doi:10.4236/ajor.2011.14030 Published Online December 2011 (http://www.SciRP.org/journal/ajor)

On Fuzzy Random-Valued Optimization

Monga K. Luhandjula

Department of Decision Sciences, University of South Africa, Pretoria, South Africa E-mail: [email protected]

Received July 27, 2011; revised August 30, 2011; accepted September 14, 2011

Abstract

In this paper, we propose a novel approach for Fuzzy random-valued Optimization. The main idea behind our approach consists of taking advantage of interplays between fuzzy random variables and random sets in a way to get an equivalent stochastic program. This helps avoiding pitfalls due to severe oversimplification of the reality. We consider a numerical example that shows the efficiency of the proposed method.

Keywords: Fuzzy Random Variables, Random Sets, Fuzzy Stochastic Optimization

1. Introduction

1.1. Background

Fuzzy Stochastic Optimization (FSO) is a worthwhile topic. It provides a glimpse into joustling with the com- plex and yet useful issue of handling situations where fuzziness and randomness are under one roof in a optimi- zation setting. Here are, without any claim for exhausti- vity, some examples of concrete problems necessitating consideration of both fuzziness and randomness: Linear regression problem in the presence of both random and fuzzy variables [1]; Renewal processes where inter-arri- val times are only known as subjective categories of the form; almost 3 hours, around 2 hours, less than 4 hours…, the occurrence of which cannot be predicted with precision [2]. An interested reader is referred to [3] where the terrain covered by FSO is surveyed. The reader may also consult [4-9] for more insights in this emerging subfield of mathematical programming under uncertainty. The presence of both possibilistic and proba- bilistic information within a mathematical programming framework is a harbinger of computational nightmares if one were to approach the problem without any simplifi- cations. Nevertheless, pitfalls due to severe oversimplifi- cation of the reality may lead to a bad caricature of the problem under consideration. In this paper the focus is on an Optimization model involving fuzzy random coef- ficients. This model comes up in several applications including optimal portfolio selection [10], inventory model [11], water resource management [12]. The com- monly used approach for solving this model is to craft a deterministic surrogate of the fuzzy stochastic optimiza-

tion at hand, by exploiting the structure available while sticking as well as possible to uncertainty principles. This approximation paradigm is central to the literature [13-15], although some researchers have questioned both its robustness and its general validity [16]. Without a serious output analysis, it is hard to ascertain both the quality of the approximation and the viability of the obtained solutions.

1.2. Contribution

In this paper, we establish a mathematical connection between fuzzy random variables and random sets. This connection is then used to get an equivalent counterpart to the original problem. The challenging task of singling out a solution of the resulting stochastic program with infinitely many objective functions is also addressed. The paper contains a systematically solved example showing the efficiency of the proposed method.

1.3. Notation

Throughout the paper will denote the set of fuzzy numbers with compact supports. If

cc

F

cc aF then a is its -level set that is a closed interval. With C

0,1 we will indicate the set of real-valued bounded functions f on [0,1] such that:1) f is left continuous for any t

0,1

0,1

2) f has a right limit for any t

Conventionally, for aFcc , , and L

a a a

0,1

C

stands for the collections of families

0,1are members of C

0,1 . We’ll use the following notation for Z

;

L,

Z Z Z . For 1 2 the distance between

0,1

, C

Z Z Z1 and

2

Z is given by:

1

1 2 1 2

0,1 , 0dH ,

C

d Z Z

Z Z d where dH denotes the Hausdorff metric. Moreover I and denote the interval [0, 1] and the indicator function of A respectively.1A

1.4. Structure of the Paper

The remainder of the paper is organized as follows. In the following section, we introduce the notions of random closed set and fuzzy random variable and we briefly discuss some of their properties. In Section 3, we prove that the set of fuzzy random variables can be embedded into the set of random closed sets isomorphically and isometrically. This embedding result is then exploited in Section 4 to describe an approach for solving mathemati- cal programs with fuzzy random coefficients. Section 5 is devoted to a numerical example for the sake of illus- tration. We end up in Section 6 with some concluding remarks along with lines for further developments in this field.

2. Random Set and Fuzzy Random Variable

2.1. Random Set

Consider a probability space

,B,P

and let F be a set of collections of subsets of . A random set in is a map:E E

F

that satisfies some measurability conditions [17]. For our purposes, and we consider random sets of the form:

E

0,1

:

( )

C

I X

X

The class of the above random sets is denoted by

R .

R can be endowed with the following metric based on the Hausdorff metric dH For

,

X YR ,

,

d

R

d X Y, dH Y P

I X d

Given X Y, R

we say that X is less or equal than Y, in symbol:

R

X Y

if , I, supX

infY

.For details on random sets, we refer the reader to [18, 19].

2.2. Fuzzy Random Variable

Consider again a probability space

,B,P

A map

:

cc

X F

X

is a fuzzy random variable if for every

0,1

and for every Borel set B of , whereis defined as follows. X 1

B B

: 2

X

X x X x .

In the sequel, the set of fuzzy random variables in the above sense is denoted by . A remarkable pro- perty of a fuzzy random variable (frv) is that Zadeh’s decomposition principle for fuzzy quantities extends naturally to frvs, that is for

F

YF ,

0,1

Y Y

.Another fundamental key fact about fuzzy random variables, which is of interest on its own right and which has a huge impact on applications is that an

-level set of a fuzzy random variable is a random interval [17]. Arithmetic operations on F

are defined as follows.Given Y Z, F

and we have:

YZ

YZ;

Y

⊙Y; Y Z if and only if Y Z, where □ and ○ indicate that operations are on

F and on Fcc

respectively. It is worthmen-tioning that and ⊙ are based on Zadeh’s extension principle [20]. Moreover, Y Z is tantamount to

IZ

Y for all (0,1] where I stands for in- equality between intervals.

We equip F

with a distance defined as follows. Given Y Z, F

,

dH

,

dF I

d Y Z Y Z Pd

As in the case of random variables, it is efficient to describe the distribution of a frv by means of certain measures summarizing some of its most relevant charac- teristics. In this way, the first two moments of a fuzzy random variable are defined as follows. The expecta- tion of a frv , in symbol is the fuzzy quantity whose

Y

Y EY

EY

f P fd is a selection of Y

.The variance of Y, in symbol VY, is given by the following relation:

F ,

VYE d Y EY

Limit theorems [22] have been obtained for frvs based on the above notions of expectation and variance.

Moreover, fuzzy random variables enjoy the Random- Nikodým property [21]. That is, if F: Fcc

is a P-continuous fuzzy measure of bounded variation, then there is YF

such that:

dB

F B

Y P, B B3. Embedding Theorem for Fuzzy Random

Variables

3.1. Auxiliary Mappings

The following three maps will play a staring role in the statement and the proof of an Embedding Theorem for fuzzy random variables.

3.1.1. Mapping

maps Fcc

into C 0,1 as follows.

0,1

:

,

cc C

L

I F

a a a

where aL

=aL and a

=a.It is well known (see e.g [23,24]) that thus defined is injective, isometric and satisfies the following relation:

For a b,Fcc

and s t, , s0, t0

1s a

1 t b

s

a t

⊙ ⊙

b .3.1.2. Mappings f and

The two other auxiliary maps are given below.

:

cc

f F F

X X

0,1

:

C F

X X

3.1.3. Remark

[image:3.595.332.515.85.185.2] [image:3.595.309.492.290.421.2]Relationships between auxiliary mappings are shown in Figure 1. The three auxiliary mappings make the dia-gram given in Figure 1 commutative.

[image:3.595.319.511.544.704.2]As a matter of fact,

f

X

X

Figure 1. Diagram involving auxiliary functions.

Therefore

of . 3.2. Main mapping

The mapping that is used in our Embedding Theorem for fuzzy random variables is defined as follows.

:

F R

X X

where

0,1

:

,

C L X

X X

and

,

,L L

I

X X X X

Relationships between the main mapping and auxiliary mappings is given in Figure 2. Mappings involved in Fig-ure 2 make the diagram given in Figure 2 commutative.

As a matter of fact, For

X X X

Hence X X .

For the sake of convenience, we identify a real number a with the following degenerate fuzzy number.

: 0

a ,1

with

X

1 if0 otherwise. t a a t

Moreover, we denote by , the degenerate fuzzy random variable:

1A A

1 :1

A cc

A F A

Building on the mappings , f, , and on the above terminological conventions, we are now ready to present the main result of this section.

3.3. Statement and Proof of the Embedding Theorem

3.3.1. Theorem 1

Consider X Y, F

; , , 0, 0and let be as in §3.2. Then the following statements hold true.

1) is injective

2) 1 X

1 Y

=XY 3) dF

X Y,

dR

X,Y

4)

R X Y X Y

In other terms maps F

into isomor- phically and isometrically.

R

Moreover, is order preserving. 3.3.2. Proof of Theorem 1

1) Let X Y, F

and assume X Y Then for we have that:

X

Y ;

X

Y

.

This means that for we have:

f

X

X f

Y

Y As is injective, we conclude that X Y for all.

Therefore X Y and we are done. 2)

1 1

1 1

1 1

1 1

1 1

X Y

X Y

f X Y

X Y

X Y

1 1

.

X Y

X Y X

X Y X Y

⊙ ⊙

Y

Therefore

1 X

1 Y

X Y

as desired. 3)

d ,

d , d

d , d

d , d

R

H I

H I

H I

X Y

X Y P

X Y P

X Y P

d

d

d .

As is isometric we have that:

d , d , d d

d , .

H I R

F

X Y X Y P

X Y

4) X Y if and only if X Y, . This is tantamount to say that:

X Y if and only if XYL , (1) As XL X and YLY, we have that (1) can be written:

if and only if

, , ,

L L

X Y

X X Y Y

(2)

(2) is equivalent toX Y if and only if

X Y if and only if

X

Y , (3) But X

Y , is equivalent to

sup X inf Y ,

or

R

X Y

.

Therefore (3) can be written: X Y if and only if

R

X Y

and we are done.

4. Solving Fuzzy Random-Valued

Optimization Problems

4.1. Case of Deterministic Feasible Set

min

1 f x

P

x X

where f:nF

and X is a convex and bounded subset of nAs is an isomorphism isometric and order preser- ving, solving

P1 is tantamount to find a solution of the mathematical program:

min

1 f x

P

x X

More formally we have, Proposition 1

*

x is an optimal solution of

P1 if and only if x* is an optimal solution of

P1.Proof

Assume x* is an optimal solution for

P1 . Then *xX and f x

* f x

x X . Then by Theorem 1 (d) we have that:

*

R

f x f

x x X

This means x* is optimal for

P1.Assume now that x* is optimal for

P1. Then *xX and f x

* f

x x X . By Theorem 1(d) again, we have that:

*

f x f x x X

and we are done

By definition of ,

P1

is equivalent to: L

min ( , (

1

0,1 ; .

f x f x

P x X

Worthy to note here is the fact that is a sto- chastic multiobjective mathematical program with infini- tely many objective functions.

P1To the best of our knowledge, there is no available solution technique for it. This is the price to pay for considering an equivalent approach to treat fuzziness instead of an approximate one. To be able to carry out a fairly discussion of we find it convenient to assu- me that:

P11) the expectation model is acceptable for tackling randomness;

2) minimizing an interval can be well handled by mi- nimizing its midpoint.

It might be pointed out in passing, that assumption 1) is often used in the literature for derandomization purposes [25,26]. Moreover, assumption 2) grants us a way for transforming intervals into real numbers. This

transformation generalizes quite canonically the real case. As a matter of fact the midpoint of

a a, is . aBearing in mind 1), 2) and considering the fact that multiplying an objective function by a constant does not alter the localisation of an optimum,

P1 may be written as follows.

min 2

0,1 ; .

L

E f x E f x

P x X

from now on,

f x

stands for

E fL x E f x Therefore (P2) reads merely:

2 min

f xP x X

I

Let’s now select a finite subset of I S, =

1,,m

and let 1,,n be real-valued functions such that: 1) j

0; I; j= 1,,m2)

1 if0 if j i

i j i j

Define a positive interpolating operator K with nodes

1, , m

as follows:

=1

= m

j j

j

Kh

h Consider now the following mathematical programs.

min3 .

Kf x

P x X

I

min 4

1, , j f x

P x X

j m

The following result bridge the gap between

P3and

P4 . Proposition 2 If *x is efficient for (P3) then *

x is efficient for (P4).

Proof

Suppose that *

x is an efficient solution for

P3and not efficient for

P4 Then there is no xX such that

*

Kf x Kf x

and

*

<Kf x Kf x for some

I (§§)

As *

x is not efficient for

P4 we have also that, there isxX such that

*

j j

f x f x

1,,m

j

and

*

<s s

x f x

f for some s

1,,m

. Consider now I

j j

arb en. As

and at:

itrarily chos we have th

0j

= 1

*

j j f x

f x

j 0 j

1,,m

and

for some

*

< 0

s f x s f x s

1,s ,m

Therefore we can say that there is xX such that:

This means, as

* =1< 0

j f x j f x

m

jj

has been chosen arbitra , that there is

rily xX such that:

*

<Kf x Kf x

I

This contradicts the fact that there is no xX such that (§) and (§§) hold.

Therefore x* is efficient for (P4).

It is a common place to say that (P3) is the same as

P2

where f x

is replaced by Kf x

Unfortuna-n be efficient for (P

tel mathe

y both

P2 and (P3) are too cumbersome for matical tractability. For practical purposes, we’ll resort to (P4) is a discretization of

P2Thanks to the contraposite of Proposition 2, we know that only an efficient solution of (P4) ca

that

3). It might also be pointed out in passing that the discretization error decreases when the grid

1, , m

S is refined [30].

This means we should keep the roughness of the grid, i.e.

1

1

, , m max min i

h h

i m I

as low as possible.

The foregoing discussion leads us to describe the for solving

following algorithm

P1 . Description of the algorithmStep 0: Fix 0an acceptable bound of error for

e (P

h. Step 1: Read data of (P1).

Step 2: Fram 1) as

P2. Step 3: Put 0.Step 4: Take a discretization of e (P4)

r (P4).

1

, , , m

I S .

Step 5: Writ .

Step 6: Find an efficient solution fo

Step 7: Compute hmaxImin1 i m i and ch-

eck whether h <.

If this is true, go t Otherwise

o Step 9, go to Step 8.

tization , put Step 8: Take a finer discre S SS an

4. zy Random Constraints

ation pro- lem.

d go to Step 5.

Step 9: Print the solution obtained. Step 10: Stop.

2. Case of Fuz

Here we are interested in the following optimiz b

5; = 1, ,

i i

P minf x

g x b i m

, i, = 1, ,

f g i m n

and

where are fuzzy random func-

tions of

-valued

i

bF ; ider the followin

= 1, , i m.

Cons g optimization problem:

6 min

; = 1, ,

f x P

i R i

g x b i m

Before stating a result that bridges the ga between p

P5 and

P6 , we introduce the following respective surrogates to

P5 and

P6 respectively.

P5 f x

minx X

min

6 f x

P

x X

X and X

where are deterministic counterparts of

the following sets respectively:

n ; = 1, ,

i i

x g x b i m

and

n ; = 1, ,

i R i

x g x b i m

Proposition 3

is an optimal solution for

P5 if and only if*

x

*

x is optimal for

P6 . ProofBy Theorem 1 (d), we have that XX Moreover by Proposition 1,

P5 and

P6 are equivalent.(P5) an

lve (P have

equivalent. To so 5) we to consider

P6

an

amp

we consider the following mple example.

d then apply the method described in the previous section for solving

P2 .5. Numerical Ex

le

For the sake of illustration, si

max c x c x

1 12 2

1 2

1 2

1 2

8

2 3 19

0; 0 E x x P x x x x

where c1 and c2 are fuzzy random variables defined

on

1, 2

with

1 15 P p 2 and

2 23 5

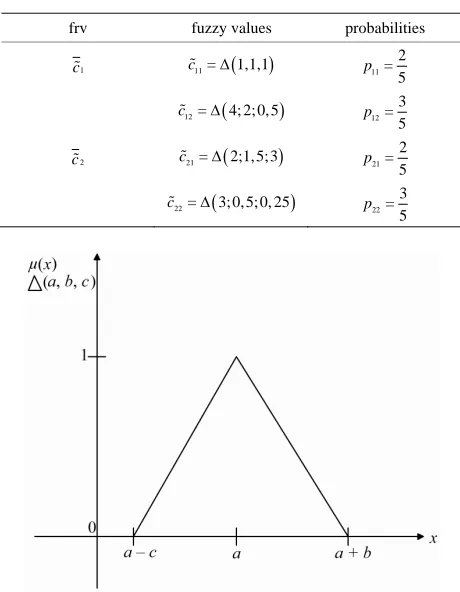

[image:7.595.56.286.411.707.2]P p Details on the two frvs are given in Table 1.

a b c, ,

stands for a triangular fuzzy number with membership a b c, , defined as in Figure 3.

According to Proposition 1,

PE is equivalent to thefollowing mathematical program:

Table 1. Details on frvs c1 and c2.

frv fuzzy values probabilities

1

c c11=1,1,1 11=

5 p 2

12= 4; 2; 0, 5

c 12

3 = 5 p 2

c c21=2;1, 5;3 21 2 =

5

p

22= 3; 0, 5; 0, 25

c 22

3 =

5

p

1 1 2 2

1 2

1 2

1 2

max 8

2 3 19

0; 0

E

c x c x x x P x x x x

= 1 1 2 2f x c x c x and

P2 reads:Here

1 1 2 2

1 1 2 2

1 2 1 2 1 2 max 8 2 3 19

0; 0

L L

E

E c x c x

E c x c x

x x P x x x x ; I

Let 0, 25 and consider the following discretiza- tion of I;

= 0; 0, 25; 0, 5;0, 75;1 S

with this grid, takes the form:

ideri g d ( 4)P

11 11 1 12 1 2

22 22 2 11 11 1 12 12 1

21 21 2 22 22 2

1 2 1 2 1 2 max 8

2 3 19

0; 0

0; 0, 25; 0, 5; 0, 75;1 L

L

E

p c x p x

p c x p c x p c x

p c x p c x

P x x x x x x

12 21 21

L L

c p c x

Cons n ata of Tables 1-3,

PE becomes:

1 2 1 2 1

1 2 1 2

1 2

1 2

1 2

max 6, 5 4, 75 , 6, 27 4, 05 4, 97 ,

5,82 5, 08 ,10, 4 5, 2

2 3 19

0; 0

[image:7.595.305.540.639.723.2]86 , 6,

Figure 3. Triangular fuzzy number delta (a, b, c).

2

8

x x x x

x x x x

x x x x x x

A Pareto optimal solution of this multiobjective pro- gram may be obtained by solving the following weighting program.

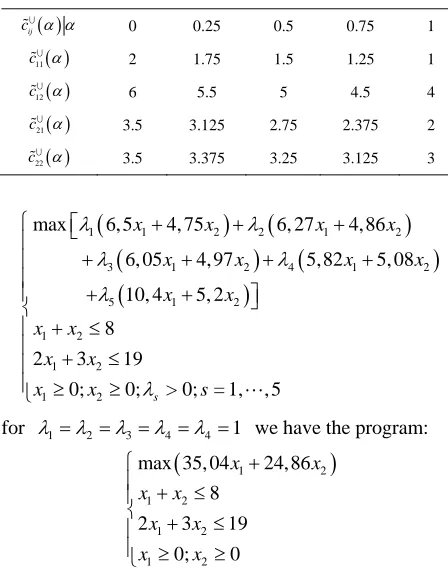

Table 2. Left endpoints of α-level cuts of

x x ij c . L ij

c 0 0.25 0.5 0.75 1 L

ij

c 0 0.25 0.5 0.75 1

11 L

c 3.5 3.625 3.75 3.875 4

21 L

c –1 –0,25 0.5 1.25 2

22 L

Table 3. Right endpoints of α-level cuts of cij.

ij

c

0 0.25 0.5 0.75 1

11

c 2 1.75 1.5 1.25 1

12

c 6 5.5 5 4.5 4

21

c

3.5 3.125 2.75 2.375 2

22

c

3.5 3.375 3.25 3.125 3

1 1 2 2 1 2

3 1 2 4 1

5 1 2

1 2

1 2

1 2

max 6, 5 4, 75 6, 27 4,86

5, 0

, 4

8

2 3

> 0 , , 5

s

x x x x

2

6, 05 4, 97 5,82 8

10 5, 2

19

0; 0; ; = 1

x x x

x

for

x

x x

x x

x x

x

s

1 2 3 4 4 1

we have the program:

1 2

max 35, 04 24,86

1 2

1 2

1 2

19

0; 0

8

2 3

x x

x

x

x x

x x

which yields the solution LINGO

software th ugh all, this

solution is a good approxim n o he

riginal problem

8,

*

0

x

the grid

atio the

using is sm

. As e ro ness of h

n of solutio f t

o

PE6. Concluding Remarks

Though significant progress has been made in recent years on Fuzzy Stochastic Optimization [3-7], there a e from an algorithmic point of view, many challenges remaining. Developing effective and efficient techniques for handling such problems still remain an important issue. This paper has been written to address some of the

e mentioned challenges. It

references for those whose appetite has been sufficiently whetted that they are hungry for more.

It might be pointed out that a general m thodology for solving Fuzzy Stochastic Optimization problems has been outlined in [3]. The quintessential of that methodo- logy is to perform a couple of transformations (possibili- r

abov is also filled with many

e

stic and probabilistic) say f1 and f2 either sequen-

tially or in parallel in a way to put the original problem into deterministic terms.

To be in tune with ncertainty principles [22], these u troduce possibilistic at a more fundam vel. They should also capture the essence of invo transformations should be able to in

and probabilistic information ental

lved le

fuzziness and randomness. This is the reason why, in this paper, we found it convenient not to let both f1 and f2

be mere approximations. The possibilistic transformation is an equivalence obtained from connections between fuzzy random variables and random closed sets. There- fore our approach contrasts markedly with those where approximation of fuzzy values by real ones is followed by approximation of random variables by their moments [7]. It also differs form approaches base fu sto

y

ear optimization problems m

d on

zzy-. The chastic simulation [28]. Moreover, our approach can handle both linear and non linear optimization problems. It is also less demanding in terms of information that the decision maker should provide before having his problem solved. This departs strongl with extant methods as illustrated by the following sample. In [4,5] for example, emphasis is placed on lin

ethod described in [28] is based on the assumption that involved fuzzy random variables are of the LR type. Techniques discussed in [6,29] require that the decision maker be able to set appropriate targets and suitable thresholds or to manipulate complex indexes. The price to pay for using the method described here is t computational challenge brought up by the resulting problem that is a stochastic program with infinitely many objective functions. An algorithm for solving this pro- blem has be presented. An efficient implementation and numerical testing of the proposed algorithm is a topic of future research.

7. References

[1] H. Bandemer and W. Gerlach, “Evaluating Implicit Func-tional Relationships from Fuzzy Observations,” Freiber-ger Forschungshefter, Vol. D170, 1985, pp. 101-118. [2] C. M. Hwang, “A Theorem of Renewal Process for Fuzzy

Random Variables and Its Application,” Fuzzy Sets and Systems, Vol. 116, No. 2, 2000, pp. 237-244.

doi:10.1016/S0165-0114(98)00143-2

he

[3] M. K. Luhandjula, “Fuzzy Stochastic Linear Program-ming: Survey and Future Research Directions,” European Journal of Operational Research, Vol. 174, No. 3, 2006, pp. 1353-1367. doi:10.1016/j.ejor.2005.07.019

[4] H. Katagiri, E. B. Mermri, M. Sakawa, K. Kato and I. Nishizaki, “A Possibilistic and Stochastic Programming Approach to Fuzzy Random MST Problems,” IEICE- Transactions on Information Systems, Vol. E88-D, No. 8, 2008, pp. 1912-1919.

[5] H. Katagiri, M. Sakawa, K. Kato and I. Nishizaki, “In-teractive Multiobjective Fuzzy Random Linear Program-ming: Maximization of Possibility and Probability,” Eu-

l of Operational Research, Vol. 188, No. 2, 539. doi:10.1016/j.ejor.2007.02.050

ropean Journa 2008, pp.

5, 2001, pp. 713-720. doi:10.1109/91.963757

[7] Y. K. Liu and B. Liu, “A Class of Fuzzy Random Opti-mization: Expected Value Models,” Information Sciences, Vol. 155, No. 1-2, 2002, pp. 89-102.

doi:10.1016/S0020-0255(03)00079-3

[8] Y. K. Liu and B. Liu, “Fuzzy Random Programming with Equilibrium Chance Constraints,” Information Sciences, Vol. 170, No. 2-4, 2005, pp. 363-395.

doi:10.1016/j.ins.2004.03.010

[9] E. E. Ammar, “On Fuzzy Random Multiobjective Quad-ratic Programming,” European Journal of Operational Research, Vol. 193, No. 2, 2009, pp. 329-341.

doi:10.1016/j.ejor.2007.11.031

[10] Z. Zmeskel, “Value at Risk Methodology under Soft Conditions Approach (Fuzzy-Stochastic Approach),” Eu- ropean Journal of Operational Research, Vol. 161, No. 2, 2005, pp. 337-347. doi:10.1016/j.ejor.2003.08.048

[11] P. Dutta, D. Chakraborty and A. R. Roy, “A Single-Pe- riod Inventory Model with Fuzzy Random Variable De-mand,” Mathematical and Computer Modelling, Vol. 41, No. 8-9, 2005, pp. 915-922.

doi:10.1016/j.mcm.2004.08.007

[12] F. Ben Abdelaziz, L. Enneifar and J. M. Martel, “A Mul-tiobjective Fuzzy Stochastic Program for Water Resource Optimization: The Case of Lake Management,” 2005. http://www.sharjah.ac.ae/academi/

[13] M. K. Luhandjula, “Optimization under Hybrid Uncer-tainty,” Fuzzy Sets and Systems, Vol. 146, No. 2, 2004, pp. 187-203. doi:10.1016/j.fss.2004.01.002

[14] C. Mohan and H. T. Nguyen, “An Interactive Satisfying Method for Solving Multiobjective Mixed Fuzzy Sto-chastic Programming Problems,” Fuzzy Sets and Systems, Vol. 117, No. 1, 2001, pp. 61-79.

doi:10.1016/S0165-0114(98)00269-3

[15] S. Nanda, G. Panda and J. Dash, “A New Solution Method for Fuzzy Chance Constrained Programming Problem,” Fuzzy Optimization and Decision Making, Vol. 5, No. 4, 2006, pp. 355-370.

doi:10.1007/s10700-006-0018-8

[16] W. M. Kirby, “Paradigm Change in Operations Research: Thirty Years of Debate,” Operations Research, Vol. 55, No. 1, 2008, pp. 1-13. doi:10.1287/opre.1060.0310

[17] R. Kruze and K. D. Meyer, “Statistics with Vague Data,” Reidel, Dordrecht, 1987. doi:10.1007/978-94-009-3943-1

[18] I. Moklanov, “Theory of Random Sets,” Springer, New

Sets and Systems: The-Press, New York, 1980.

383- York, 2005.

[19] G. Matheron, “Random Sets and Integral Geometry,” John Wiley & Sons, New York, 1975.

[20] D. Dubois and H. Prade, “Fuzzy ory and Applications,” Academic

[21] J. Bán, “Radon-Nikodyým Theorem and Conditional Expectation of Fuzzy-Valued Measures and Variables,” Fuzzy Sets and Systems, Vol. 34, No. 3, 1990, pp. 392. doi:10.1016/0165-0114(90)90223-S

[22] E. P. Klement, M. L. Puri and D. A. Ralescu, “Limit Theorems for Fuzzy Random Variables,”Proceedings of the Royal Society A, Vol. 407, No. 1832, 1986, pp. 171- 182. doi:10.1098/rspa.1986.0091

[23] C. X. Wu and M. Ma, “Embedding Problem of Fuzzy Number Space,” Fuzzy Sets and Systems, Vol. 44, No. 1, 1991, pp. 33-38. doi:10.1016/0165-0114(91)90030-T

[24] H. C. Wu, “Evaluate Fuzzy Optimization Problems Based on Biobjective Programming Problems,” Computer and Mathematics with Applications, Vol. 47, No. 6-7, 2004, pp. 893-902. doi:10.1016/S0898-1221(04)90073-9

[25] P. Kall, “Stochastic Linear Programming,” Springer, New York. doi:10.1007/978-3-642-66252-2

[26] S. Vajda, “Probabilistic Programming,” Academic Press, New York, 1972.

[27] G. J. Klir, “Principles of Uncertainty: What Are They? Why Do We Need Them?” Fuzzy Sets and Systems, Vol. 74, No. 1, 1995, pp. 13-31.

doi:10.1016/0165-0114(95)00032-G

[28] J. Li, J. Xu and M. Gen, “A Class of Multiobjective Lin-ear Programming Model with Fuzzy Random Coeffi-cients,” Mathematical and Computer Modelling, Vol. 44, No. 11-12, 2008, pp. 1097-1113.

doi:10.1016/j.mcm.2006.03.013

[29] V. H. Nguyen, “Solving Linear Programming Problems under Fuzziness and Randomness Environment Using Attainment Values,” Information Sciences, Vol. 177, No. 14, 2007, pp. 2971-2984.

doi:10.1016/j.ins.2007.01.032

[30] K. Glashoff and S. A. Gustafson, “Linear Optimization and Approximation,” Springer-Verlag, Berlin, 1983.