1.1 Causal Relationship

The terms “cost object” and “cost objective” are commonly used in accounting literature to describe the product, service or other resulting manifestation of the contribution of numerous costs. Direct costs can be identified, tracked or linked solely to one particular cost object. In the construction context, a cost object could be defined as a discrete, measurable component of the construction work. For example, a specific quantity of concrete masonry unit (CMU) material (a discrete “cost item”) which will be incorporated into a defined section of masonry wall partition (the “cost object”) is a direct construction cost and is easily and directly associated with the cost object. This CMU material has been specified and purchased for this particular wall location and is installed accordingly. The cost of this CMU material is independently accounted for and can be directly linked to the cumulative cost of this uniquely identifiable section of masonry wall partition. The cost of CMU material (a discrete cost item) is a direct cost and a component of the total cost of the masonry wall partition (a cost object).

2.1.2 Physical Incorporation

Another concept of differentiation between direct and indirect costs relates to whether the cause of the cost ultimately becomes physically incorporated into a final product delivered to the client. This partitioning approach of direct and indirect costs is common in manufacturing-related cost accounting methodologies. As a general categorization rule, if the source of the cost does not ultimately become a physical element of the final product sold to the consumer, then this cost item is considered an indirect cost. Only the costs of the set of accumulated physical elements incorporated into the product delivered to or purchased by the client are considered direct costs. By this definition, all labor and equipment is indirect and only a portion of material costs actually becomes direct cost; waste materials are considered indirect cost.

This strict definition of direct cost provides some contribution to a construction-industry definition for indirect costs, but is too limiting to correlate directly from a manufacturing to construction context. Yet, an adaptation of this logic is offered by Ahuja and Campbell in their definition of direct costs. “Direct costs include labor, materials, equipment, and supplies, all of which are incorporated into some distinct feature of the completed work” (1988, p. 10). Although labor, equipment and supplies are not physically incorporated into the final product, these authors acknowledge that labor, equipment and supplies necessary for transformation of materials into the final product can be considered direct cost of the identifiable and discrete cost object. Holland and Hobson also assessed, through a survey of contractors, that contractors categorize certain cost items as direct cost even if the cost is associated with equipment, supervision or other activity that is not ultimately a physical component of the constructed improvements (1999).

2.1.3 Definition of the Cost Object

thousands of material invoices, subcontractor monthly payment applications, payroll and other expenses. In comparison, owners typically make payment for aggregated invoices with differing degrees of back-up or breakdown of the associated costs. An owner’s requirement of cost accounting detail varies by company operating procedure, the contract delivery method, the payment requirements set forth in the owner-contractor agreement, and other guidelines. Independent of a contractor’s internal definition for direct vs. indirect cost, often times owner billing requirements insist that contractors provide accounting per specific owner-mandated guidelines.

Holland and Hobson (1999) have suggested that perspective impacts the identification guidelines for cost objects and changes whether a particular cost item is a direct or indirect cost. These researchers proposed that a particular discrete cost can be defined both as a direct cost and indirect cost depending upon the perspective of the categorizer or the definition of the cost object. For example, consider the following situation―a shared scaffolding structure used simultaneously by a masonry subcontractor to lay exterior brick veneer, a glazer to install glass and aluminum window systems and a sealant subcontractor to install caulking in the joints between the brick material and adjacent aluminum mullions. In this situation, all three activities (laying brick, installing windows and caulking joints) require the scaffolding and all three trades are using the scaffolding periodically through a workday. There is no ability to definitively associate the cost of the scaffolding directly to each of these three cost-causing trade activities.

(the defined cost object). In this perspective, all scaffolding costs are direct costs to the project.

In the initial phase of this research, much deliberation and discussion was held among the industrial team members of the research team regarding a collective definition for indirect costs. Presentation was made with regards to how casual relationships, physical incorporation and perspective impact the categorization of individual cost items. The difficulty to which this team of industry veterans struggled to form a common definition supports statements made within this dissertation that there is no universal definition for indirect costs within the construction industry and it is unlikely that any definition proposed in this research will be universally accepted. Yet, for the purposes of establishing the research charter as required by CII, the team settled on the following definition for indirect costs.

Indirect costs are supporting functions that cannot be attributed readily to a part of the final product (e.g., temporary facilities).

This author notes that the definition above defines “indirect costs.” For the purposes of this research, the author believes it is worthwhile and necessary to establish an operational definition for a more narrowly defined set of indirect costs, namely indirect construction costs (IDCC).

2.2 Indirect Construction Costs

Literature suggests that there exist no universally-accepted or shared-categorization framework within the construction industry for partitioning construction costs into direct and indirect categories (Holland and Hobson, 1999). Further, Holland and Hobson surmised that “there is little consistency among construction firms concerning what constitutes the indirect costs of performing a construction project or the indirect costs of operating a construction firm” (p. 49). David Norfleet concluded through his research that many interpretations are used by companies for the definition of indirect costs (2007). Additionally Holland and Hobson found through survey analysis that often contractors categorize certain costs as direct costs although these researchers suggest they are more correctly termed indirect costs.

Investigation of literature for a definition of indirect construction costs produced a list of many other terms used by owners and contractors in the construction industry to label indirect costs associated with capital improvement projects, e.g., general conditions, general requirements, and many others. Table 2.2 summarizes terms often used with similar or equivalent meaning to indirect construction costs. Table 2.3 provides clarification between indirect construction costs and indirect non-construction costs by providing a roster of representative cost items in these two categories.

Table 2.2: Definitions of Commonly Used Terminology Similar to or Substituted for IDCC

Terminology Definition(s) of Terminology Source

Burden “Burden is the term loosely used to describe the application of

some form of indirect cost such as overhead to a direct cost such as labor.”

Norfleet (2007)

General Conditions

1. “General conditions, also called general requirements, include the costs to administer and run the field office.” 2. “The items of work on a project related to job overhead as opposed to specific construction of integral parts of the project.”

1. Gould (2002) 2. Eppes and Whiteman (1984)

General Requirements

1. See General Conditions for reference to general requirements.

2. “In an estimate, they (general requirements) should represent all the direct costs necessary that are not directly related to specific parts of the work.”

3. See General Expenses

Table 2.2 continued

Indirect Job or Indirect Field Costs

1. “Indirect job costs are those that are not identifiable with a construction activity.” (page 50)

2. “Indirect job costs are cost necessary for the performance of a job but are difficult to identify to a specific contract.” (page 4)

3. “The indirect field costs are also referred to as general condition costs in building construction.” (p. 2) Also see job overhead.

1. Holland and Hobson (1999) 2. Shelton and Brugh (2002) 3. Dagostino and Feigenbaum (2003)

Home office overhead

“HOOH is generally described as company costs incurred by the contractor for the benefit of all projects in progress.”

Zack (2001)

General Expenses

“The general expenses of a project comprise all of the additional, indirect costs which are also necessary to facility the construction of the project. These indirect costs are sometimes titled General Requirements of the Project of Project Overhead.” (p. 313)

Pratt (1995)

General Overhead

“Costs that cannot be charged to a specific construction project or be included in the equipment costs section of the income statement.”

Peterson (2005)

General Overhead Costs

“General overhead costs are those costs that cannot be identified readily with a specific project.”

Peurifoy and Oberlender (1989) Job Overhead or Project Overhead Costs

1. “Job overhead (project overhead) is similar to general overhead but it must be distributed over the associated project, since it cannot be allocated to specific work packages.” 2. “Also referred to as general conditions or indirect field costs, jobs overhead comprises all costs that can be readily charged to a specific project but not to a specific item of work on that project.” (p. 51)

3. “Project overhead is the cost specific to a project, but not specific to a trade or work item.” (p. 33)

1. Peurifoy and Oberlender (1989) 2. Dagostino and Feigenbaum (2003) 3. Assaf et al. (1999)

Overhead costs 1. “Overhead costs are those which cannot be identified with or charged to jobs or units of production unless some more or less arbitrary allocation basis is used.” (p. 243)

2. “Overhead costs are those charges that cannot be attributed exclusively to a single product or service, or the summary of expenses that benefit more than one cost objective.” (p. 295) 3. “Overhead costs are those costs that are not a component of the actual construction work but are incurred by the contractor to support the work” (p. 295)

1. Palmer et al. (1995)

2. and 3. Assaf et al. (2001)

Direct Overhead Costs

“See Indirect Costs.” (p. 542) Peterson (2005)

Office Overhead

Office overhead is a percentage of the total yearly costs, which are incurred wither or not income is being received.

Ahuja and Campbell (1988) General &

Administrative (G&A)

Table 2.2 continued

Mark-up “Mark-up is an amount, usually stated as a percentage of cost,

added to the cost to derive a price for a product or service. It is simply profit.”

Nortfleet (2007)

Company Overhead

“Company overhead is also called general and administrative overhead and includes all the costs incurred by the construction firm in maintaining the firm in business and supporting the production process, but are not directly related to a specific project.” (page 296)

Assaf et al. (2001)

Table 2.3: Categorization of Project Costs by Indirect Construction vs. Indirect Non-Construction Costs.

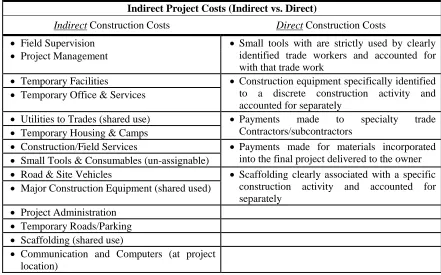

Indirect Project Costs (Construction vs. Non-Construction)

Indirect Construction Costs Indirect Non-Construction Costs

• Field Supervision • Design & Engineering (performed

pre-construction)

• Project Management • Financing & Interest

• Temporary Facilities • Contractor Profit & Fees

• Temporary Office & Services • Insurance (owner & contractor provided)

• Utilities to Trades • Owner-provided Project Management

• Temporary Housing & Camps • Home-office Services–with some exceptions

• Construction/Field Services (including cost of

testing and inspections of work in place)

• Pre-construction Services (e.g., estimating,

planning, material procurement) –with some exceptions)

• Small Tools & Consumables (un-assignable) • Bonding

• Road & Site Vehicles • Home-office Overhead (G&A) –with some

exceptions

• Major Construction Equipment (if shared used) • Geotechnical services completed

pre-construction to support the design function

• Project Administration

• Temporary Roads/Parking

• Scaffolding (if shared use)

• Communication and Computers (at project

location)

• Design & Engineering (only when performed

during the course of construction)

• Cost estimating, scheduling and material

procurement functions performed during the course of construction to support the project

• Geotechnical services completed during

CHAPTER 3: METHODOLOGY

In Chapters 1 and 2 introduced IDCC as a relevant and important topic within the context of the construction industry and summarized existing published literature regarding indirect costs and specifically IDCC. Having established a foundational understanding of IDCC, Chapter 3 outlines in detail the methodology completed for this investigation. This chapter also describes the various statistical methods conducted and software used for this research.

3.1 CII Approach to Research

Research projects sponsored by the Construction Industry Institute (CII) are completed by teams of industry representatives coupled with academic researchers. The industry team members contribute their professional experiences and provide data gained from other experts within or records from their respective companies. In the case of this research project, the 25-member research team (referred to as Research Team No. 282 or RT-282), was comprised of 19 industry representatives and 6 members of academic background (two principal investigators with Ph.D. credentials and five civil engineering/construction management graduate students, including this author). The industry members of RT-282 are professionals of significant industrial experience and are considered as subject matter experts with respect to the topic of IDCC. Table 3.2 presents the companies represented by industry members. Industry team members are purposely solicited from both owner and construction companies in order to ensure representation of both perspectives in research products.

Table 3.1: Companies Represented by Subject Matter Experts on RT-282

Owner Companies Construction Companies

Abbott Foster Wheeler

Air Products Jacobs

ConocoPhillips Shaw Group

DuPont Pioneer Hi-Bred URS Corporation

ExxonMobil Corporation Walbridge

National Institutes of Health WorleyParsons

Ontario Power Generation Zachry

3.2 Overview of Research Methodology

An overview of the research methodology is provided by first outlining the methodology in a step-by-step manner. Next, a table is provided which provides a roster of the many data collection instruments used for this research.

3.2.1 Outline of Research Methodology

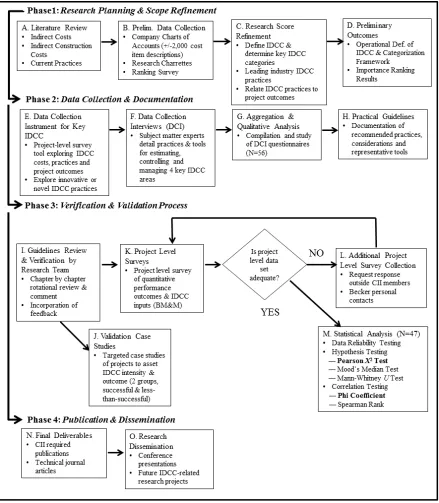

The following outline presents the research methodology, including 15 work tasks within four phases, conducted to address the research objective stated in Chapter 1.

Phase 1: Research Planning and Scope Refinement

• Work Task A: Conduct literature review regarding indirect costs and IDCC. This discovery focuses on the civil engineering and construction management-related body of knowledge but also includes the related areas of cost accounting and manufacturing.

• Work Task B: Collect charts of accounts for IDCC from numerous owner and construction companies. Conduct research charrette presentations to obtain testimony from the research team members regarding industry-used definitions for IDCC; to share how representative companies presently estimate, control and manage IDCC; and to identify common problems related to estimating, controlling and managing IDCC.

• Work Task C: Refine research scope based upon findings of the literature review and address perspectives and priorities of the research team members.

• Work Task D: Produce preliminary outcomes to strategically guide and focus the scope of the research project.

― Identify the key IDCC categories that affect construction project performance through ranking of most important IDCC categories.

Phase 2: Data Collection, Preliminary Analysis and Documentation

• Work Task E: Prepare and issue a survey instrument regarding practices and actual project costs regarding “Key IDCC” rather than “all” IDCC (this document is referred to as the Data Collection Instrument for Key IDCC).

• Work Task F: Conduct data collection interviews to investigate and document leading industry practices currently used for estimating, controlling indirect construction costs (specifically focusing on the key IDCC categories previously identified by the research team as being the most important to achieving project success). These interviews also included questions that ask what novel or innovative IDCC practices are being tested.

• Work Task G: Aggregate and analyze the data collected from Work Tasks E and F.

• Work Task H: Draft guidelines of recommended practices, considerations and practical tools for use by owners and contractors in improve estimation, control and management of IDCC.

Phase 3: Verification and Validation

• Work Task I: Perform a rotational, progressive review and edit of the preliminary version of the guidelines within the research team members. Solicit specific feedback regarding what representative tools should be included.

• Work Task J: Validate recommended IDCC practices through targeted case study investigations at the project level.

• Work Task L: If necessary, pursue collection of additional project level data as required to meet generally adopted rules of minimum dataset sizes for statistical analysis.

• Work Task M: Perform statistical analysis to test relationships between IDCC practices and project performance metrics. Correlate the direction and strength of relationships between IDCC practices and project outcomes to suggest management strategies and practices to improve the predictability of certain construction project outcomes and to ultimately increase project success.

Phase 4: Publication and Dissemination of Research

• Work Task N: Publish research findings as required by CII, including a research summary, research report, and implementation guide. Seek publication in civil engineering technical journals, e.g. ASCE Journal of Construction Engineering and Management.

• Work Task O: Make presentations of this research at appropriate academic and/or industry conferences, e.g. Construction Research Congress. Propose extensions of this work through CII and/or other funding organizations.

Fig. 3.1: Flowchart of Research Methodology by Phase & Task 3.2.2 Data Collection Instruments

survey questionnaires, research charrette templates and structured interview guides and others (refer to Table 3.2).

Table 3.2: Summary of Data Collection Instruments

Description of Research Tool

Purpose of Tool Presentation Format of

Findings

Phase 1: Research Planning and Scope Refinement Aggregated List of

Company Charts of Account Codes

• To collect and review all the many unique

cost items referred to as IDCC by industry

Aggregated Chart of IDCC Accounts (refer to

Appendix B) Research Charrette

Template

• To collect company definitions of IDCC

• To obtain testimonials from industry team

members regarding how their companies estimate, control & manage IDCC

Comprehensive list of current practices and gaps regarding estimating, controlling and managing IDCC in general(refer to Appendixes C and D) Ranking Survey of

IDCC Clusters and Categories

• To identify those IDCC cost categories which

have the greatest impact on project performance

Radar plot depicting the most impactful IDCC categories, including variance between owner and contractor perspective (refer to Appendix E) Research

Assignment Template

• To identify current practices used in industry for estimating, controlling and managing IDCC

• To identify gaps and problems in these

processes

• To solicit metrics and ratios used with IDCC

An Excel spreadsheet was compiled to aggregate the data provided through PowerPoint slides and verbal presentation (refer to Appendix F)

Phase 2: Data Collection, Preliminary Analysis & Documentation Project Level

Survey for IDCC

• To determine key indirect cost components

and their impact on total construction cost.

• To rank the impact of various indirect cost

components on total project performance.

• To identify the role innovation might play in

economizing and/or optimizing indirect construction cost components.

• To identify the potential for breakthroughs in

this topic.

Table 3.2 continued

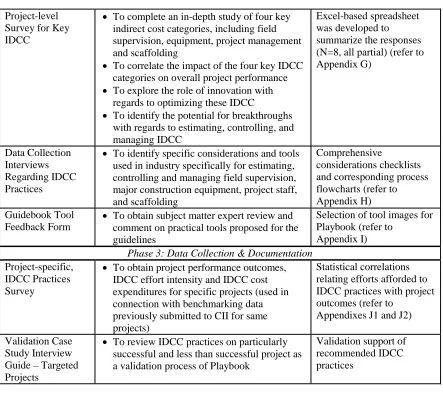

Project-level Survey for Key IDCC

• To complete an in-depth study of four key

indirect cost categories, including field supervision, equipment, project management and scaffolding

• To correlate the impact of the four key IDCC

categories on overall project performance

• To explore the role of innovation with

regards to optimizing these IDCC

• To identify the potential for breakthroughs

with regards to estimating, controlling, and managing IDCC

Excel-based spreadsheet was developed to summarize the responses (N=8, all partial) (refer to Appendix G)

Data Collection Interviews Regarding IDCC Practices

• To identify specific considerations and tools

used in industry specifically for estimating, controlling and managing field supervision, major construction equipment, project staff, and scaffolding

Comprehensive

considerations checklists and corresponding process flowcharts (refer to Appendix H) Guidebook Tool

Feedback Form

• To obtain subject matter expert review and

comment on practical tools proposed for the guidelines

Selection of tool images for Playbook (refer to

Appendix I) Phase 3: Data Collection & Documentation

Project-specific, IDCC Practices Survey

• To obtain project performance outcomes,

IDCC effort intensity and IDCC cost expenditures for specific projects (used in connection with benchmarking data previously submitted to CII for same projects)

Statistical correlations relating efforts afforded to IDCC practices with project outcomes (refer to

Appendixes J1 and J2)

Validation Case Study Interview Guide – Targeted Projects

• To review IDCC practices on particularly

successful and less than successful project as a validation process of Playbook

Validation support of recommended IDCC practices

3.3 Phase 1: Research Planning and Scope Refinement

The details of Phase 1 of the methodology is presented by first restating MRQ #1 followed by sections addressing in detail each research task completed to answer MRQ #1.

3.3.1 Master Research Question #1

Phase 1 of the research process addressed MRQ #1 restated as follows.

Within MRQ #1 are the following sub-set research questions. 1. How is indirect cost defined in published literature?

2. How do other industries, e.g., accounting or manufacturing, define indirect costs?

3. What factors can be used to partition discrete construction project costs as either IDCC or direct construction costs.

4. What categories of IDCC are perceived by industry professionals as being the most important to project success?

Extensive investigation into published academic work was conducted in the area of indirect costs, indirect construction costs, and practices and tools employed to estimate, control and manage IDCC. A summary of this literature review is presented in Chapter 2 and in part addresses MRQ #1.

3.3.2 Aggregation and Analysis of IDCC Items

A preliminary step in the research methodology included the request and submission of individual company charts of accounts by each member of the research team. Members were asked to submit a chart of accounts of all but only the IDCC items their organizations consider to be IDCC. The purpose of this effort was to build an aggregated list of all discrete project cost items that any of the member companies consider to be IDCC.

The industry members of the research team were instrumental in the review and verification of this aggregated list. Through structured deliberations by multiple sub-teams and within the research team as a whole, they reviewed both the overall categorical structure and the placement of specific IDCC items into certain groupings within a categorical framework. As a group, the team discussed particular cost items for which an individual team member was unsure of the best categorization position. This discussion, deliberation and rework resulted in both the aggregated chart of accounts and the categorization framework presented in Chapter 4.

3.3.3 Structured Research Charrettes

Phase 1 of the research methodology included specifically-designed presentations given by the industry members of the research team (referred to as “research charrettes”). These research charrettes were structured around a template format of questions furnished by the academics intended to foster a common understanding of IDCC and to explore practices and problems with respect to IDCC. The research charrettes required that each industry team member address the following items from their company’s perspective: 1) company background, 2) company’s definition of IDCC, 3) company’s strengths and weakness with respect to estimating, controlling and managing IDCC, 4) opportunities for improvement with respect to IDCC, and 5) and specific projects that had particularly strong IDCC-related performance.

3.3.4 IDCC Importance Ranking Survey

The research charrettes also provided the venue for research team debate and deliberation regarding the relationship of IDCC items and their corresponding importance to project performance. General consensus was made that not all IDCC items are equally important. The research team asserted that certain categories of IDCC have greater importance with respect to project success for two primary reasons: 1) these items have a greater impact on project success, and 2) spending on these items is typically decided at the project level, while those of other IDCC functions generally are not—these spending decisions are made at a home or corporate office. As such, the team proposed to focus the research work on those most important or key IDCC categories as would be determined by survey of the industry team members.

Consistent with the Pareto principle, the scope of the research was focused by the above reasoning. The research team decided to prioritize the 17 preliminary IDCC groupings and to identify a limited number of the most important of these groupings. To do this, 12 research team members—representing seven owner companies and five contractor companies—completed an importance ranking survey. The survey was designed to answer the following research questions.

1. Which of the 17 preliminary IDCC groupings are the most important with respect to project performance?

2. Are owner and contractor companies in agreement with respect to which of the preliminary IDCC groupings are the most important?

A Microsoft Excel-based survey instrument with pull-down selection menus was prepared and distributed by electronic mail. It asked respondents to rank order the importance of the four IDCC function clusters. It also asked respondents to rank order by importance the four or five secondary roll-up categories contained within each of the four function clusters. The following steps were followed to calculate an average weighted rank value for each of the 17 IDCC groupings.

2. Determine the average rank of each of the IDCC categories.

3. Multiply the average rank of each of the four clusters by the average rank of each of the 17 categories to calculate the weighted average of each of the 17 categories.

The weighted ranking analysis was conducted on all respondents as a whole and as groups of only contractors and owners to test for the presence of any difference in perspective of which IDCC categories are most important by respondent group. The result was a ranked order of the 17 IDCC groupings based upon the perceptions of the research team members. Additionally, the ranking data could be sorted and analyzed separately by owner and contractor respondents.

At the point of substantial completion of the literature review, research team agreement with an operational definition and IDCC categorization framework, and identification of the key IDCC categories; the research planning and scope refinement work was complete and MRQ #1 had been appropriately addressed. Phase 2, the next step, involved data collection and documentation.

3.4 Phase 2: Data Collection & Documentation

modeling could be developed to relate expenditures by IDCC category to levels of project performance.

Requests for the envisioned level of detailed cost records were made to the members of the research team, but these requests were received with resistance and confidentiality concerns. Thus, given the little response and at the direction of both the research team and CII, the data to be collected changed direction from primarily continuous scale data in money or time-based units of measurement to substantially qualitative data describing leading industry practices for estimating, controlling and managing IDCC and ordinal type data to measure the level of effort afforded IDCC practices and the resulting project outcomes.

3.4.1 Master Research Question #2

Phase 2 of the research addresses MRQ #2 restated as follows.

2. What are the leading industry practices for estimating, controlling and managing IDCC?

The methodology to address this question is discussed in this section with results provided in Chapter 5—Implementation Guidelines. Within MRQ #2 are the following sub-set research questions.

1. What considerations do industry professionals take into account when estimating IDCC, controlling IDCC, and managing IDCC?

2. What are the detailed steps in the process of estimating IDCC, controlling IDCC, and managing IDCC?

3. What tools, e.g., worksheets, check-lists, templates, do industry professionals use to estimate IDCC, to control IDCC, and to manage IDCC?

3.4.2 Pilot Project Level Survey for IDCC

this data for a large collection of projects, specifically including “all” IDCC records. The data were proposed to be used to correlate spending on specific IDCC cost items and/or categories to project performance outcomes and to develop benchmarking data for companies to compare planned spending on specific IDCC cost items to what other project spent, in particular what amounts did successful project spend on specific IDCC items. It was acknowledged that differing types of projects and differing project delivery methods may cause differing results and that data from a large population of projects would be necessary to achieve statistically valid results. To this end, a pilot survey questionnaire comprised of 14 pages was prepared and entitled a Project Level Survey for Indirect Construction Costs. In order to promote a shared vocabulary and common understanding of IDCC, the survey included the IDCC categorization framework and a glossary of other relevant terms.

As the research project advanced, opposition was expressed by the research team members that requesting the amount of project cost detail contained in the pilot Project Level Survey is both difficult to obtain and possibly a violation of corporate privacy concerns. Only one survey was submitted and it was partially completed. Therefore, consistent with the prioritization methodology explained in the prior section, the research team decided to focus its data collection specifically on only on those costs and practices related to estimating, controlling and managing the “key” IDCC categories including rather than attempting to address all IDCC on a project. It was believed that this request might be more palatable for the responding companies and therefore, more probable to be accomplished.

3.4.3 Data Collection Survey for Key IDCC

construction equipment. The research team also chose to include scaffolding as a key category as this was identified as a significant concern by the research team members representing owner companies.

The data collection instrument requested data in four sections: general project description, construction performance outcomes, key indirect cost metrics and project innovations and breakthrough opportunities. In addition to cost data and completion of the survey instrument, companies were asked to submit representative tools used within the company to demonstrate with examples how they estimate, control and manage IDCC (referred to in this research as “artifacts”). The last section of the pilot survey asked for evaluation of the instrument and the effort required for its completion. Twelve, partially completed data collection survey instruments were submitted by 12 members of the research team during the pilot distribution. A summary of the team’s feedback on the pilot survey instrument was prepared and distributed including all comments and a response to each comment. In general, the team members found the survey difficult to complete and time consuming.

Thus, the survey instrument was improved and redistributed. In the second request, five additional, however partially completed, questionnaires were submitted. The general evaluation of the data collection instrument was that it was too difficult to complete without established knowledge of the research project and without shared understanding the terminology used within the context of the research team. An alternate approach was proposed in which team members would conduct one-on-one data collection interviews with subject matter experts rather than request surveys to be independently completed by volunteer respondents.

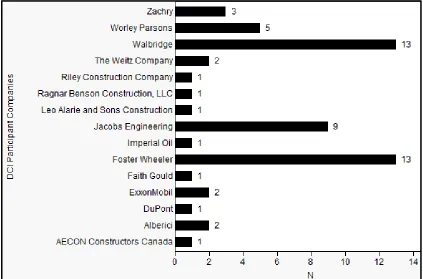

3.4.4 Data Collection Interviews

one of the specific professional service areas of estimating, controlling or managing. It was decided to substantially focus on representatives from construction companies as it was expected that owner company representatives would usually not have the detailed knowledge of specific industry practices and tools used by construction companies to estimate, control and manage IDCC.

Information collected through the data collection interviews provided the necessary data to answer the essential question presented in Section 1.2. A formal interview guide was prepared so that industry team members could independently, yet consistently, conduct interviews if they wished and so that common data were collected (refer to Appendix H). For those industry team members not interested in conducting interviews, they still made arrangements for experts they knew to be available for interview by one of the academic team members. Each interviewee was provided the interview guide in advance of the interview.

Fig. 3.2: Categorization of Project Type Experience of Subject Area Experts