A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 1

HUMAN RESOURCE ACCOUNTING PRACTICES IN SATYAM

COMPUTERS SERVICES LTD

DR. Reeta

Assistant Professor, Department of Commerce Zakir Husain Delhi College, University of Delhi

ABSTRACT

The Employees are the most valuable among all available resources in the service sector. They, like the other resources of the company, possess value as they provide future services. It would thus be a worthwhile exercise identifying and measuring the value of human capital. With increasing knowledge and skills the economy has become more dependent on its human resources thereby making it an integral part of success. The growth of the software companies all over the world depend on its human and intellectual resources thereby making retention and maintenance of these a primary aim of all employers. These employees are assets that appreciate in value through the skill, knowledge and experience they acquire while working in the organization. Their departure from the organization makes the business lose an essential element of intellectual capital. This loss becomes great if such intellectual element is acquired by a rival business concern and that makes the valuation of this asset essential for the success of the company and by reporting it to the public it also enhances the image of the company. Satyam became the second software company to value its human resources in India. In the present paper an attempt is made to critically discuss the human resource accounting practices followed by Satyam computers Services Ltd.

Key Words: Human Resources, Human Resource Accounting, Satyam, Lev & Schwartz Introduction

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 2 energies, skills, talents and knowledge of people that are or can be potentially applied to the production of goods or rendering useful services. The quality and caliber of the people working in an organization are its real assets. A sick concern can be transformed into a successful one by a team of competent, devoted and motivated persons. On the other hand, incompetent and unmotivated personnel may not only squander away the existing physical and financial resources but also push the concern into bankruptcy. Henry Fayol, a French Management writer, on taking charge found his company to be on the verge of bankruptcy. Through his managerial ability, in a short span of time, he turned the company into a successful one. Corporations cannot run machines or systems alone, however smart they may be, as the human element in it is inevitable. Therefore one cannot dispute the fact that “people are the most important assets of an organization.”

Yet accounting has concentrated on the physical and financial resources of an entity without bringing this “vital ingredient of social system” into its fold and in the process, forgetting that the performance of an enterprise itself is the product of human activity and the failure of most of the companies is because of the poor performance of its people.

The American Accounting Association (1973) defines Human Resource Accounting as “the process of identifying and measuring data about human resources and communicating this information to interested parties.” This definition considers HRA as the application of basic functions of accounting, viz., identification, measurement and communication. Thus HRA may be considered as an information system that reveals the data about human resources to the management and other interested parties.

Approaches to HRA

A number of approaches have been suggested and developed for the measurement and valuation of human resources. These may broadly be classified into two types:

1. Human Resource Cost Accounting

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 3 made by the organization towards acquisition and development of human resources as well as the replacement of cost of the people employed.

2. Human Resource Value Accounting.

Human Resource Value Accounting is based on the view that the difference in the present and future earnings of two similar firms is due to the difference in their human assets. The economic value of the firms can be determined by obtaining the present value of future earnings. A number of valuation models have been developed for determining the present value of future earnings.

Review of Literature

The importance that Emperor Akbar gave to his nine jewels is a strong evidence for the same. The history of our freedom movement will not be complete without mentioning the names of distinguished freedom fighters like Moti Lal Nehru, Mahatma Gandhi, Sardar Vallabh Bhai Patel and several others but no effort was made to assign any monetary value to such individuals in the balance sheet of the nation.

Sir William Petty was the pioneer in this direction. The first attempt to value the human resource in monetary terms was made by him in 1961. Petty considered that labour was the „father of wealth‟ and it must be included in any estimate of national wealth without fail. The real work started only when behavioural scientists vehemently criticized the conventional accounting practice of not valuing the human resources along with other resources. Rensis Likert in 1960s was the first to emphasize the importance of strong pressures on the HRs qualitative variables that can be divided into three categories:

i) Casual ii) Intervening iii) End-result

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 4 The development of HRA as a systematic and detailed academic activity, according to Eric G Flamholtz (1999), began in the sixties. He divides the development into five stages that are: First Stage (1960-66)

This marks the beginning of the academic interest in the area of HRA. However the focus was primarily on deriving HRA concepts from related bodies of theories.

Second Stage (1967-70)

The focus in this was on developing and validating different models for HRA. The aim was to develop some tools that would help the organizations in assessing and managing their human resources. One of the earliest studies here was that of Roger Hermanson. In his doctoral research he studied the problem of measuring the value of human assets as an element of goodwill. Many research projects were taken up by researchers to develop concepts and methods taking the inspiration from the Roger study.

Third Stage (1971-77)

This was the period of rapid growth of interest in HRA. It involved a significant amount of academic research throughout the western world, Australia and Japan. It was a time of early attempts to apply the HRA theory to business organizations. During this stage the R G Barry experiment continued and received considerable recognition because at least for a few years the company published performa financial statements that included human assets. Various research studies were conducted to find the impact of HRA in decision making. (2006-07/2005-06 9-10) Fourth Stage (1978-1980)

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 5

Fifth Stage (1980 onwards)

From early 1980s interest in HRA again rekindled as competition among the organizations had intensified and most of the developing economies had shifted from manufacturing to service economies. Whereas it has been agreed that valuation and accounting for human resources is necessary, the problems associated with such processes have not been resolved.

Objectives of the study

The Human Resources are fundamental to all available resources of an economy or an organization. Accounting of this valuable asset plays a significant role in decision making especially in the service sector where the human resources play a major role.The main objective of the present paper is to critically evaluate the human resource accounting practices followed by Satyam Computers Limited.

Research Methodology

After Infosys, Satyam was the Software Company that initiated the reporting practices of human resource valuation in its annual reports. Therefore this company is selected randomly for the purpose of the study. To know the detailed reporting system followed by Satyam for human resource valuation annual reports of the company were scanned for a period of 2003-04 to 2010-11. From the information supplied in the annual reports certain ratios have been calculated to do the comparative study of HRA status during the five year period i.e. 2003-04 to 2007-08 as it stopped reporting human resource accounting after 2007-08.

SATYAM COMPUTERS SERVICES LIMITED

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 6 Indian internet companies to be listed on NASDAQ. Satyam Computers network is spread over 55 countries across six continents serving over 558 global companies.

There are over 40,000 employees on its rolls. Satyam with its high and steady vision believes that the real strength of the balance sheet of a company is reflected only if its tangible and intangible assets are taken into account. Satyam being in the knowledge based industry with the global operations, valuation of its human resources and brand is highly important and could be equally insightful to the stakeholders. It is a front runner in taking stock of and valuing the intangible assets.

In June 2009 the beleaguered Satyam Computer Services was acquired by Tata Mahindra and the company became Mahindra Satyam. The company after this also stopped reporting its tangible assets value in the annual reports.

Human Resource Accounting System of Satyam

Satyam being a knowledge based industry with global operations believes that the conventional approach to valuing business hardly reflects the true picture of financial position. This is because it does not take into account the cumulative value of intangible assets that play such a decisive role in modern business building initiatives. As per the company‟s opinion HR challenge for any organization is its capability building and enhancement and associate engagement. The company continued to work towards these components through various initiatives. Satyam started valuation of human resources in the year 2002 by publishing this data under the heading „additional information to investors‟.

Satyam used Lev and Schwartz model for calculating the human resource value. The valuation is based on the present value of future earnings upto retirement age with the following assumptions:

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 7 * The future earnings have been discounted at the weighted average cost of capital for the past five years. Different discount rates are used based on cost of capital as shown in Table1 for different years.

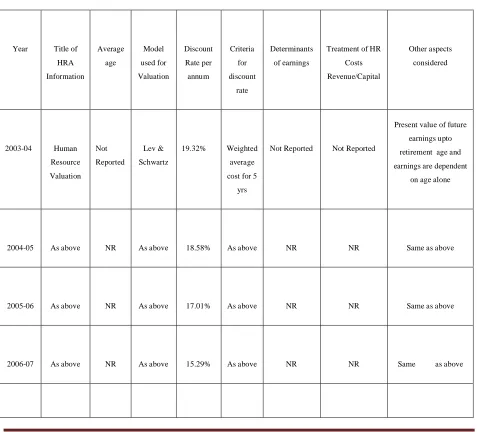

[image:7.612.67.544.274.706.2]Table 1 gives an overview of various aspects considered by Satyam for valuation of its human resources for the period 2003-04 to 2007-08 as Satyam stopped reporting this information after 2007-08 in their annual reports. Two aspects that are important for human resource valuation i.e. the average age and treatment of HR costs were not disclosed by Satyam.

Table 1 Various Aspects Considered for Valuation of Human Resources by Satyam

Year Title of

HRA Information

Average

age

Model

used for Valuation

Discount

Rate per annum

Criteria

for discount

rate

Determinants

of earnings

Treatment of HR

Costs Revenue/Capital

Other aspects

considered

2003-04 Human

Resource

Valuation Not

Reported

Lev &

Schwartz

19.32% Weighted

average

cost for 5 yrs

Not Reported Not Reported

Present value of future earnings upto

retirement age and

earnings are dependent on age alone

2004-05 As above NR As above 18.58% As above NR NR Same as above

2005-06 As above NR As above 17.01% As above NR NR Same as above

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 8

2007-08 As above NR As above 14.26% As above NR NR Same as above

Source: Annual Reports of Satyam for 2003-04 to 2007-08.

Trends in Structure and Value of Human Resources of Satyam

In Table 2 trends in structure and value of human resources of Satyam during the period of 2003-04 to 2007-08 has been shown. Table 1 clearly indicates that for valuation purpose associates i.e. employee‟s strength is divided into development and support categories. During the year 2003-04 the total number of associates was 14032 as against 9759 associates in the previous year. The company‟s attrition rate was 17.46% as on 31.3.2004.

Table 2 Trends in Structure and Value of Human Resource of Satyam

Year 2003-04 2004-05 2005-06 2006-07 2007-08

Category No of

employe es Value of HR (Rs in crores) No of employe es Value of HR (Rs in crores) No of employe es Value of HR (Rs in crores) No of employe es Value of HR (Rs in crores) No of employe es Value of HR (Rs in crores) Developme nt 13120 (93.50) 11314.7 5 (95.99) 17859 (93.19) 15886.3 1 (95.78) 24801 (93.55) 22203.0 6 (95.03) 33812 (94.79) 39319.7 6 (96.13) 43279 (94.15) 53354.5 3 (95.63)

Support 912

(6.50) 473.09 (4.01) 1305 (6.81) 700.10 (4.22) 1710 (6.45) 1161.49 (4.97) 1858 (5.21) 1581.79 (3.87) 2690 (5.85) 2440.50 (4.37)

Total 14032

(100.00) 11787.8 4 (100.00 ) 19164 (100.00) 16586.4 1 (100.00 ) 26511 (100.00) 23364.5 5 (100.00 ) 35670 (100.00) 40901.5 5 (100.00 ) 45969 (100.00) 55795.0 3 (100.00 )

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 9 Out of a total of 14032 associates 13120 (93.5%) belong to the development category and the rest 912 (6.5%) come under the support category. The total number of associates increased from 14032 (2003-04) to 45969 (2007-08). Table2 clearly shows that from 94-95% associates in different years belong to the development category whereas 4-6 % associates fall under the support category. The total number of associates as on March 31, 2008 was 45959 against 35670 on March 31, 2007. The attrition rate for the year 2007-08 was 13.09%. The human resource value also increased from Rs.11787.84 crores in 2003-04 to Rs.55795.03 crores in 2007-08. This is due to the increase in number of associates from 14032 to 45969. The discount rate per annum that fell from 19.32% (2003-04) to 14.26% (2007-08) is also one of the causes of increase in the value of human resource.

Productivity and Performance Ratios of Human Resources of Satyam

In Table 3 an attempt has been made to analyze productivity and performance of human resources of Satyam by selecting few important parameters. There was an upward trend in the value of human resources per employee over the period of five years i.e. 2003-04 to 2007-08. The percentage increment over the last year in the value of human resources per employee varies from 1.15 to 30.68. The lowest increase over the last year was noticed in the year 2005-06 (1.15%) and the highest increase over the last year was in the year 2006-07 i.e. 30.68%

Table 3 Productivity and Performance Ratios of Human Resources of Satyam

Year Ratios 2003-04 2004-05 2005-06 2006-07 2007-08

Value per employee (Rs in crores)

0.84 0.87 0.88 1.15 1.21

(3.57%) (1.15%) (30.68%) (5.22%)

Value added per

employee (Rs in crores) 0.15 0.15 0.16 0.15 0.16

(0.0%) (6.67%) (-6.25%) (6.67%)

Value added/HR

(Rs in crores)

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 10

(-0.1%) (5.88%) (-27.78%) (0.0%)

Value per

employee/Value

added per employee

(No. of years)

5.6

5.8

5.5

7.67

7.56

HR/Total Resources

82%

84%

84%

88%

88%

Profit before

Tax/HR

5.62%

5.23%

6.19%

3.85%

3.48%

Source: Annual reports of Satyam for 2003-04 to 2007-08

Value added is the wealth the company has been able to create by its own and its employee‟s efforts during a period. Though Satyam annual reports do not disclose the value added statement but value added is calculated from information available in its annual reports. The value per employee increased at the rate of 5.22% over the last year during 2007-08 and there is 6.67% increase in value added per employee during this period over the last year. This shows that during this period of one year employees contribution was more than the compensation made to them by the organization. Similar is the case in 2005-06 over the last year. In contrast the situation is reverse in 2003-04 and 2006-07. During these years employees were compensated more by the organization than their contribution to the organization.

The ratio of value added to human resources decreased from Rs.0.18 crores in 2003-04 to Rs.0.13 crores in 2007-08. This is an indicator of decrease in the productivity of human resources of Satyam. Due to this decrease in productivity the number of years it takes to recover the investment made in human resources also increased from 5.6 years to 7.56 years.

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 11

Evaluation of HRA System of Satyam

The company also uses Lev and Schwartz Model for valuation of its human resources and it disclosed HRA information under the head “additional information for investors”. Satyam not only value its intangibles but also disclosed value of intangibles in its balance sheet including intangibles for the convenience of the investors. The value of human resources is shown on the asset side of the balance sheet under the head human resource value and for the same amount it has been included in intangible reserves on liability side. Though Satyam disclosed all this information but the system of valuation of HRA in Satyam also suffers from the inherent limitations of Lev and Schwartz Model.

The information related to age-structure of human resources is significant since it provides an outlook of the composition of human resources. Though it is not directly related with the accounting of human resources, it certainly helps to determine the expected remaining service life of human resources. Satyam has also not reported average age of employees.

Recommendations

Human Resource Accounting has a great potential in the modern age of professionalization, particularly in the case of labour intensive service industry where human resource constitutes the prime resource. HRA information thus would be of immense help in decision making both for internal and external users. Therefore all organizations should adopt HRA system.

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 12 along with other professionals, researchers and accounting bodies both at the national and international levels for the measurement and reporting of such valuable assets. Researchers should come forward to review the models as per the requirements of our country.

Limitations of the study

This study is based on secondary data. Information disclosed by the company in their annual reports has been used for the purpose of study. The limitation is that secondary data influence the study. No comparisons can be made as the study is restricted to only one company.

References

AAA Committee. (1973). Report of the AAA Committee on Accounting for Human Resources,

The Accounting Review, 48,189.

Brummet,R.L, Eric G. Flamholtz and William C. Pyle. (1968). Human Resource Management: A Challenge for Accountant. The Accounting Review, 43 (2), 217-224.

Dasgupta, N.D. (1990). Human Resource Accounting. Sultan Chand and Sons, New Delhi. Giles,W.J. and Robinson, D.F. (1972). Human Asset Accountants. Institute of Personnel Management and Institute of Cost and Management Accountants, London.

Gul, Ferdinand A. (1984). An Empirical Study of the Usefulness of Human Resources Turnover Cost in Australian Accounting Firms. Accounting Organization and Society, 9, 233-239.

Gupta, D.K. (1990). The Lev and Schwartz Model Based Human Resource Accounting in India: Some Issues. Indian Journal of Accounting, 20(1), 79-81.

Hekimian, J.S and Jones, C.H. (1967). Put People on Your Balance Sheet. Harvard Business Review, 107-108.

Hermanson, Roger H. (1964). Accounting for Human Assets. Occasional Paper No. 14, Graduate School of Business Administration, Michigan State University, 1-69.

Jaggi, Bikki and Hon-Shiang Lau. (1974). Towards a Model for Human Resource Valuation. The Accounting Review, 321.

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

International Research Journal of Human Resources and Social Sciences (IRJHRSS)

Website: www.aarf.asia. Email: [email protected] , [email protected] Page 13 Flamholtz, Eric G. (1972). Towards a Theory of Human Resource Value in Formal Organizations. TheAccounting Review, 48 (4), 666-678.

Likert, Rensis. (1967). The Human Organization: In Management and Value. McGraw Hill Book Co, New York, 83-84.

Lev, B and Schwartz, A.(1971). On the use of the Economic Concept of Human Capital in Financial Statements”, Accounting Review, 103-112.

Morse, W. J. (1973). A Note on the Relationship between Human Asset and Capital. The Accounting Review, 5.

Ogan, Pekin.A. (1976). Human Resource Value Model for Professional Service Organizations

The Accounting Review, 51 (2), 306.

Paton, William A. (1962). Accounting Theory. Chicago American Studies Press, 448-487.

Schwan, E.S. (1976). The Effects of Human Resource Accounting Data on Financial Decisions: An Empirical Test. Accounting, Organization and Society, 1, (2), 219-237.