Voluntary Disclosure of Listed Chinese Companies~2008-2012: An Empirical Study

Full text

Figure

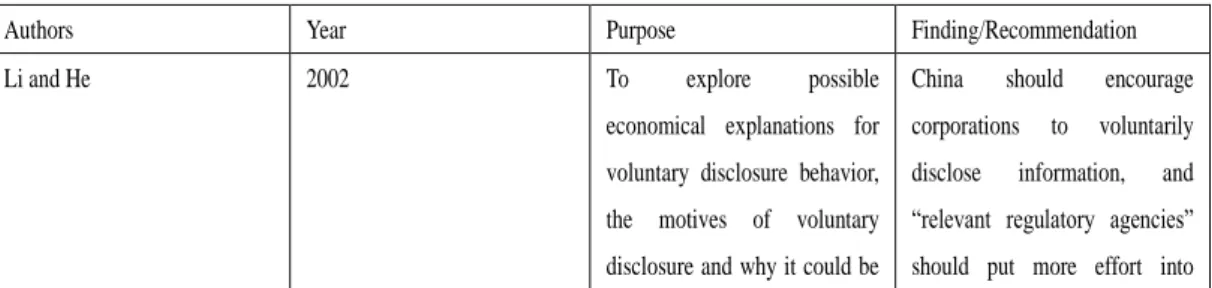

![Table 3]: Summary of empirical Chinese studies undertaken on Voluntary Disclosure](https://thumb-us.123doks.com/thumbv2/123dok_us/111853.2512834/35.892.159.766.707.1154/table-summary-empirical-chinese-studies-undertaken-voluntary-disclosure.webp)

Outline

Related documents

Typical activities during the operations of terminal facilities include receiving and unloading of products from ships, rail tankers, trucks, and pipelines; storage and handling

Where they exist, roles described include leadership and management of medical staff; strategic development and advising executives; clinical governance, including quality and

The LH Martin Institute for Higher Education Leadership and Management has been established by the Australian Government to enhance tertiary education in Australia and New Zealand

At the assessment stage a training provider is assessed against ACRRM and RACGP Standards using the Bi-College Accreditation Principles and Outcomes.. The Accreditation Review

1998 Member of the Complementary Therapies Workgroup, National Arthritis Foundation 2002-04 Chair, Behavioral Rheumatology Study Group, American College of Rheumatology

[r]

Participants came from various library stakeholders such as the National Library Service, Information management students representative, Ministry of Education,