Pricing Better

Ray, Sourav and Wang, Li and Levy, Daniel and Bergen,

Mark

McMaster University, McMaster University, Bar-Ilan University,

Emory University, and RCEA, University of Minnesota

16 August 2019

Online at

https://mpra.ub.uni-muenchen.de/95596/

Pricing Better

Sourav Ray**

Department of Marketing, McMaster University Hamilton ON L8S 4M4, CANADA

Li Wang

CHEPA, McMaster University Hamilton ON L8S 4M4, CANADA

Daniel Levy

Department of Economics, Bar-Ilan University Ramat-Gan 52900, ISRAEL,

Department of Economics, Emory University Atlanta, GA 30322, USA, and

Rimini Center for Economic Analysis, ITALY

Mark Bergen

Department of Marketing, Carlson School of Management University of Minnesota

Minneapolis, MN 55455, USA

August 16, 2019

Keywords: Retailing; Pricing; EDLP; HI-LO; Dynamic Capability; Menu Costs; Price Adjustment; Price Elasticity; Price Discovery

JEL Codes: M31, E31, D22, D40, C93, L10, O33, L81

* This work has been possible thanks to grants from SSHRC Canada, Canadian Foundation for Innovation (CFI) and Ontario Research Fund – Research Infrastructure. We owe a debt of gratitude to our industry collaborators for their generous and patient help. We thank Kulothungan Jeganathan and Naeem Ahmed for excellent research assistance. We also thank numerous seminar and conference participants for their comments. We also thank Indian School of Business (ISB), Hyderabad, India, where Sourav Ray was a visiting ISB-CLMP Research Fellow in 2018 while completing a part of this research. All errors are ours.

Pricing Better

Abstract

Electronic shelf label (ESL) is an emerging price display technology around the world. While

these new technologies require non-trivial investments by the retailer, they also promise

significant operational efficiencies in the form of savings in material, labor and managerial costs.

The presumed benefits of ESL, for example, tend to be focused around lower price adjustment

costs (PAC), also known as menu costs. However, ESL not only can save PAC but may also

enable the retailer to price “better,” generating greater value for the transacting parties. Thus,

ESL’s strategic impact for retailers occurs between claiming these presumed efficiencies and

realizing the value generating potential. Using transactions data from a longitudinal field

experiment, we assess such impact of ESL by studying how it shapes retail pricing practices and

outcomes. Our general finding is that ESL plays an enabling role to the retailer’s strategy –

thereby enhancing the retailer’s sales and revenues. The price adjustment efficiencies of ESL

allows retailers to do better waste management, price discovery, as well as leveraging value in

information for consumers. However, ESL’s impact on prices is nuanced, based on the retail

strategy (EDLP, HI-LO) being used. Papers quantifying emerging technologies’ impact on retail

outcomes are sparse, even fewer investigating their role in pricing. To the best of our

knowledge, ours is the first study to explore and quantify how ESL interacts with retail strategy

to affect retail pricing practices and retail outcomes.

Keywords: Retailing; Pricing; EDLP; HI-LO; Dynamic Capability; Menu Costs; Price Adjustment; Price Elasticity; Price Discovery

1. INTRODUCTION

Electronic shelf labels (ESL) are part of an expanding array of retail technologies that include

the likes of self-checkout kiosks, smart carts and a number of RFID beacon and other near field

communication (NFC) applications. Despite the significant investments required, these

technologies are of interest to retailers because they promise significant operational efficiencies.

For example, self-checkout kiosks and smart carts save managerial time and labor costs at check

out, while the several beacon and NFC applications promise savings in information gathering

and communication costs by facilitating customer monitoring and customized prices and

promotions. Similarly, the presumed benefits of ESL tend to focus around lower price

adjustment costs (PAC). However, the impact of these new technologies may go beyond cost

savings. The self-checkouts and personalized promotions may enhance customer shopping

experiences, while ESL may also enable the retailer to price “better,” generating greater value for

the transactions. Competitive advantage for the retailers is derived between claiming these

efficiencies and realizing the value-add potential of such technologies with appropriate

strategies. Unfortunately, papers quantifying emerging technologies’ impact on retail outcomes

are rare, even fewer investigating their role in pricing. In particular, it is hard to find similar

studies for ESL. Thus, our research questions are: How does ESL affect retail pricing and

outcomes like sales volume, and revenue; and how do retailers deploy ESL to support their

strategy?

Note that while the basic technology has been around since the 1990s, the adoption of ESL in

retail has been fragmented at best – greater popularity in Europe and Japan, and a much smaller

installed base but increasing contemporary interest in China, Canada, Israel, USA etc. Recent

engineering advances in the display technologies (e.g. electronic paper) have given it prominence

within the expanding ecosystem of new retail technologies with falling label prices and vigorous

marketing efforts driving industry adoptions. Industry research pegs potential annual growth of

ESL markets to be over 15% globally, with an even higher rate of growth in the American

market (Research and Markets, 2017a,b). At this rate of growth, the global installed base will

almost double within the next five to six years. Surprisingly, few papers directly assess the

possible impact of ESL on retail pricing and outcomes. For example, several papers allude to the

potential of ESL to impact retail prices and pricing practices, either directly or by enabling

Ray et al. 2006; Bergen, et al. 2008; Gedenk et al. 2010; Grewal et al. 2011; Bolton and Shankar

2018). Yet, none directly estimate such impacts. To the best of our knowledge, Garaus et al.

(2016) is the only published paper that assess the direct impact of ESL. However, their focus is

on consumer perceptions of ESL, not ESL’s impact on retail pricing and outcomes.

This lack of attention is quite surprising as it creates a serious gap in our understanding of

pricing technologies. Not only are ESL systems large strategic investments by the retailers, the

retail deployment of ESL with its lower price adjustment costs is presumed to have a direct

impact on the extent of price rigidity and flexibility, which play a central role in modern macro

and monetary economics literature. For example, the modern New Keynesian Dynamic

Stochastic General Equilibrium (New Keynesian DSGE) model, the workhorse model used for

monetary policy analysis, critically depends on the response of prices to monetary policy shocks,

which in turn, depends on the extent of price rigidity. Many monetary economy models need a

high degree of price rigidity to match aggregate data patterns. Among the existing theories of

price rigidity, perhaps the best known and the most popular is the price adjustment cost (PAC),

also called the “menu cost” theory (Barro 1972, Sheshinski and Weiss 1977, Mankiw 1985, Ball

and Mankiw 1994). According to this theory, prices are rigid and thus adjust sluggishly because

it is costly to change them. The natural conclusion is prices will be less rigid with ESL. Yet,

there is limited evidence supporting this outcome.

In recent years, an emerging literature in marketing has explored how the extent of variation

in micro-level price rigidity is an outcome of strategic decisions (Ray et al. 2006; 2012). These

suggest, the deployment of ESL may be only partially predictive of the extent to which prices are

rigid. Moreover, the menu cost models assume that the PACs are exogenously generated—either

fixed and independent of the size of price change (Mankiw 1985), or convex, where cost

increases with the size of price change (Rotemberg, 1982, 1987). In contrast, another developing

literature in business and economics, explicitly consider PACs as endogenous to organizational

factors such as strategic capabilities (Zbaracki et al. 2004; Hallberg 2017). To this end, ESL

technology, which require large expenses and significant organizational changes to realize its

benefits, can be seen as resources that build strategic capabilities, whose return on investments

would depend on its effectiveness in supporting a given retail strategy. Thus the same

technology may support very different retail pricing strategies associated with very different

In this paper, we contend that technologies like ESLs are strategic investments that enhance

the retailer’s strategic capabilities. These capabilities enable retailers to create and claim value

by effective deployment of their strategy and more effective prices. To understand the

mechanism of its impact, we investigate how ESL affects price sensitivity, price adjustments and

price discovery efforts of the retailer. Our empirical design is a pseudo field experiment

comprising transactions data from two supermarkets that implemented ESL. Our analyses use

standard econometric models including Differences-in-Difference (DID), etc.

Our general finding is that ESL plays an enabling role to the retailer’s strategy, offering

significant value-oriented benefits beyond cost efficiency. We find the impact on price

sensitivity, price adjustment patterns, and price discovery modes of the retailers are consistent

with these different roles of ESL. We also find that the nature and scale of ESL’s impact on

retail prices is contextual with greater price rigidity observed in some situations. These indicate

that the impact of ESL is highly nuanced. To the best of our knowledge, we are the first to

explore and quantify how a price display technology like ESL interacts with retail strategy to

affect retail pricing and its outcomes.

In the rest of the paper, we first discuss the ESL technology and the related literature in

section 2. We describe our data in section 3, in particular – the supermarket stores from which

we get our data, their respective positioning strategies and specific use cases for the ESL

implementation. In section 4, we describe the experimental set up identifying the treatment and

control groups. In section 5, we specify the empirical models estimating the impact of ESL on

retail outcomes, price sensitivity, price adjustment patterns and price discovery, and present the

results. A discussion of the results and their implications for research and practice is in section

6. Section 7 concludes by pointing out some limitations and future areas of study.

2. ELECTRONIC SHELF LABELS AND RELATED LITERATURE

Electronic Shelf Labels (ESL) are electronic label displays that, for the most part, replace

paper tags. Sometimes, also referred to as electronic price tags or as electronic point of purchase

(EPOP) displays, these labels are typically based on LCD or electronic paper (e-paper)

technologies. The labels are wirelessly connected to a central computer, typically in the back

office of the retailer. This allows the retailer to change the information displayed on the labels

displays are integrated with the point of sale (POS) systems used at store checkout.

Economies of Scale in Physical Price Adjustment Costs (Menu Costs)

One immediate and obvious benefit of ESL systems in a multi-product setting is their ability

to cut dramatically the physical price adjustment costs (menu costs) of the traditional paper-tag

based price system, to the point where the menu cost of adjusting one additional price is close to

zero, or perhaps even zero. Thus, ESL systems introduce economies of scale in price adjustment

technology, letting the retailer adjust the price of a given good more frequently while incurring a

fraction of the cost. These savings can be substantial in light of the existing empirical evidence.

For example, Levy et al (1997, 1998) and Dutta et al (1999) use time and motion

measurements data on paper-price tag based price adjustment processes, which were collected by

an ESL system manufacturer. The company collected these data in order to measure and validate

the cost savings that their system could generate. Using these data, Levy et al (1997, 1998)

report that the annual menu costs at large US supermarket chains average about $105,887 per

store (in 1991–1992 prices).1 In relative terms, the total estimated menu costs, which equal

$0.52 per price change on average, comprise 0.70 percent of revenues and 35.2 percent of net

margins, suggesting that the magnitude of the menu cost is substantial. Dutta et al (1999) report

comparable menu cost estimates for a large US drugstore chain. There are no comparable cost

estimates with ESL. However, it is safe to conclude conservatively, ESLs would save the bulk

of these physical price adjustment costs.

Managerial Price Adjustment Costs

Going beyond the physical menu costs, there is an emerging literature that calibrates the

managerial and customer costs of price adjustments. The ESL’s role in these other components

of the PACs is unclear. Zbaracki et al (2004) try to shed light on the magnitude of the

managerial cost of price adjustment. They conduct time and motion measurements of price

adjustment processes at a one-billion-dollar US industrial manufacturing company and its

customers. They find that the managerial costs of price adjustment are more than 6 times, and

the customer costs of price adjustment are more than 20 times the menu cost. In dollar terms,

1 In 2019 prices, this would be equivalent to $199,131. For large chains, these figures amount to significant sums of

they find the total annual cost of price adjustment in 1997 is $1,216,445.2 Of this amount, 3.57%

is the menu cost, 23.03% is the managerial cost which includes the cost of information gathering

and analysis, systems cost, and the cost of the managerial time spent on the evaluation and

decision of price changes, and 73.40% is the customer cost of price adjustment. So,

conservatively, even if the managerial and customer costs of ESL are similar to that of paper

labels, the potential for saving the physical menu costs are still significant.

However, there is reason to believe, ESLs introduce significant economies even in the

managerial costs of price adjustments. Much of these managerial costs derive from the time and

effort required by managers to decide on what prices to implement. Large price changes can be

especially onerous. ESL systems make small price changes profitable. For example, under the

existing manual, posted paper price tag based system, small price changes might not be

worthwhile because their fixed cost may exceed the benefits. The ESL systems, by reducing the

menu costs to zero (or close to zero), make such small price changes profitable. For example,

Levy et al. (1997) report that the supermarket chains in their sample, in an average week

experience cost increases on about 800–1,000 products they sell. However, the supermarkets

adjust prices of only about 70–80 percent of these products. The remaining 20–30 percent of the

prices are not adjusted immediately because the existing menu costs make the necessary price

adjustments unprofitable. ESL systems would make these smaller price changes profitable, and

thus the chain would leave less money on the table.3

Economies of Scope

ESL systems also have the ability to adjust many prices with a click of a button, suggesting

that these systems introduce economies of scope as well in the price adjustment technology, an

idea that was suggested by Lach and Tsiddon (1996, 2007), to explain the within-store

synchronization and cross-store staggering of price changes that they found in their data.4

Newer versions of the ESL technology come with enhanced graphics and display options that

allow the retailer to provide myriad information, including, but not limited to branding,

2 In 2019 prices, this is equivalent to $2,287,646.

3 Consistent with these empirical observations, in standard theoretical menu cost models that economists frequently

use, prices do not adjust to small shocks. In some models, the shocks need to be exceptionally large for prices to start adjusting. See, for example, Karadi and Reiff (2012).

4 Alvarez and Lippi (2014), Baudry et al (2007), Dhyne and Konieczny (2007), Levy et al (1997), Midrigan (2011),

competitor information, vendor promotions, quality and product attributes, price discount ending

date, etc. So, ESL systems enable the company managers to monitor and adjust not only the

prices, but also the quantities, the inventories, promotional information, competitive information,

vendor management, nutritional value information, etc. In other words, the economies of scope

that comes with ESL systems, covers wider range of business activities and resource use.

Price Discovery

An important advantage of an ESL system over the existing paper price tag based system that

is related to these managerial costs, is its ability to allow price experimentation. Price

experimentation and price discovery practices seem to be far more common than the literature

recognizes. There is evidence that the type of price adjustment practices sometimes retailers are

engaged in, can be best explained by a model in which there is an uncertainty about the demand

elasticity and/or about competitive factors. Under these circumstances, the firms are unable to

price optimally. To overcome these difficulties, it might be optimal for the firms to engage in

price experimentation, in order to discover the right price, by trial and error. Theoretically, the

optimality of these types of activities that involve price learning and discovery, has been

demonstrated by Rustichini and Wolinsky (1995), Balvers and Cosimano (1993), and Aghion et

al. (1991), among others.

On the empirical front, Argente and Yeh (2016) find that the prices of new products change

twice as often as the prices of the average product. In addition, they find that the average size of

these adjustments is at least 50 percent larger than the average price change. They show that a

menu cost model with price experimentation can rationalize these findings. Bachmann and

Moscarini (2011) present evidence that is consistent with a model of monopolistic competition in

which there is imperfect information about the demand, but the firm gradually learns and

discovers its price elasticity from the sales volume. Keil et al (2001) report that managers that

were assigned long-term goals were engaged in more price experimentation, in comparison to the

managers that were assigned short-term goals. Campbell and Eden (2014) also document

micro-level price behavior, which is consistent with a model that incorporates experimentation.

ESL makes it feasible to review and consider price adjustments of varying frequency as well

as of varying sizes by conducting small scale, within-store, pricing and price adjustment

the zone level, etc., at low cost. ESL systems can be linked to the companies’ inventory and

financial management software, and therefore learning, analyzing, and discovering the

bottom-line profitability scenarios and outcomes of such pricing experiments can be accomplished

quickly and efficiently, at relatively low cost.

This capability of the ESL systems is particularly beneficial because in the absence of

experimentation, a full optimization requires a complete knowledge of all the relevant

information, which would be prohibitively costly to gather and process. Experimentation of the

type we are discussing here is perhaps not the first best, but given its feasibility and its low cost,

it can be a very cost-effective in terms of the learning speed as well as effectiveness.

Price Coordination across Markets/Regions

Adams and Williams (2019) note that many large multi-store retailers do not always price on a

store-by-store or even on a market-by-market basis. Instead, they observe, prices are set on a

zone-by-zone basis, where each zone spans several markets that form a heterogeneous group.

DellaVigna and Gentzkow (2019) find that most US food, drugstore and mass merchandise

chains charge nearly uniform prices across stores despite wide variation in consumer

demographics and the level of competition. Based on price elasticity estimates, they conclude

that the average chain sacrifices 7 percent of profits relative to a benchmark of flexible prices.

This pricing practice may be due the chains’ to inability to efficiently manage heterogeneous

pricing profiles across large number of stores and/or markets. The ESL technology has the

potential to make geographically segmented pricing and price adjustment processes practically

and logistically more feasible as well as more cost efficient. The ability of the ESL to permit

small-sample experiments and price discovery exercises at low cost, will permit more optimal

pricing adapted to local settings.

Strategic Benefits and Consumer Value

There are other, less obvious advantages of ESL systems. The economies of scale in changing

prices can allow retailers manage waste more effectively, especially for perishable products.

They can change prices more frequently (e.g. several times a day or even by the hour, instead of

once a day or week), and can time and grade them to achieve higher sales yields and lesser

excess inventory at the end of the selling cycle.

implications. Ray et al. (2006) study a theoretical model, where a strategically minded

wholesaler with low enough menu costs, takes advantage of the menu cost that the retailer faces

to make frequent “small” price increases. The retailer is unable to pass-through these because of

the menu cost s/he faces. Such small price changes can also be key strategic imperatives for

retailers in consumer electronic markets as shown in Ray et al. (2012). Chen et al (2008) show

that frequent small price changes exist at the retail food markets as well.

The integration of the ESL systems with the same POS database that is connected to the

checkout counters minimizes chances of a mismatch between the shelf price and the checkout

price (over or under ring), leading to greater consumer confidence in prices. Bergen et al. (2008)

discuss the potential significance of such confidence for both retailers and policy making.

The savings in time and efforts of the in-store execution and management staff can be

channeled into providing more streamlined and effective service to improve customer

experience. These complement the sleek designs of ESL, which can improve the look and feel of

a store, creating a more positive image compared to stores with older technology (Garaus et al.

2016). Some argue that the standardized design of price displays may even mute the salience of

prices and enhance the utility of other non-price related attributes of the retailer (Soutjis, et al.

2017), thereby reducing the consumer’s price sensitivity.

ESL and Retail Strategic Positioning

Overall, the potential impacts of ESLs appear to come in essentially two different forms. The

first is efficiency in terms of cost savings – both physical menu costs as well as managerial price

adjustment costs. The second is the added value ESL creates for retailers and consumers. It

enables retailers to manage its price adjustments strategically, find better prices and in turn,

being able to offer greater value to its customers. Between realizing these efficiencies and

claiming the added value, retailers can generate better gross margins for themselves.

Nevertheless, the process by which these higher margins are to be generated completely

depends on the strategic focus of the retailer. For some retailers, frequent price changes are a

core part of their strategic positioning. Certainly, ESL would potentially result in cost savings

for such retailers. However, the potential for ESLs to support even greater flexibility in prices

may be less compelling for these retailers than supporting higher margins due to added value and

strategic positioning. Thus, both cost savings from frequent price changes as well as the

potential of ESLs to support flexible prices may be moot for such retailers. Yet, ESL systems

may enhance these retailers’ ability to find the right prices to support such consistency. A key

upshot of this line of thinking is to suggest that while ESL may reduce PAC, it may not

necessarily lead to less rigid prices, which would depend on retail strategy.

3. DATA

The data for our study comes from two different supermarket stores in the North-West Milan

region of Italy. We will call them stores S and M. Both belong to one of the largest grocery

store operators in the country, which has over 1,000 stores. Both stores are owned and operated

by individual store management. The parent company had worked collaboratively with a

consulting company specializing in POS technology, to install ESL in limited scale in the two

stores. ESL was installed in the Fresh Fruits and Vegetables departments of both stores as well

as in the Delicatessen department of store M. One of the objectives of the installation was to

assess the potential return on such investments, over an extended period of deployment.

Our data comprises of two types. First, we have records of sales-receipts generated at the

POS over a two-year period, spanning the date when ESL was installed. In particular, for store

S, we have 445,252 receipts for 105 weeks (July 16, 2007–July 16, 2009); with ESL installed in

the 60th week (September 16, 2008). For store M, we have 384,475 receipts for 106 weeks (July

3, 2007–July 23, 2009); with ESL installed in the 70th week (November 18, 2009). Second, we

received privileged access to some confidential internal reports and white papers of the company.

Our descriptive details are drawn from the information in the written reports, while the statistical

analyses are based on the POS sales records.

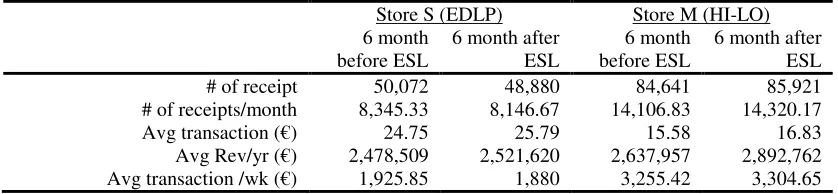

Store Size and Operations

The stores are largely similar to each other in many respects including size, gross profit

percentages and growth. Based on the sales data of 6 months before the ESL installation in

2008, we estimate the annual sales revenue of store S to be in the range of 2.5 million Euros, and

that of store M to be about 2.6 million Euros. The average purchase per receipt is higher for

store S at €24.75 than for store M at €15.58. However, store S has an average of about 1,900

consumer transactions per week, compared to about 3,200 for store M. Based on internal

respectively, and similar sales growth trajectories for comparable categories (3%).

However, we find that there are differences in expenses as a percentage of sales, 23.8% at

store S vs. 4.2% at store M. The staff at store S is mostly comprised of temporary and

inexperienced workers, while that of store M is comprised of more skilled, department managers.

This reflects in the average wage rate for store S (at £9/hr) being significantly less than that of

store M (£12/hr). That said, there are important distinctions between the stores when it comes to

their strategic retail positioning and their purported use of the ESL technology.

ESL for Store Pricing Practices – EDLP and HI-LO Positioning

From a description of their pricing processes, we know that store S prices are based on

warehouse price margins. Yet, pricing consistency is deemed very important and changes in cost

are not immediately reflected in prices, and there are only few promotions. This type of pricing

is generally associated with Every Day Low Price (EDLP) positioning. EDLP retailers aim to

provide value to consumers by maintaining a high level of price consistency and reducing

instances and salience of periodic price promotions.

In contrast, in store M, maintaining price consistency is less important with around 50% of

prices changing daily, only some of which may be due to cost changes. In fact, the store

manager can set its own selling price, and not necessarily as a margin on warehouse price. This

type of pricing is consistent with HI-LO positioning. HI-LO retailers aim to provide value to

consumers and draw traffic to the store by frequent price promotions over its product lines.

As a pricing technology that purports to give enhanced ability to the retailer at managing price

changes, ESL appears to have a direct role to play in implementing these retail strategies –

greater price consistency in EDLP and more effective price changes in HI-LO. A key focus in

the assessment of return on investment (ROI) was the ESL’s role in better implementation of the

retail strategies.

Figure 1 plots the average weekly prices for two random treatment group product for the two

stores. Note here store S has fewer price changes than store M in a similar time period – as

would be expected from the description above. Visually it is difficult to discern any specific

change in pattern between pre- and post-ESL installation weeks.

ESL for Waste Management

significantly. Acting proactively to clear unsold inventory of perishables was a major concern

for store S. Typically, the department manager would reduce prices at the end of the day to sell

off unsold produce. This came with several challenges. First, the manual task of managing price

reductions across a number of products is non-trivial. Second, discounts could be too deep,

leaving money on the table, or too shallow, resulting in unsold produce.

ESL could enable the managers to run more efficient “on special” promotions as opposed to

engaging in a fire sale of unsold inventory. ESL could also help price better, resulting in less

“extra” inventory towards the end of the day, as well as discounting just enough, and no more, to

get the desired sales lift. In contrast, waste management was not a big managerial concern for

store M. In the perishable Fruits and Vegetables department a waste of 5%–7% was considered

acceptable. In the Delicatessen department where products are normally cut to order, wastage

was negligible.

ESL for Consumer Information

Consumer information was also a focus of the ROI from ESL. Strict Italian fresh food

labeling laws require detailed and accurate provenance information be displayed at point of

purchase, with heavy fines imposed on retailers for noncompliance. So both stores were keen to

avoid such fines. ESL could reduce the costs of compliance by making the process of providing

such information more efficient when products were repriced, re-shelved, and during inventory

changeovers. However, ESL would allow the stores to easily provide additional information not

mandated by law, such as competitor pricing information or additional non-price attributes. This

is where the stores differed. While store S focused on compliance, store M aimed at going

beyond and provide additional information such as region of origin, flavor, etc. across its product

lines. This would presumably give greater value to its customers, resulting in a sales lift and

contributing further to the ROI.

ESL and Managerial Supervision

Last but not the least, was the concern with managerial time-savings. Recent legal changes in

Italy required stores to provide additional data for livestock such as where the animal was raised,

where slaughtered and where butchered, along with license numbers for the slaughterer and

butcher. The item purchased must contain this data for full traceability. The volume and

applied to beef, the externalities of such regulatory attention meant there was a heightened

sensitivity for managerial supervision and monitoring of staff compliance across the store. ESL

was expected to introduce more economies of scale for both stores by centralizing such efforts.

In summary, the key differences in the use of ESL across the stores were in the

implementation of strategic price positioning – EDLP for store S, HI-LO for store M; greater

emphasis on efficient waste management for store S; and greater emphases on value through

consumer information for store M.

4. EXPERIMENTAL DESIGN AND MEASUREMENT ISSUES

Recall that ESL was installed in the fresh fruits and vegetables (F&V) department in store S

and in both F&V and Delicatessen departments in store M. Given the before-the

ESL-installation and after-the-ESL-ESL-installation data, we have a pseudo experimental setup to study the

impact of ESL on retail outcomes (price, sales volume and revenue) in these departments. For

purposes of comparability, we only analyse the F&V department. In experimental design terms,

this would be considered the treatment group. However, a simple before- and after-comparison

would not be able to isolate the impact of ESL since several unobserved variables that vary over

time might confound the results. Therefore, for identification purposes, i.e. to isolate the effect

of ESL, we need to choose an appropriate department as a control group.

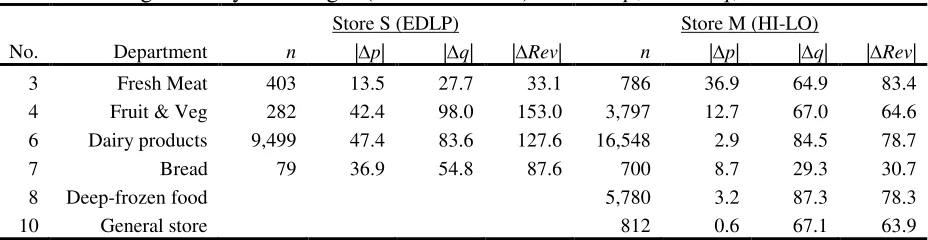

Choice of Control Group

Ideally, this control department would be similar to the treatment department such that it

would be affected by all the potential unobserved variables, except that it will not be affected by

ESL. Since there are several departments other than F&V in the stores, where ESL was not

installed, all of them are potential candidates as control departments. We select a specific

control in the following three steps:

(1) Select candidate daily purchase categories, preferably food related. At this stage, we

selected the following five departments: Fresh Meat, Dairy Products, Bread, Deep-Frozen Food,

General Store.

(2) From the above we then select a subset with similar average price, volume and revenue

changes over time. This resulted in the following three departments: Fresh Meat, Bread, General

Store. We then dropped General Store and Bread, for we did not have enough observations in

(3) Lastly, we checked if Fresh Meat exhibits similar time trends before and after ESL. A

similar trend offers additional assurance that Fresh Meat is independent of ESL and thus a good

control. For this we ran the following regression:

(

)

(

)

2 2

1 2 3 4 5

t t t t

y = α + βt + β t + β ESL × t + β ESL × t + β ESL + ε (1)

where yt is the dependent variable (price, sales volume, or revenue of Fresh Meat) in week t,

t

ESL is a binary variable which equals 1 if t is after implementation of the ESL and 0, if before,

and

ε

t is the error term. A significantβ

3 orβ

4 coefficient would suggest that the trend differsbetween before and after ESL. We run this analyses for both stores and find strong evidence that

there is no such ESL dependency – five out of the six regressions return insignificant

coefficients. Thus we conclude that Fresh Meat is an appropriate control department for our

identification purposes.5

Data Aggregation and Descriptive Statistics

Recall that our data is at a highly disaggregate, individual purchase incident level. This

allows us to track individual products over time. To ensure relative balance we use 53 weeks’

data before ESL installation, for both stores. We then use most of the available weeks in the post

installation period – 42 weeks for store S (EDLP) and 33 weeks for store M (HI-LO). We drop

four weeks (2 weeks before and 2 weeks after) around the installation date to filter out any

disruption due to installation.

Each product in our data is identified by a 13 digit EAN (European Article Number) code and

is classified as belonging to one of 25 “departments” which are the broad store categories like

F&V (our treatment category), Fresh Meat (our control category), etc. For store S (EDLP), the

before-ESL and after-ESL number of products in the sample were (26, 26) for the treatment

group and (17, 11) for the control group. Correspondingly, for store M (HI-LO) the before-ESL

and after-ESL number of products in the sample were (335, 273) for the treatment group and (61,

87) for the control group. To adjust for the unbalanced nature of the sample between the

treatment and the control groups, we use robust estimates in our analyses.

We aggregate the data for each EAN code in the two departments at a weekly level.

Computing the average weekly unit price is not straightforward. We first calculate the unit

prices for each receipt in a given day from the recorded gross price divided by the units. We

then compute the median of such unit prices as our daily central tendency measure. For the

weekly unit price, we take the average of the daily medians. We impute missing unit prices with

previous period price only if the number of continuous missing weeks is less than or equal to 2.

We had to exclude approximately 36% of the original data – mostly products sold by weight, for

which we did not have enough information to calculate the unit price.

After accounting for missing data (e.g., not all products are purchased every week) and the

aggregations, the total number of observations we have for store S (EDLP) are 422 before-ESL,

and 302 after-ESL, for the treatment (F&V) category. The corresponding numbers are 422 and

389 for the control (Fresh Meat) category. For store M, the number of observations are 9,097

and 4,543 for the treatment category, and 1,636 and 1,402 for the control category, respectively.

See Table 1.

In Table 2, we report some descriptive statistics pertaining to price, volume sales and revenue

in our sample. The average prices in store S increase (e.g. from 1.59 to 2.58 for treatment

group), while that of store M remain similar (e.g. 1.73 to 1.69). The average sales volume for

store S decreases (12.88 to 9.36) while that of store M remains similar (22.96 vs. 23.13).

Revenue in both cases remain similar (19.61 vs. 18.83, and 36.90 vs. 35.30 – in ×100 Euros – for

store S and store M, respectively).

While we restrict our analyses to F&V and Fresh Meat departments, we also looked at the

store-wide sales figures by comparing the number of transactions and average value of the

receipt level transactions six months before and after the ESL installation. The average

transactions of the store are marginally better in the post-ESL period (25.79 vs. 24.75, and 16.83

vs. 15.58, for store S and store M respectively). However, there is some drop in the average

number of transactions per week for store S (1,925 to 1,880), and a small increase for store M

(3,255 to 3,304). See Table 3. However, not much can be inferred from these descriptive

numbers in terms of the impact of ESL on the retail outcomes. For that we now turn to the

econometric analyses.

5. EMPIRICAL MODEL ESTIMATIONS AND RESULTS

Our primary empirical objective is to investigate how the ESL technology can enable and

outcomes, viz. prices, volume and revenue, as well as the process by which such an impact

operates.

We start by assessing the impact of ESL on price, volume and revenue and how these differ

for the different stores, and discuss the robustness checks we conduct. Then, to get insights into

the processes that operate for different retail strategies, we estimate ESL’s impact on price

sensitivity for the different stores, along with several robustness checks of our results. The next

analysis investigates ESL’s impact on price adjustment patterns of the different stores as further

investigation into the determining processes. The last analysis explores whether ESL impacts the

price discovery efforts of a retailer.

Impact of ESL on Price, Sales Volume and Gross Revenue – Difference-in-Difference

To estimate the impact of ESL we use the Difference-in-Difference (DID) model. DID is a

quasi-experimental method used to measure the effect of a treatment or intervention over time. It

allows for comparisons over time for a non-random sample by comparing the treatment group

before and after an intervention, with a suitably matched control group that does not receive the

intervention.

DID with Pooled Data

We first pool the data from both stores to run the following basic model:

ln (𝑦𝑦𝑗𝑗𝑗𝑗𝑗𝑗) =𝛼𝛼+𝛾𝛾(𝑇𝑇𝑇𝑇) +𝛽𝛽(𝐸𝐸𝐸𝐸𝐸𝐸) +𝛿𝛿(𝑇𝑇𝑇𝑇×𝐸𝐸𝐸𝐸𝐸𝐸) +𝜇𝜇𝑗𝑗+𝜗𝜗𝑗𝑗 +𝜏𝜏𝑗𝑗+𝜀𝜀𝑗𝑗𝑗𝑗𝑗𝑗 (2) where, yjit refers to the dependent variable of interest (price, sales volume, revenue) – for store

j, product (SKU/EAN) i, and week t. TD is a dummy variable, which equals 1 if product i

belongs to the treatment department, and 0 otherwise; ESL is a dummy variable, which equals 1

if week t is after the ESL intervention, and 0 otherwise; µj is a fixed effect for store,

ϑ

i is afixed effect for products, and

τ

t is a fixed effect for week. εjit is the error term. We use robuststandard error estimates to deal with potential heteroscedasticity of the error terms.

There are two reasons why we use the natural log transformation. First, our data is highly

skewed with large variance. Using the natural log transformation flattens the spread and reduces

the impact of the outliers.6 Second, using ln( ) jit

y makes the interpretation of the coefficient δ

particularly convenient; it is the post-ESL change of the treatment group response as a

percentage of the control group.

The results of the pooled DID is reported in Table 4(a). We find that following ESL

installation, there is a marginally significant decrease in unit price of the treatment group relative

to the control group (δ = –0.021; p = 0.056). On the other hand, sales volume and gross revenue

shows a significant increase by 9.8% (δ = 0.098; p = 0.002) and 7.3% (δ = 0.073; p = 0.023),

respectively.

DID by Store

We next run the same DID analyses separately for the two stores to check if ESL has different

impact on the two stores. For this we run the following model, separately for each store:

ln (𝑦𝑦𝑗𝑗𝑗𝑗) =𝛼𝛼+𝛾𝛾(𝑇𝑇𝑇𝑇) +𝛽𝛽(𝐸𝐸𝐸𝐸𝐸𝐸) +𝛿𝛿(𝑇𝑇𝑇𝑇×𝐸𝐸𝐸𝐸𝐸𝐸) +𝜗𝜗𝑗𝑗+𝜏𝜏𝑗𝑗+𝜀𝜀𝑗𝑗𝑗𝑗 (3) Since we run the analyses separately for each store, this model is identical with the earlier model

except that we do not have the subscript j and the store fixed effect µj. Table 4, panels (b) and

(c) report the estimation results.

The results show that for store S (EDLP), post-ESL treatment group responses are

significantly higher than pre-ESL levels: unit price is higher by 13% (δ = 0.131; p = 0.001),

sales volume is higher by 17% (δ = 0.174; p = 0.003), and gross revenue is higher by 31% (δ =

0.308; p = 0.000), compared to the control group. These numbers are substantial and are all

statistically significant at the 1% level. For store M (HI-LO), the results are more of a mixed

bag. While there is no statistically significant change in unit price levels (δ = –0.018, p = 0.132),

sales volume exhibits an increase of 8% (δ = 0.082, p = 0.017) relative to the control group.

Gross revenue also exhibits an increase of about 6% (δ = 0.058; p = 0.091), though only

significant at the 10% level.7

Robustness Check – Placebo Interventions

To rule out the possibility that the estimation results are an artifact of the DID method, we

conducted the placebo test. For this we separated the pre-ESL and post-ESL data and introduced

arbitrary intervention points in each. We then proceeded to conduct the DID estimation for each

of these arbitrary specifications. A significant δ coefficient will reject the null hypothesis that

there is no placebo effect.

Recall that for store S, the actual ESL installation was on the 63rd week. For the placebo test

in the pre-ESL sample, we introduced weeks 23, 33 and 43 as intervention points. Similarly, for

the post-ESL sample, we specified weeks 73 and 83. For store M, where the original ESL

installation was done on week 70, we specified weeks 30, 40 and 50 for the pre-ESL sample; and

weeks 80 and 90 for the post-ESL sample. So, we are able to do 2 (store) × 3 (response

variables) × 5 (intervention points), i.e. 30 comparisons. A large majority (26 out of 30) of the

coefficients are not significant statistically, suggesting that our estimation results are not an

artifact of the DID specification.8

Impact of ESL on Price Sensitivity

We next focus on assessing how ESL affects price sensitivity of the treatment group. There

are several reasons to believe ESL will have an effect on consumers’ response to retail prices. In

principle, to the extent retailers are able to discover “better” prices, they are able to generate

greater response from the consumer. Smaller price reductions, for example, might result in the

same demand lift as higher reductions were getting earlier. This will reflect in the data as higher

price sensitivity. On the other hand, to the extent retailers are able to offer diagnostic

information that is valuable to the consumer, through the use of ESL, they may succeed in

moving the consumer focus away from a price-centric purchase decision to a more value-centric

one. This could reflect in the data as lesser price sensitivity. In addition, ESLs could also free

up staff time from managing and supervising pricing processes to customer service, further

contributing to perceptions of value (Levy et al 2010). As well, ESLs might also contribute to a

cleaner and more sophisticated look and feel of the store, enhancing the shopping experience and

also contributing to the perceptions of value.

To estimate price sensitivity, we use the standard Autoregressive Distributed Lag (ADL)

models. Our basic specification is an ADL(1,1) model, as follows:

𝑙𝑙𝑙𝑙(𝑞𝑞𝑗𝑗𝑗𝑗) =α + 𝛽𝛽1𝑙𝑙𝑙𝑙�𝑞𝑞𝑗𝑗,𝑗𝑗−1�+β2𝑙𝑙𝑙𝑙(𝑝𝑝𝑗𝑗𝑗𝑗) +β3𝑙𝑙𝑙𝑙�𝑝𝑝𝑗𝑗,𝑗𝑗−1�+𝛾𝛾1𝑙𝑙𝑙𝑙(𝑝𝑝𝑗𝑗𝑗𝑗)∗ 𝐸𝐸𝐸𝐸𝐸𝐸

+𝛾𝛾2𝑙𝑙𝑙𝑙�𝑝𝑝𝑗𝑗,𝑗𝑗−1� ∗ 𝐸𝐸𝐸𝐸𝐸𝐸+𝛾𝛾3𝐸𝐸𝐸𝐸𝐸𝐸+𝜗𝜗𝑗𝑗+𝜀𝜀𝑗𝑗𝑗𝑗 (4) where, qit and pit are respectively, the quantity sold and unit price of product i in week t; ESL is

a dummy variable which equals 1 if t is after ESL installation, and 0 if before;

ϑ

i is productfixed effect and

ε

it is the error term. Using the natural log-log specifications have the twinadvantage of muting the impact of outliers as well as offering a convenient interpretation of the

regression parameters. In particular, price elasticity can be calculated from the estimated

coefficients, as:

Price Elasticity = + ×

β γ

2 1 ESL (5)Endogeneity and Instrumental Variables

One of the challenges of the earlier specification is the potential endogeneity between pit and

it

q . Not only does price affect the quantity demanded but quantity might also affect the prices

set by the retailer, making price potentially correlated with the error term. It might be

worthwhile to mention here that since our data comes from a single retailer who has price setting

power, the endogeneity problem might not be as severe as in more aggregate data sets with

multiple, possibly multi-store retailers, who set prices for multiple stores and multiple products.

In our case, it is more likely that the retailer only has control over prices that he uses to get a

response in terms of quantity demanded. Nevertheless, we address the potential endogeneity

with a standard two-stage-least-squares approach using instrumental variables.

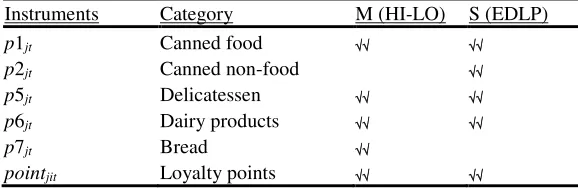

The desired characteristic of good instruments is that they will be correlated with the

endogenous variable, in our case pit, but uncorrelated with the dependent variable, in our case

it

q . We consider two broad types of instruments. First, we take the average prices of available

“other” categories as instruments. Specifically, we consider the average prices of the following

categories: Canned food, Canned non-food (only for Store S), Delicatessen, and Dairy and Bread

(only for Store M). The average retail prices are a big part of a retailer’s price positioning; for

example, they distinguish between high-price versus low-price retailers. Therefore, these “other”

category prices are expected to be correlated with price levels of the treatment group; but are

otherwise not expected to be correlated with the treatment group quantity sold. Second, we take

advantage of the data on the store’s loyalty program, to construct the following instrument:

a particular receipt r that included purchase of product i. Pointsjit is the sum of all loyalty points

in receipts including the purchase of product i in a particular week t. Pointsjit is constructed

such that it satisfies two key characteristics. First, more frequently purchased products get

assigned more Pointsjit compared to those that are not. This is by construction. Since more

frequently purchased products are likely to be priced differently than products not purchased as

frequently, Pointsjit would be correlated with pjit. Second, Pointsjit is related to the total

monetary value of the purchase and not the quantity of individual product purchases. Hence,

purchase quantity of the product qjit, is uncorrelated with Pointsjit. Thus, Pointsjit appears to

be a good instrument for pjit. We run the analyses separately for the two stores. The estimation

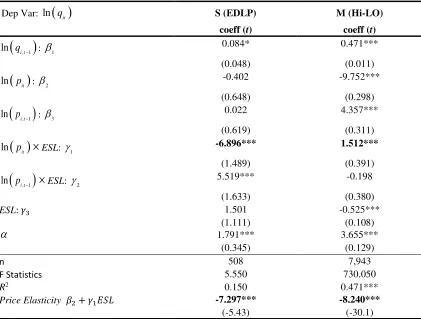

results are reported in Table 5.

Note the distinct nature of the coefficients.

β

2 is not significant for store S (EDLP) whereasit is for store M (HI-LO) (

β

2= –9.752). This is consistent with the different strategic positioningof the stores since the EDLP stores do not change much prices, while the HI-LO stores depend

on periodic promotions to draw traffic. The coefficient

γ

1 is statistically significant andnegative for store S (–6.896) suggesting that the demand is more price sensitive post-ESL. On

the other hand,

γ

1 is statistically significant and positive for store M (1.512) suggesting demandis less price sensitive post-ESL. Calculating the pre-ESL and post-ESL price elasticity for the

two stores, we get the price elasticity (in absolute value) of store S (EDLP) increases from –

0.402 (not statistically significant) to –7.297 (statistically significant); while that of store M

(HI-LO) decreases from –9.752 to –8.240 (statistically significant).

Robustness Checks for Price Sensitivity Patterns – Alternate First Difference Specifications

To check that the price sensitivity patterns evident in the estimated elasticities above are

robust, we ran the following alternate first difference specification.

( )

1( )

2 1( )

ln qit lnα β pit β ESL γ ln pit ESL ϑ εi it

∆ = + ∆ + + ∆ × + + (7)

We use the first differenced values of the same variables used earlier, as instruments for

( )

ln pit

∆ . The results are reported in Table 6.

sensitivity post-ESL. For store S (EDLP),

γ

1 is –2.061 (p < 0.01) suggesting price sensitivityincreases in the post-ESL period. On the other hand, for store M (HI-LO),

γ

1 is 1.830 (p < 0.01)suggesting price sensitivity decreases in the post-ESL period. Note that this pattern is exactly

the same as in the ADL(1,1) specification.

Impact of ESL on Price Adjustments

We turn our focus next on investigating the price adjustment patterns of the stores in the pre-

and post-ESL periods. Specifically, we estimate the average percentage price changes,

separately for price increases and decreases, as follows:

(

, 1)

, 1% /

% % 0

% % 0

it it i t i t

it it it

it it it

p p p p

p p if p

p p if p

− −

+

−

∆ = −

∆ = ∆ ∆ > ∆ = ∆ < ∆ (8)

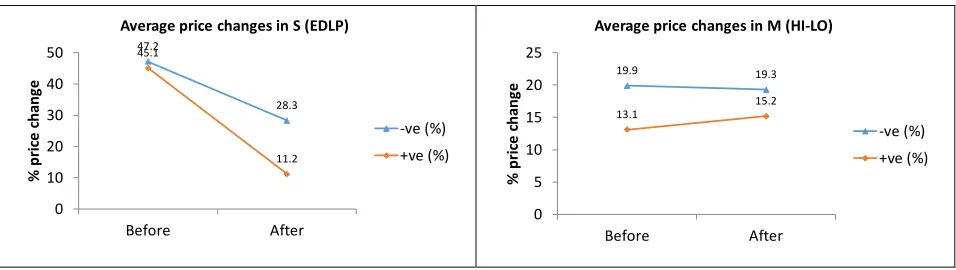

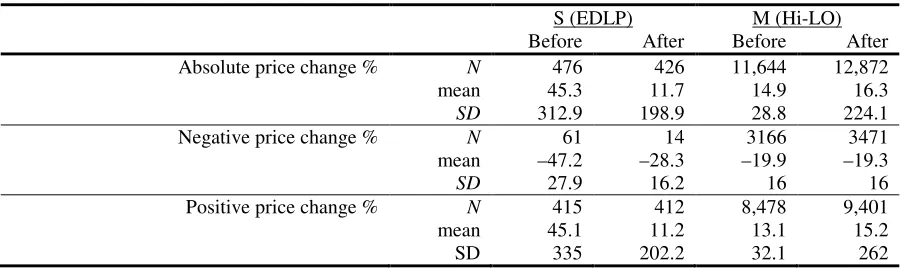

The estimation results are given in Table 7. For store S (EDLP), the average price reductions

decrease from 47.2% before ESL to 28.3% after ESL. At the same time, the average price

increases also decrease from 45.1% before ESL to 11.2% after ESL. So, there seems to be

overall, lesser magnitude of price changes after ESL. Indeed the average magnitude of price

changes decrease from 45.3% before ESL to 11.7% after ESL. In contrast, for store M (HI-LO),

the average price reductions are almost unchanged between 19.9% before ESL to 19.3% after

ESL. However, average price increases marginally increase from 13.1% to 15.2%. Overall, the

magnitude of average price changes go up from 14.9% to 16.3%, a modest increase. We

summarize the price changes in Figure 2.

Impact of ESL on Price Discovery

One of the key presumed advantages of ESL is that it gives the retailer the ability to change

prices more readily than it can with paper labels. A corollary of this is that retailer may be better

positioned to set prices based on more current information. As the business environment

changes, the retailer faces the challenge of not only interpreting and analyzing such changes to

decide whether and how those should impact its prices, but also implement changes should that

be needed. The retailer’s analyses of current information can happen in multiple ways. While it

can use existing models, routines and heuristics to map the information to its pricing choices, it

product mix combine in a given situation to affect its revenue outcomes. The combination of

these efforts and a consideration of any of several possible objectives such as maximizing

revenue, traffic, market shares, gross margins etc., inform the retailer’s decisions on what prices

to choose. We call this exercise “price discovery” by the retailer.

In the absence of direct observation and access to retail decision makers, it is difficult to

impute these activities from POS data. However, one of the implications of ESL is that, not only

can the retailer implement price changes easily, but knowing that, the retailer is also more likely

to engage in more frequent and current price discovery. This would then reflect in the post-ESL

prices incorporating more contemporaneous information than the pre-ESL prices. To explore

this possibility, we use a general autoregressive model specification on unit prices and estimate

the maximum duration of lagged impact for model fit. ESL driven price discovery would

suggest that the duration of such lagged impact would be shorter in the post ESL sample since it

would have used more current information.

( )

, ,(

,)

, 1ln ln

r

i t i k i t k i t

k

p α β p − ε

=

= +

∑

+ (9)For each product, we estimate the maximum lag r as being the higher of the two criteria: AIC

(Akaike’s Information Criterion) and SBIC (Schwarz‘s Bayesian Information Criterion). We are

able to do this analysis only for store M (HI-LO) since store S (EDLP) did not have sufficient

price changes to estimate the parameters. We find that the average lag after ESL (2.13 weeks) is

significantly smaller than the average lag before ESL (3.21). This is consistent with more

efficient price discovery discussed here.9

Summary of Results

Our results span two levels of comparisons – first between pre-ESL and post-ESL outcomes,

which is the direct impact of ESL; the second is between the two stores through the lens of retail

strategy (EDLP and HI-LO). Our estimations comprise prices, quantity sold, gross revenues,

price sensitivity, price adjustments and price discovery.

We find that the impact of ESL on average price levels is not to decrease prices. Rather, we

find an increase of 13% for store S (EDLP) and no significant change for store M (HI-LO). On

the other hand, ESL results in an increase of quantity sold and gross revenue for both stores – for

store S (EDLP) by 17% and 31%, and for store M (HI-LO) by 8% and 6%, respectively. In

absolute numbers, these are very significant levels of impact on sales volume and revenues –

without lowering prices. So, this must be due to something more than just cost efficiencies.}

For price sensitivity, we find the impact of ESL is quite different for the two stores. While

ESL makes demand more price sensitive for store S (EDLP) it makes demand less price sensitive

for store M (HI-LO). Similarly, there are differences between pre- and post-ESL price

adjustments between the two stores. For store S (EDLP), ESL appears to dampen large price

changes – the magnitude of average price reductions decrease from 47.2% to 28.3%, while

average price increases reduce from 45.1% to 11.2%. For store M (HI-LO), on the other hand,

ESL does not appear to affect average price reductions with no change between the pre- and

post-ESL price reduction magnitudes. However, there is a small amplification of price increases

from 13.1% to 15.2%.

The findings related to price level, sensitivity and price changes are significant. Recall that

one of the applications of ESL for store S (EDLP) was to better manage wastage of perishables.

Traditionally end of the day deep discounts (“fire sale”) were used to clear the inventory. It

appears that the ESL allows the retailer to use smaller price reductions to achieve such inventory

clearance, as reflected in the higher average price levels and price sensitivity post-ESL. The

smaller price reductions should directly contribute to the retailer’s bottom line.

In contrast, recall that one of the applications of ESL for store M (HI-LO) was to offer greater

value to its customers through the provision of relevant information. It appears that the store is

able to do that – its customers are less price sensitive in the post-ESL period, which would be

expected if price is no more the key criterion for purchase decisions. If customers were to give

more relative weight to the information and the other non-price related sources of value offered

by ESL in making purchase decisions, it lessens the price pressure faced by the retailer.

Consistent with this, it also appears that the retailer is able to sustain higher price increases,

albeit by smaller amounts than the EDLP store, and albeit the aggregate price increase is not

statistically significant.

With respect to price discovery, we cannot compare the two stores since we are only able to

estimate it for store M (HI-LO). We estimate a significantly lesser lag in the extent to which its

prices depend on past prices – 2.13 weeks for the post-ESL prices compared to 3.21 weeks for its

efficiencies of discovery, experimentation and learning, thereby responding to more cognate

relevant information in their price optimization efforts. Indeed, store M (HI-LO) seems to use

information that is more current, in setting its prices, in the post-ESL period.

In essence, ESL seems to allow the EDLP store achieve better pricing consistency by

dampening its price changes. On the other hand, ESL seems to allow the HI-LO store to

emphasize the non-price value and shift the consumer from narrowly focussing on price. Both

these outcomes seem to match the strategic imperatives of the respective stores.

6. DISCUSSION

Substantively, our main effort here is to understand how an emerging retail technology, ESL,

affects retail outcomes. Our data comes from a field implementation of the ESL technology,

covering almost two years around the installation date. The “field” aspect of the design brings

with it some benefits of external validity. Further, given our experimental design with distinct

treatment and control groups, as well as the longitudinal Difference-in-Difference (DID) model

used in the analyses, we are able to draw “causal” inferences with greater certainty.

Much of the causal inferences we are able to draw point to one primary conclusion – ESL can

be used to engage in better pricing practices, which in turn drives better retail outcomes. In

concluding this, we implicitly characterize “better pricing” as being intimately tied to retail

strategy, such that, it is the better fit between strategy and implementation of pricing that makes

the pricing better, and which drives retail outcomes like superior sales and revenue. Thus,

“better outcomes” are not pre-ordained as immutable characteristics of ESL systems. Rather, the

key issue seems to be whether characteristics of ESL allow retailers to better implement their

pricing tactics to support their idiosyncratic retail strategy. Thus, ESL has shades of a strategic

capability for retailers. At the same time, ESL’s promise to reduce menu costs and its attendant

implication for price rigidity has a direct bearing on how we interpret the technology and its

impact from a policy perspective. We frame our subsequent discussions through these twin

lenses – strategy and policy.

ESL as a Dynamic Capability: Best Practices Strategy Enabler

ESL systems are big-ticket expenses by the retailer – of the order of a couple of hundred

thousand dollars for one supermarket store – representing a significant investment for a

ROI from such strategic investments. On this, our results appear to bring good news for retail

managers, that ESL can significantly enhance retail sales volumes and revenue, two key

traditional measures of retail performance. There seem to be at least four related ways these

advantages of ESL accrue: reduction in menu costs, greater efficiency in waste management,

providing greater value to consumers and better price discovery. However, the key takeaway

from our results is that ESL acts as an enabling technology for the retailers – facilitating the

implementation of their idiosyncratic store positioning strategies to create and claim value.

For the EDLP store, the key impact of ESL is felt in its ability to dampen the end of the day

“fire sale” nature of price cuts necessitated by unsold inventory of perishable produce. With an

ability to readily adjust prices and find the “sweet spot”, the EDLP store is able to achieve a

lower level of aggregate price cuts (and hence a smaller range to which price goes back up after

the promotion) to clear the same level of inventory as before the implementation of ESL. This

reflects in the higher aggregate price sensitivity of demand in the post-ESL period.

For the HI-LO store, the key impact of ESL appears to be in its ability to offer greater value to

its customers in the form of better product related information. In this, the store effectively

reduces the centrality of price in the consumer decisions, which reflects in the lower aggregate

price sensitivity of demand achieved in the post-ESL period. For the store, finding this sweet

spot between value and price point is an onerous task. To this end, we find evidence that the

store engages in more price optimization and discovery in the post-ESL period.

The idea that ESL enables retailers effectively integrate their pricing, inventory and marketing

resources to better implement their positioning strategies indicate ESL enhances the competitive

advantages for the retailer, and as such, it has the dimensions of a strategic capability. In

particular, given that ESL allows the retailer to make quick adjustments in response to changes in

its business environment, be it competition, demand or supply conditions, it is a dynamic

capability as envisaged by Eisenhardt and Martin (2000).

Eisenhardt and Martin’s (2000) view of dynamic capability sought to demarcate boundaries

between “best practices” and dynamic capabilities that impart competitive advantage, sustainable

or not. While ESL could be seen as a “best practice” across the industry and any retailer could

invest in ESL, there would be idiosyncratic differences in the manner different retailers would

use the technology to integrate its existing resources to implement their specific strategies. In

management efficiencies. At the core of this outcome was that ESL enabled the EDLP store

converge on a narrower band of price changes that would effectively limit their end-of-the day

inventory of unsold perishable produce. The HI-LO store, on the other hand, combined product

information and pricing to achieve better value extraction. At the core of this outcome was that

ESL enabled the HI-LO store to communicate more effectively with their customers while

engaging in more effective price discovery.

The lesson from the above in our retail context is that the right strategy per se does not

necessarily yield competitive advantage. Effective implementation of that strategy is crucial. In

circumstances where the implementation itself may be too costly, the retailer will not derive any

advantage from its strategy. However, technologies like ESL may allow retailers to achieve both

operational efficiencies as well as enhance value extracted from its customer transactions,

thereby yielding a strategic dividend on their investments.

Several past papers allude to the potential of ESL enabling strategic capabilities of the retailer

(cf. Dutta, et al. 2003; Levy et al. 1997; Zbaracki et al. 2004; Ray et al. 2006; Bergen et al.

2008). However, to the best of our knowledge, this is the first study to offer direct evidence of

its strategic impact.

ESL through a Policy Lens: Menu Cost Saver

While we illustrate the strategic value of ESL in the earlier discussions, from a policy lens, the

impact of ESL is nuanced. An explicit function of ESLs, as argued in earlier literature, has been

that it reduces menu costs, which are the direct or physical component of the retailer’s total price

adjustment costs (Levy et al. 1997). The associated menu cost theories in the monetary policy

literature (Barro 1972, Sheshinski and Weiss 1977, Mankiw 1985, Ball and Mankiw 1994)

suggest that such lower menu costs would make prices less rigid. In fact, several jurisdictions

specifically incorporate menu cost savings as considerations in enacting their pricing policies

(see Bergen et al. 2008 with respect to Item Pricing Law). Our results illustrate that this policy

impact also depends on retailer strategy.

Whereas, ESL enables the EDLP store to achieve greater pricing consistency by allowing

them to dampen the magnitude of price changes, it works differently for the HI-LO store. For

the latter, ESL appears to enable the retailer extract greater value by effectively lowering the

the policy impact of the ESL technology appears to be ordered by the prevalent retail strategy.

This builds on an emerging literature in marketing, which explores how the extent of variation in

micro-level price rigidity could be strategic in nature (Ray et al. 2006; 2012).

Managerial Implications

The immediate managerial implications of our results pertain to the cost-benefit calculus

facing the retailer tasked with the decision to implement ESL. Our results show that traditional

efficiency arguments related to operational cost savings (e.g. menu costs) are conservative. A

key benefit associated with ESL in our data is that of yielding strategic dividend. In other words,

the large investments needed to implement ESL must be measured against its potential to

generate and claim transactional value, as well.

At the same time, it is important to note that while different retailers interested in gaining

market advantage may adopt the ESL technology as industry “best practices,” the key to

generating competitive advantage is to deploy ESL in combination with the retailer’s other

strategic resources. Thus, the retailer must identify the short-term and long-term benefits as it

engages with the ESL technology. In the short run, the retailer can save in menu costs.

However, these “plug and play” benefits of ESL are not likely to bear competitive advantage for

long. To achieve the long run benefits of better pricing and effective communications, the

retailer must actively engage in a phase of learning and experimentation. It is through these

options and opportunities that the retailer may realize the idiosyncratic benefits of ESL in the <